The recent news of a downgrade in the debt instruments of quite a few companies, and the resultant mark-to-market loss in some income funds brings out the fact that debt funds are not entirely free of risk. Also, as is the case with equity, debt funds too require a buy and hold approach, if one has to recoup such falls and reduce volatility in performance.

If you cannot take some volatility in your debt, and prefer steady duration quality credit profiles with debt funds, then HDFC Medium Term Opportunities is a good choice for any long-term portfolio.

Investors with a time frame of over 3 years who want to build an asset allocated portfolio of equity and debt can add HDFC Medium Term Opportunities as part of their debt allocation. With a return of close to 9 per cent annually since its launch in 2010, this fund has been a consistent performer, with no period of negative 1-year returns, when rolled daily.

The fund and suitability

HDFC Medium Term Opportunities is an income accrual fund. It predominantly takes exposure to top-rated corporate bonds, and delivers a chunk of its return through accrual (interest), and also through occasional capital appreciation opportunities when the spreads (between corporate bonds and gilts) shrink. Traditionally, its exposure to long-term gilt has been low.

The fund requires a time frame of not less 3 years, what with its average portfolio maturity being typically in the range of 2-3 years. Investors should tame their returns expectation from this fund for two reasons: one, it does not take duration calls. That is, the fund does not load up on long-term gilts that can generate high capital appreciation opportunities in a falling interest rate scenario. Two, the fund does not also take high credit risks, and sticks to instruments with a high rating. Hence, the yield on its instruments will not be as high as those funds that take instruments that are AA-rated and below.

Do note that not taking duration calls or credit calls has helped the fund curtail volatility far better than typical dynamic bond or corporate bonds funds. Hence, its risk profile is lower than the above-mentioned category of funds. You can expect this fund to deliver superior returns to your bank FD on a post-tax basis over 3 years or more.

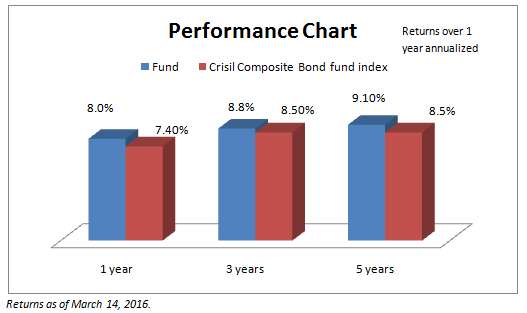

Performance

HDFC Medium Term Opportunities has been an outperformer over 3 and 5-year periods. Over a 5-year period the fund delivered 9.1 per cent annually, beating the benchmark return of 8.5 per cent. Over a 3-year period too, it managed to beat its benchmark by 30 basis points with a return of 8.8 per cent annually.

Still, as is the case with this category of funds, it has not been easy beating the category benchmark – Crisil Composite Bond Index, consistently over shorter periods. For instance, over rolling 1-year returns in the past 3 years, the fund beat its benchmark only 53 per cent of the times. That’s about the same score for top income funds from the Franklin stable as well. This difficulty in beating the benchmark consistently is because the Crisil Composite Bond Fund index has a 40 per cent exposure to long-term gilt, and most income funds (other than dynamic bond funds) do not take such exposure.

HDFC Medium Term Opportunities, for instance, had an average 7 per cent exposure to gilt in the past 2 years (although it held 26 per cent in medium-term government securities as of February 2016), and that too in gilt with short to medium-term portfolio maturity. That means any returns from an interest rate rally will not be reflected in its performance. Equally, any fall if duration calls misfire (as it happened in the last few months) won’t affect the fund’s returns.

For example, in the past one year, while HDFC Medium Term Opportunities managed to hold to 8 per cent returns, many dynamic bond funds that had one-year double digit returns a few months ago, slipped to returns in the range of 4-6 per cent for the same period.

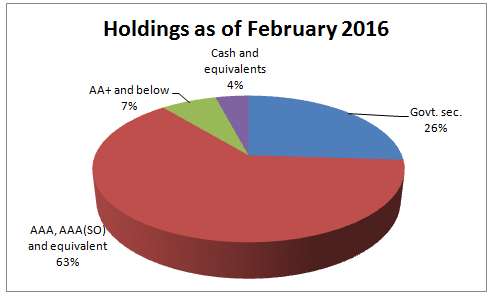

Portfolio

HDFC Medium Term Opportunities holds close to 62 per cent of its assets in AAA-rated corporate bonds. While it upped its exposure to government papers to 26 per cent, it is mostly medium-term papers with less than 5-year residual maturity. Therefore, its average maturity remains low at under 3 years. As opposed to this, its benchmark had an average maturity of 7.6 years (January 2016), as a result of higher exposure to long-term gilt.

As part of its corporate bond exposure, it holds several PSU bonds such as REC, NTPC, PFC and IRFC, thus keeping its portfolio credit risk quite low.

The fund’s current yield to maturity at 8.3 per cent will likely ensure you get returns several notches higher than your FD over a 3-year time frame.

The fund is managed by Anupam Joshi from October 2015. It has over Rs. 4,000 crore of assets.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis of investment decisions. To know how to read our weekly fund reviews, please click here.

How dies the taxation work? Similar to debt funds? I.e. DDT at AMC ? 9.1% is post DDT or pre DDT

Hello Sir,

Taxation is similar to all debt funds. Gains over 3 years get capital gains indexation benefit and then subject to 20% tax. Less than 3 year holding will be taxed at your slab rate. DDT is only in the dividend option. 9.1% is the returns of the fund under the growth option. That is what is seen to assess the performance of a fund. Under dividend option 28.33% is dividend distribution tax on the dividend option. To answer your question 9.1% is not post tax returns.

thanks

Vidya

thanks

Vidya

How dies the taxation work? Similar to debt funds? I.e. DDT at AMC ? 9.1% is post DDT or pre DDT

Hello Sir,

Taxation is similar to all debt funds. Gains over 3 years get capital gains indexation benefit and then subject to 20% tax. Less than 3 year holding will be taxed at your slab rate. DDT is only in the dividend option. 9.1% is the returns of the fund under the growth option. That is what is seen to assess the performance of a fund. Under dividend option 28.33% is dividend distribution tax on the dividend option. To answer your question 9.1% is not post tax returns.

thanks

Vidya

thanks

Vidya