Key Highlights

1. Continuing on the path of Fiscal Consolidation

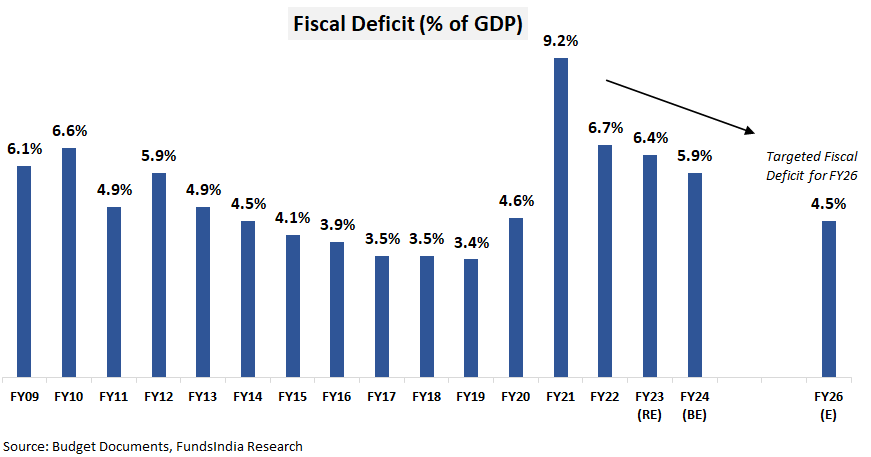

- Projected fiscal deficit at 5.9% of GDP for FY24 – in line with the fiscal consolidation glide path – to reduce fiscal deficit to 4.5% of GDP by FY26

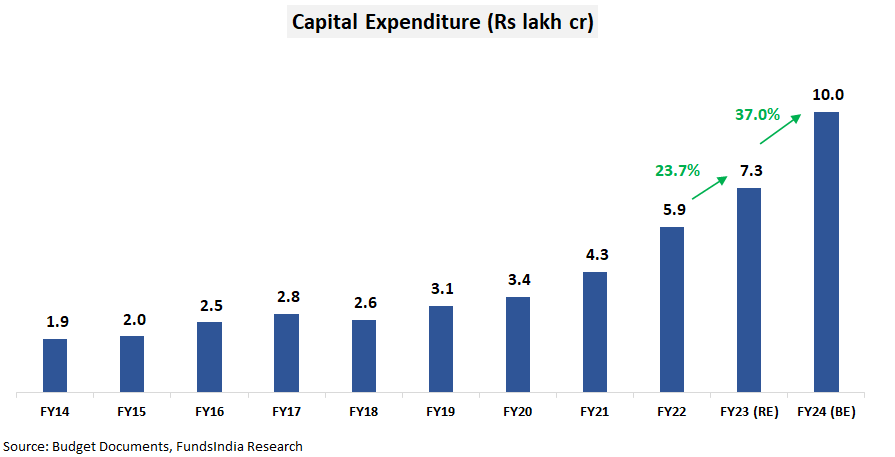

2. Strong thrust on Capital Expenditure (Infrastructure) – has significant multiplier effects on growth and employment

- 37% increase in Capital Expenditure from Rs 7.3 lakh cr in FY23 (RE) to Rs 10 lakh cr in FY24

- Major focus is on:

- Road Transport and Highways (Rs 2.6 lakh cr)

- Railways (Rs 2.4 lakh cr)

- Defence (Rs 1.6 lakh cr)

3. Cut in Personal Income Tax under New Tax regime

Multiple changes have been made to the new income regime to make it more attractive (details in a later section).

4. No changes to Equity or Mutual Fund taxation

Budget in Visuals

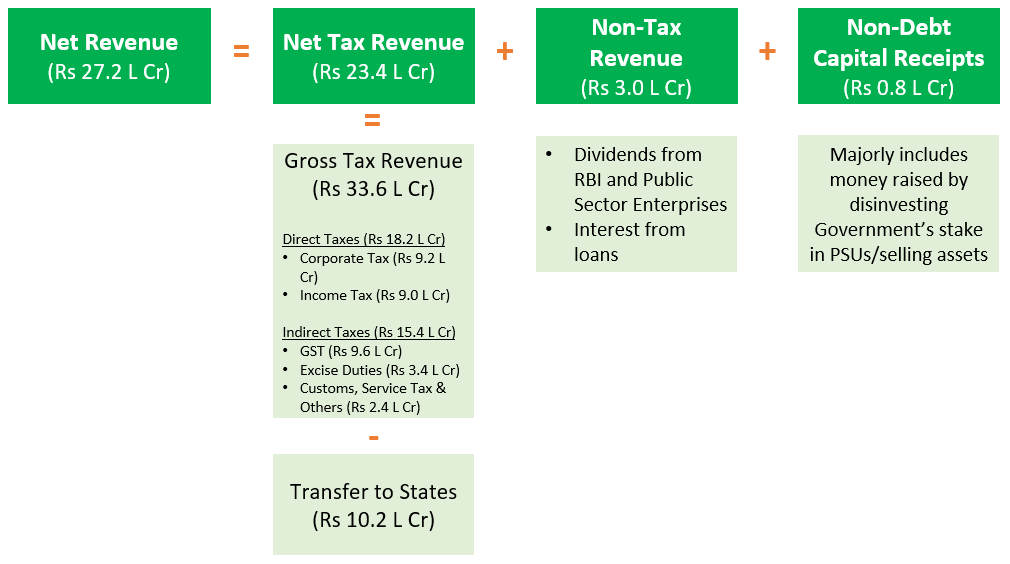

Where does the money come from?

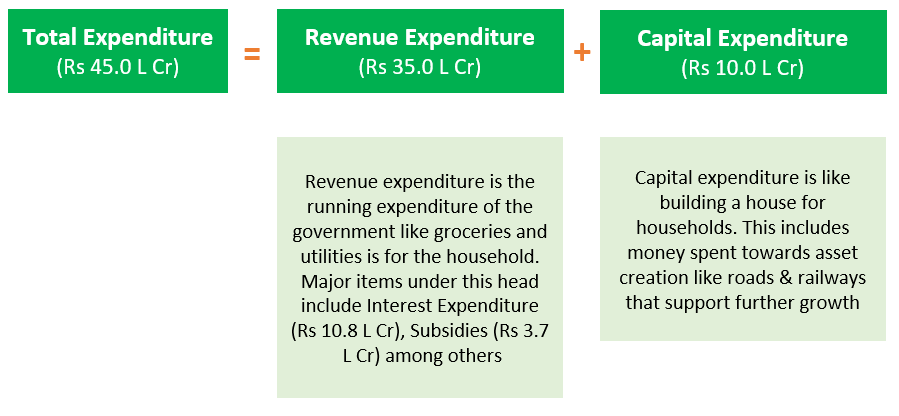

Where does the money go?

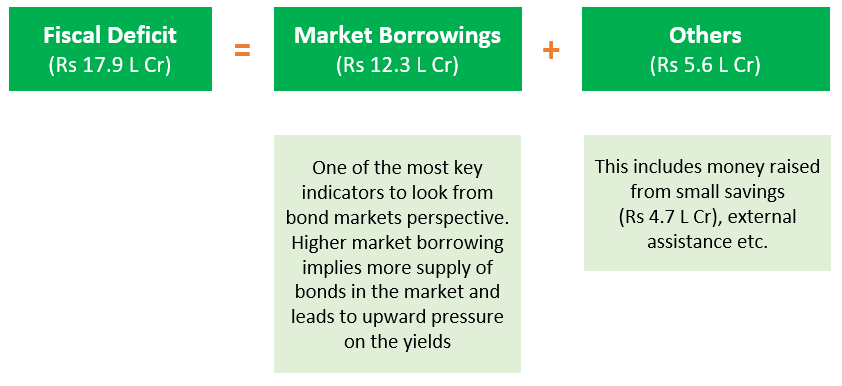

How is the deficit financed?

Fiscal Consolidation On Track

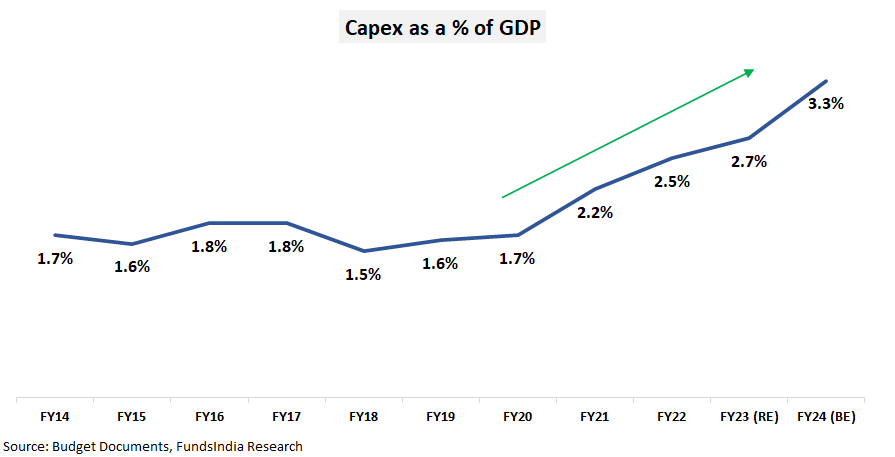

Thrust on Capex Continues

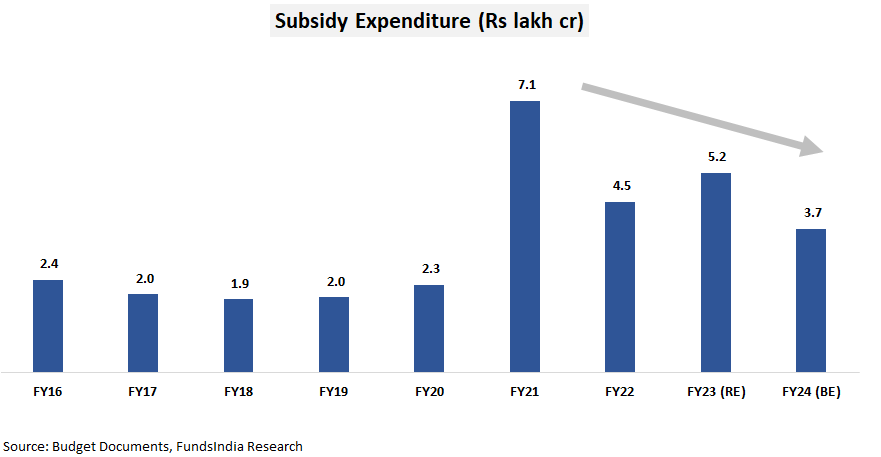

Subsidy expenses continue to slide

What’s in it for you?

1. No change in Equity or Mutual Fund Taxation

- Taxation of equity, equity mutual funds and other non-equity mutual funds remains the same

2. Nudge towards New Income Tax Regime with multiple revisions

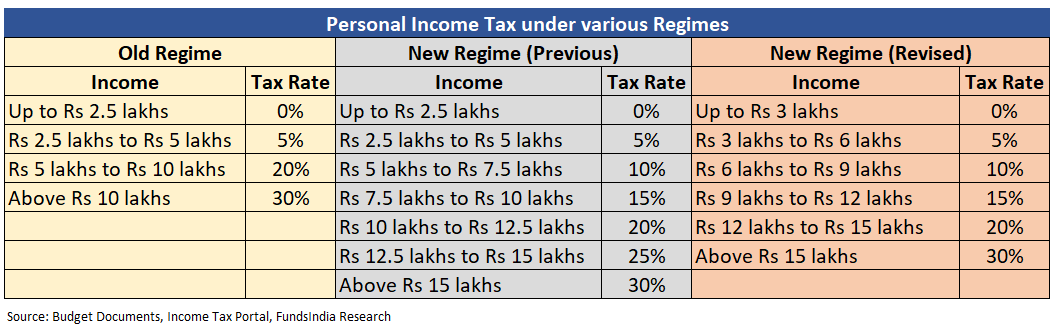

- Revisions in the income tax slabs – The tax slab under the new regime has been revised as follows

- Increase in the Tax Rebate limit – The tax rebate limit has been increased to Rs. 7 lakhs (from Rs. 5 lakhs). This means that taxable income up to Rs. 7 lakhs will be essentially tax-free from FY24 (any tax paid can be claimed back when filing the returns).

- Standard deduction benefit extended to the new regime – Standard deduction of Rs 50,000 which was so far available only under old tax regime has now been extended to new tax regime.

- Relief for High Earners – Surcharge on the tax paid by individuals earning over Rs. 5 crores has been reduced from 37% to 25%. This change reduces the effective tax rate from 42.7% to 39%.

3. Maturity amount on Insurance premium above Rs 5 lakhs will be taxed

Income from life insurance policies (non-ULIPs) where the aggregate premium is up to Rs 5 lakhs will continue to be tax exempt. But income from policies with yearly premium more than Rs 5 lakhs will be taxed at the applicable slab rates.

4. Cap imposed on reinvestment of gains from residential property

Currently, there is no need to pay taxes on the long-term capital gains from the sale of an asset, if the gains are used to purchase a residential property. This tax exemption has now been capped at Rs 10 crores.

5. Market Linked Debentures to get taxed per slab

Until now, there was a taxation arbitrage in Market Linked Debentures (a type of a listed debt security). If you held an MLD for more than a year and then sold it, it was classified as long term capital gains which were taxed at 10%. Going forward, this taxation arbitrage won’t be applicable and any capital gains from MLDs will be treated as short-term capital gains and will get taxed at the applicable slab rates irrespective of the holding period. This has no impact on the taxation of fixed income mutual funds.

6. Higher Tax Collected at Source for foreign remittances

The Tax Collected at Source on payments made through the Liberalised Remittance Scheme (excluding education and medical expenses) has been increased from 5% to 20%. For instance, if you invest in foreign stocks under LRS, you will have to shell out 20% more at the time of payment. However this can be adjusted against the tax payable or claimed back as refund while filing the returns.

7. Increase in Earned Leave Encashment Limit

The limit of Rs 3 lakhs for tax exemption on leave encashment on retirement of non-government salaried employees has been increased to Rs 25 lakhs.

8. Maximum Deposit Limit for SCSS has been doubled

The limit for the amount that can be deposited under the Senior Citizens Savings Scheme has been doubled from Rs 15 lakhs to Rs 30 lakhs

9. What could get Cheaper / Costlier?

- Cheaper: Mobiles Phones, TV Sets, Lab Grown Diamonds, Pecan Nuts etc

- Costlier: Cigarettes, Gold & Silver articles, Imitation Jewellery, Imported Cars, Toys etc

Equity View: Growth remains the priority – Positive for Equity Markets

The Union Budget FY24 continues to put growth on the forefront. The focus remains on capital expenditure that can drive a multiplier impact on economic growth and employment. This is evident from the sharp 37% increase in capital expenditure for FY24 (versus a meagre 1% increase in revenue expenditure).

Contrary to some pre-budget rumours, no changes were made to the equity capital gains taxation. This removes the near term uncertainty with regards to equity taxation.

Prior to the budget, we had a POSITIVE view on Equities with a 5-7 year horizon

Our Equity view is derived based on our 3 signal framework driven by

- Earnings Cycle

- Valuation

- Sentiment

As per our current evaluation we are at

NEUTRAL VALUATIONS + EARLY PHASE OF EARNINGS CYCLE + NEUTRAL SENTIMENTS

We expect a robust earnings growth environment over the next 3-5 years. This expectation is led by Manufacturing Revival, Banks – Improving Asset Quality & pickup in loan growth, Revival in Real Estate, Government’s focus on Infra spending (which continues in FY24 Budget), Early signs of Corporate Capex, Structural Demand for Tech services, Structural Domestic Consumption Story, Consolidation of Market Share for Market Leaders, Strong Corporate Balance Sheets (led by Deleveraging) and Govt Reforms (Lower corporate tax, Labour Reforms, PLI) etc.

The equity market valuation measured via FundsIndia Valuemeter has turned NEUTRAL as on 31-Jan-2023 (was in the expensive zone in Dec-22).

From a sentiment point of view, direction of FII flows remains a key near term trigger. The market expectations on next year elections which will start getting built by the fag end of this year will also have an influence on near term returns.

Overall, we maintain our Positive view on Indian equities from a 5-7 year time frame. The Budget announcements reinforce our robust earnings growth outlook.

Fixed Income View: Stability on the fiscal front – Favourable for Debt Markets

The Fiscal Deficit for FY24 at 5.9% of GDP is broadly consistent with the fiscal glide path and in line with our expectation. The government also reiterated its intention to bring this deficit number down to 4.5% of GDP by FY26.

FY24 Net Market Borrowing (Gsec +T bills) at INR 12.3 lakh crores also is in line with the bond markets expectations.

The absence of significant negative surprises in the budget seems to have kept the bond yields in check.

In our assessment, we may be close to peak policy rates driven by

- Sharp fall in domestic inflation in recent months – CPI inflation dropped by 169 basis points from 7.41% in Sep-22 to 5.72% in Dec-22

- The current repo rate at 6.25% is comfortably above RBI’s inflation expectation of 5.0% in Q1 FY24.

- The external monetary environment is showing some signs of easing amid falling global inflation and slowing pace of rate hikes by the US FED.

We expect RBI to go for a long pause in rate hikes from hereon or after one more rate hike to 6.50% in the next policy.

Given the sharp increase in yields over the last 12 months, 3-5 year bond yields (GSec/AAA) continue to remain attractive. The current yields provide a sufficient buffer for higher returns compared to FDs over a 3+ year time frame even if yields were to temporarily slightly inch up further.

We prefer debt funds with

- High Credit Quality (>80% AAA exposure)

- Short Duration (1-3 years) or Target Maturity Funds (3-5 years)