Last week, we covered the tax rules with regard to all categories of mutual funds. You know that with mutual funds, taxes apply in your hands at the time of your redeeming your fund and that your tax liability depends on how long you held the fund.

If you sold all your units at one go, and bought it on a single date, it is easy to arrive at the holding period. But what if you redeemed in multiple tranches? What if you had invested at multiple points, like you do in an SIP? How then do you calculate what your holding period is, and consequently, what tax applies?

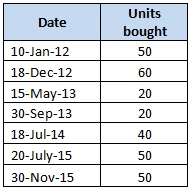

Determining holding periods

The rule the taxman follows is that the first unit you bought is the first you sold. This first-in-first-out rule also applies while determining whether units of tax-saving funds are free from lock-in.

Here’s an example to make it more clear. Let’s say you invested in a fund at various points of time as below:

Now, you have a total of 290 units today. You decide to sell 100 units. Going by the rule, thus, it’s assumed that the 50 units bought on the 10th Jan 2012 and 50 of the units bought on 18th December 2012 are sold. If the fund is an equity fund, you won’t pay capital gains tax as the holding period of the units is greater than one year. If it was a debt fund, since the holding period from January and December 2012 is longer than three years, you will pay long-term capital gains tax. What if you sold all 290 units? If it’s an equity fund, for the units bought in July and November 2015 (100 units), you will pay short-term capital gains tax as the holding period is less than a year. On the remaining 190 units, you pay no tax. If it was a debt fund, then, the 160 units you bought from September 2013 onwards will qualify as short-term. The 130 units you bought between January and May 2013 will qualify as long-term.

In other words, the holding period of every unit that you bought would be from the date of such unit’s purchase.

Consider a systematic transfer plan (STP). Apply the rule above. The units you sell is taxed based on the date of its purchase. That’s easy. But what is the date of purchase of the fund you are transferring into? When this money is transferred into another fund, the date of purchase for this fund would be the date when the units are credited to you.

For example, say you are doing an STP from Fund X to Fund Y for Rs 1000 a month. The date of sale for X fund would be the date of STP. For the Y fund, the date of purchase would be when new units are credited to you under Fund Y. This is the case with any switch-out and switch-in of funds.

Thus, date of purchase remains a key input for you to determine your holding period.

To understand the basics of mutual fund taxation, read the first part of our taxation series.

Dear Sir

Who will calculate the capital gain tax on MF ? The incumbent orthe fund house ? How the tax will be paid ?

Will it be under the head of income from other sources ?

Hi Arijit,

Since a lot of you need clarity over how to look at these incomes and where they fall, as well as setting off, we’ll do a separate blog on it in a couple of weeks. It will be easier to explain it in detail instead of in a comment. Do look out for it.

Thanks,

Bhavana

Is this is applicable to share purchase in SIP manner?

This is a great article with detailed explanation. I was hoping you would also cover taxation for other types of funds such as foreign funds (those that invest in Nasdaq etc.), gold linked funds, ultra liquid funds etc. Could you please throw some insights into that?

Thanks, Mitesh! All funds that aren’t equity funds are taxed the same way. That is, equity funds hold nil tax on long-term capital gains if held for more than one year. All other funds have short-term capital gains (less than 36 months) taxed at slab rate and long-term capital gains taxed at 20% with indexation. Its explained here: https://blog.fundsindia.com/blog/mutual-funds/fundsindia-explains-how-are-mutual-funds-taxed-part-i/9107

Regards,

Bhavana

Nice article…First part of article was very informative. However some more clarifications are expected from this second part.

I can see in my portfolio view there is short term and long term gains/loss mentioned for each fund. If I redeem all units. Can I combine the short term and long term gains/loss. Means can short term losses be compensated with long term gains or vice versa?

Hi Gangadhar,

Short-term capital loss on both equity and debt can be set off against both short-term (equity and debt) and long-term capital gains (debt). Long-term capital loss can be set off only against long-term capital gains (both in debt only), and carried forward for 8 years. Long-term capital loss on equity cannot be set off against anything, since capital gains are exempted from tax in this category.

Thanks,

Bhavana

Great help from this article and the first part !!!

A MUST READ for all investors of mutual funds.

Please go a step further and explain the filling up of Schedule CG(Capital Gains) for STCG and for LTCG made from

investment in mutual funds.The form applicable for Capital Gains is ITR2 .

Kindly give the pictorial snapshot of both the excel and Java utility’s form’s line number(picture of the relevant column) where we need to drop the figures of capital gains.

So far, I know is that the LTCG of Equity mf are to be mentioned in the EXEMPT income column of itr1 and in the schedule EI(Exempt Income ) of itr2.

Just help us know the columns (with pics) WHERE to DROP the figure of capital gains for STCG & LTCG , both for EQUITY & DEBT mfs.

Do we need to reflect the same figures in Schedule SI(Special rate Income) also? I believe the utility picks the value AUTOMATICALLY from schedule CG in itr 2.

Plz devote an article for the ITR FILLING with respect to capital gains from mutual funds. It is much needed.

Thanks for this wonderful article !!

Great help from this article and the first part !!!

A MUST READ for all investors of mutual funds.

Please go a step further and explain the filling up of Schedule CG(Capital Gains) for STCG and for LTCG made from

investment in mutual funds.The form applicable for Capital Gains is ITR2 .

Kindly give the pictorial snapshot of both the excel and Java utility’s form’s line number(picture of the relevant column) where we need to drop the figures of capital gains.

So far, I know is that the LTCG of Equity mf are to be mentioned in the EXEMPT income column of itr1 and in the schedule EI(Exempt Income ) of itr2.

Just help us know the columns (with pics) WHERE to DROP the figure of capital gains for STCG & LTCG , both for EQUITY & DEBT mfs.

Do we need to reflect the same figures in Schedule SI(Special rate Income) also? I believe the utility picks the value AUTOMATICALLY from schedule CG in itr 2.

Plz devote an article for the ITR FILLING with respect to capital gains from mutual funds. It is much needed.

Thanks for this wonderful article !!

If I switch from one debt fund to another debt fund within 3 years, do I need to pay short term capital gains tax?

Hi Akash, Yes you will have to pay taxes on the fund that you switched out of. Vidy

Hi Akash, Yes you will have to pay taxes on the fund that you switched out of. Vidya

hi, if i have to pay tax on Liquid/ultra short term or short term fund, how are the better than FDs or sweep-in account? especially if it’s for 3-6months, the difference in the returns is not much! Is it better only because it’s taxed on redemption that too after indexation or am I missing something. It would be very helpful if you explain. I have been waiting to invest for emergency fund and not clear where to!

thanks

regards

Hi,

No, debt funds generally give returns higher than FDs or savings bank (which is what a liquid fund should ideally be compared with) apart from being more tax-efficient in the long term. Debt funds invest in instruments that deliver higher returns which retail investors do not have access to. You can read these two posts – here and here – to better understand the debt funds vs FD argument.

For emergency funds, liquid funds are best suited as they can be redeemed within a day. You will find it hard to break FDs when you need the cash, and you may have to pay penalties as well. You would be paying the tax every year on these FDs. With a liquid fund, you would not be paying any tax until you actually redeem. And in the best circumstances, it wouldn’t be happening very soon 🙂 So you’d benefit much more with a liquid fund.

Thanks,

Bhavana

Hello,

Part 1 and 2 are informative, good reads.

I recall one more article but cannot locate it – It was surely from FI, but not sure if it blog entry or something else.

I currently invest in mutual funds through FI and can download my CG statement GROUPED BY ASSET CLASS and the article explained precisely how to make use of the grouping when filling up ITR2.

Please can you direct me to it?

thanks

Jeevan

Hello Sir,

Not sure which article you’re referring to, but you can check if the following link answers it. I don’t recall any other article that specifically dealt with tax filing procedures.

https://blog.fundsindia.com/blog/general/5-things-to-note-before-you-file-your-income-tax-return/3031

Thanks,

Bhavana

Nice reading part I and II of the articles on MF Taxation. It’s really very informative and easy understandable.

In respect of my post- retirement funds, some amounts have been kept in EQ oriented (Growth & Dividend) funds in addition to some amounts in Debt and Liquid/ Ultra Liquid fund.

Now, after completion of one year period investments in EQ funds, STP of such funds (EQ oriented) to Debt Fund and Liquid Fund are being done. Again SWP from Debt fund after 3 years holding to be done to meet up expenses need and surplus (if any) to be re-invested in EQ fund for one year. Liquid funds stands as ‘Emergnecy’ without any SWP.

Is it an efficient Tax management approach?

Thanks for your valuable advice in advance

Hi,

You’ve approached this entirely from the tax angle, which isn’t always the best thing to go by. Yes, equity gains are tax-free after a year, but there are enough chances that your returns are going to be low if you hold it only for a year. For the 2015 and 2016 calendar, for example, returns were less than 5%. In the past 1 year, yes, markets are up 11-12%, but if a correction happens now returns will reverse quickly. For equity, you need a 4-5 year horizon minimum. So if you’re doing an STP from equity to debt immediately after 1 year, your returns are unlikely to be optimal for long. For retirement purposes, its best to keep requirements for around 5 years in pure debt funds and invest only the remaining in equity funds. You will pay tax on it for some time, but that’s fine. Safety is more important. Also remember that, in withdrawals, there is a cost component each time. So you’re not paying tax on the entire amount but only on the gain – for ex, if you withdraw Rs 10,000, and the investment cost of those units is Rs 9,000, then you’re paying tax only on Rs 1,000 and not the entire withdrawal amount.

Thanks,

Bhavana

Hi Team

I bought one equity linked mutual fund i.e. a lifestage pension advantage fund with a yearly premium of 50K.

this was bought in Feb’ 2010. Six months back I switched my entire money from equity fund to money market fund under the same policy as I was given the option to switch funds if I wanted. I went to surrender my policy today and I was told that I will be charged an income tax as per my salary slab. Can you please advise if an income tax will be charged on this policy which was purchased almost 8 years back.

Thanks for your cooperation!

So, from these articles the thing is: Tax is to be paid for the profits and not on the investements.

If I invested 1,00,000 and if my total returns is 1,20,000 and if the tax % is x….

Then tax paid by me is 20,000 * x / 100. Am I right..??

Hello,

Tax is always paid on profits and not investments 🙂 Tax is on “income”, and in the case of investments, this income is in the form of profits. So yes, tax to be paid is tax rate * gain. Please note that tax laws on equity investments have changed from the date of this point. You can access the updated info here: https://www.fundsindia.com/blog/mf-basics/investment-definitions/new-tax-structure-mutual-funds/13035

Thanks,

Bhavana

Dear Sir

Who will calculate the capital gain tax on MF ? The incumbent orthe fund house ? How the tax will be paid ?

Will it be under the head of income from other sources ?

Hi Arijit,

Since a lot of you need clarity over how to look at these incomes and where they fall, as well as setting off, we’ll do a separate blog on it in a couple of weeks. It will be easier to explain it in detail instead of in a comment. Do look out for it.

Thanks,

Bhavana

This is a great article with detailed explanation. I was hoping you would also cover taxation for other types of funds such as foreign funds (those that invest in Nasdaq etc.), gold linked funds, ultra liquid funds etc. Could you please throw some insights into that?

Thanks, Mitesh! All funds that aren’t equity funds are taxed the same way. That is, equity funds hold nil tax on long-term capital gains if held for more than one year. All other funds have short-term capital gains (less than 36 months) taxed at slab rate and long-term capital gains taxed at 20% with indexation. Its explained here: https://blog.fundsindia.com/blog/mutual-funds/fundsindia-explains-how-are-mutual-funds-taxed-part-i/9107

Regards,

Bhavana

Nice article…First part of article was very informative. However some more clarifications are expected from this second part.

I can see in my portfolio view there is short term and long term gains/loss mentioned for each fund. If I redeem all units. Can I combine the short term and long term gains/loss. Means can short term losses be compensated with long term gains or vice versa?

Hi Gangadhar,

Short-term capital loss on both equity and debt can be set off against both short-term (equity and debt) and long-term capital gains (debt). Long-term capital loss can be set off only against long-term capital gains (both in debt only), and carried forward for 8 years. Long-term capital loss on equity cannot be set off against anything, since capital gains are exempted from tax in this category.

Thanks,

Bhavana

Is this is applicable to share purchase in SIP manner?

If I switch from one debt fund to another debt fund within 3 years, do I need to pay short term capital gains tax?

Hi Akash, Yes you will have to pay taxes on the fund that you switched out of. Vidy

Hi Akash, Yes you will have to pay taxes on the fund that you switched out of. Vidya

Hi Team

I bought one equity linked mutual fund i.e. a lifestage pension advantage fund with a yearly premium of 50K.

this was bought in Feb’ 2010. Six months back I switched my entire money from equity fund to money market fund under the same policy as I was given the option to switch funds if I wanted. I went to surrender my policy today and I was told that I will be charged an income tax as per my salary slab. Can you please advise if an income tax will be charged on this policy which was purchased almost 8 years back.

Thanks for your cooperation!

Nice reading part I and II of the articles on MF Taxation. It’s really very informative and easy understandable.

In respect of my post- retirement funds, some amounts have been kept in EQ oriented (Growth & Dividend) funds in addition to some amounts in Debt and Liquid/ Ultra Liquid fund.

Now, after completion of one year period investments in EQ funds, STP of such funds (EQ oriented) to Debt Fund and Liquid Fund are being done. Again SWP from Debt fund after 3 years holding to be done to meet up expenses need and surplus (if any) to be re-invested in EQ fund for one year. Liquid funds stands as ‘Emergnecy’ without any SWP.

Is it an efficient Tax management approach?

Thanks for your valuable advice in advance

Hi,

You’ve approached this entirely from the tax angle, which isn’t always the best thing to go by. Yes, equity gains are tax-free after a year, but there are enough chances that your returns are going to be low if you hold it only for a year. For the 2015 and 2016 calendar, for example, returns were less than 5%. In the past 1 year, yes, markets are up 11-12%, but if a correction happens now returns will reverse quickly. For equity, you need a 4-5 year horizon minimum. So if you’re doing an STP from equity to debt immediately after 1 year, your returns are unlikely to be optimal for long. For retirement purposes, its best to keep requirements for around 5 years in pure debt funds and invest only the remaining in equity funds. You will pay tax on it for some time, but that’s fine. Safety is more important. Also remember that, in withdrawals, there is a cost component each time. So you’re not paying tax on the entire amount but only on the gain – for ex, if you withdraw Rs 10,000, and the investment cost of those units is Rs 9,000, then you’re paying tax only on Rs 1,000 and not the entire withdrawal amount.

Thanks,

Bhavana

Hello,

Part 1 and 2 are informative, good reads.

I recall one more article but cannot locate it – It was surely from FI, but not sure if it blog entry or something else.

I currently invest in mutual funds through FI and can download my CG statement GROUPED BY ASSET CLASS and the article explained precisely how to make use of the grouping when filling up ITR2.

Please can you direct me to it?

thanks

Jeevan

Hello Sir,

Not sure which article you’re referring to, but you can check if the following link answers it. I don’t recall any other article that specifically dealt with tax filing procedures.

https://blog.fundsindia.com/blog/general/5-things-to-note-before-you-file-your-income-tax-return/3031

Thanks,

Bhavana

hi, if i have to pay tax on Liquid/ultra short term or short term fund, how are the better than FDs or sweep-in account? especially if it’s for 3-6months, the difference in the returns is not much! Is it better only because it’s taxed on redemption that too after indexation or am I missing something. It would be very helpful if you explain. I have been waiting to invest for emergency fund and not clear where to!

thanks

regards

Hi,

No, debt funds generally give returns higher than FDs or savings bank (which is what a liquid fund should ideally be compared with) apart from being more tax-efficient in the long term. Debt funds invest in instruments that deliver higher returns which retail investors do not have access to. You can read these two posts – here and here – to better understand the debt funds vs FD argument.

For emergency funds, liquid funds are best suited as they can be redeemed within a day. You will find it hard to break FDs when you need the cash, and you may have to pay penalties as well. You would be paying the tax every year on these FDs. With a liquid fund, you would not be paying any tax until you actually redeem. And in the best circumstances, it wouldn’t be happening very soon 🙂 So you’d benefit much more with a liquid fund.

Thanks,

Bhavana

So, from these articles the thing is: Tax is to be paid for the profits and not on the investements.

If I invested 1,00,000 and if my total returns is 1,20,000 and if the tax % is x….

Then tax paid by me is 20,000 * x / 100. Am I right..??

Hello,

Tax is always paid on profits and not investments 🙂 Tax is on “income”, and in the case of investments, this income is in the form of profits. So yes, tax to be paid is tax rate * gain. Please note that tax laws on equity investments have changed from the date of this point. You can access the updated info here: https://www.fundsindia.com/blog/mf-basics/investment-definitions/new-tax-structure-mutual-funds/13035

Thanks,

Bhavana