A steady dividend payer

UTI Mastershare Unit Scheme (UTI Mastershare) is certainly not one of the top performing funds in the large-cap diversified equity category. Yet, the fund has been a consistent performer if you consider a 10-year period. Its most noteworthy feature is that it declared dividends every year in the past 26 years, post its launch in late ‘86. The fund’s return of 19% since inception is evidence to its long-term steady performance.

Suitability

UTI Mastershare is not a fancied fund for those looking to build wealth for medium-term goals. Nor is its performance superior to some of the large-cap peers such as HDFC Top 200 or Franklin India Bluechip.

The fund is only suitable for investors who are looking for limited risk and more importantly would like to get some steady returns from their fund by way of dividends.

While the dividend payout strategy will not help build long-term wealth, such a strategy is for investors who do not like to leave their money on the equity table and prefer to sweep some money off every year.

Fund manager Swati Kulkarni has kept the fund’s risk profile at bay by holding a portfolio dominated by large-cap stocks. To this extent, the fund’s risk profile is also moderate.

Performance

UTI Mastershare is the oldest equity fund. Its presence in the equity market, early on, helped it reap market gains well. A sum of Rs 10,000 invested in the fund in November 1986 would have grown to Rs 3,97,000 as of April 2013. Similar investment in the benchmark would have fetched Rs 3,08,000.

Be that as it may, UTI Mastershare has not been too successful in beating its benchmark in sound market rallies especially in recent years. While it beat its benchmark in the 2007 market rally, it underperformed both in the 2009 market pick-up as well as in 2012.

This can be attributed to the higher proportion of large-cap stocks in its portfolio when compared with its own benchmark the S&P BSE 100; the latter sporting a good dose of nascent large caps and mid caps.

Simply put, that UTI Mastershare stays away from the mid- and small-cap segment has meant that its returns are capped to a good extent, when compared with its benchmark. The Sensex or the Nifty may be a better reference point when comparing this fund’s performance.

Still, in the last 5 years, UTI Mastershare beat its benchmark 73% of the times on a rolling one-year return basis. While this is not outstanding performance, it is still noteworthy. The fund contained declines better than its benchmark in down markets and in markets that lacked direction (like 2010).

It also beat the category average return over three and five-year periods.

The most noteworthy feature of the fund is its ability to declare dividends in all market phases. In bull markets such as 2007, it neatly timed dividends a few months ahead of the peak. In down markets such as 2008 too, its dividends, albeit low, served as a good confidence booster for its investors.

It is true that the fund’s long innings has provided it with sufficient surplus to declare dividends. A fund with limited track record may not have this luxury.

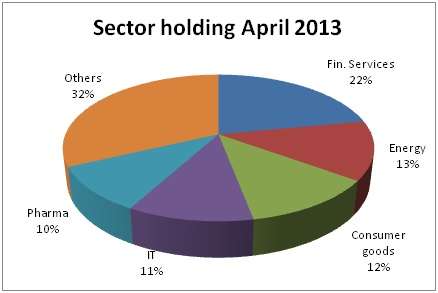

Portfolio

UTI Mastershare held about 88% of its assets in large-cap stocks as of April 2013. The few mid-cap stocks it held were more in the nature of emerging large-caps. The fund made some sector shuffles in the course of the last one year. It marginally increased its exposure to FMCG, although trimming holdings in top stocks such as ITC. It also marginally increased exposure to IT.

In terms of stock picks, the fund made some smart moves in recent times, picking beaten stocks such as IDFC and Adani Port & Special Economic Zone. This helped make some quick gains. That said, overall portfolio turnover remained low over the course of the year with the fund adopting a buy and hold approach in many of the stocks.