Target maturity funds have gained a lot of popularity in recent times. In 2022 alone, mutual fund houses have newly launched over 40 of these funds.

Perhaps you’re wondering what target maturity funds are and why they’ve become so popular lately.

Let us find out!

What are Target Maturity Funds?

Target Maturity Funds are debt funds that share some characteristics of fixed deposits.

Just like other debt mutual funds, Target maturity funds invest in a basket of fixed-income securities such as Government bonds, State Development Loans, and bonds issued by PSUs & high-quality Corporates.

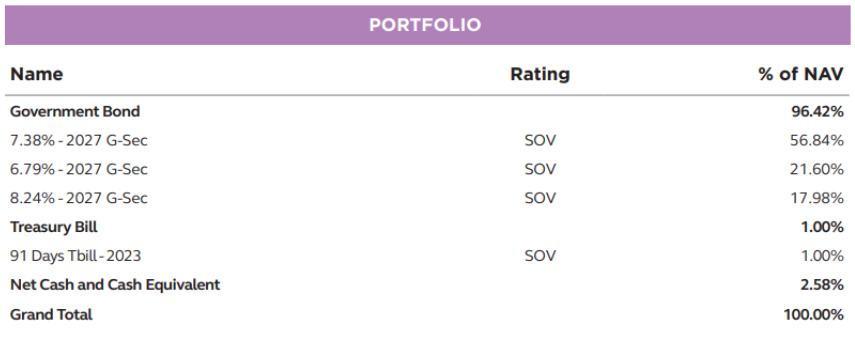

The difference is they are passively managed i.e. they track specific fixed-income indices and invest in line with the index. For example, IDFC CRISIL Gilt 2027 Index Fund which is a target maturity fund tracks the Crisil Gilt 2027 Index.

Similar to FDs, Target maturity indices have a pre-defined maturity date. The investments mature closer to this date, and your money gets credited back to your bank account post-maturity.

For instance, IDFC CRISIL Gilt 2027 Index Fund invests in 2027 G-Secs and will mature on June 30, 2027.

And just like FDs, we can also get to know the ballpark expected returns of a target maturity fund at the time of investment.

The fund returns will be closer to the net yield-to-maturity (YTM) at the time of investment provided we stay invested until maturity. Net YTM is the difference between the fund’s yield to maturity at the time of investment and its expense ratio.

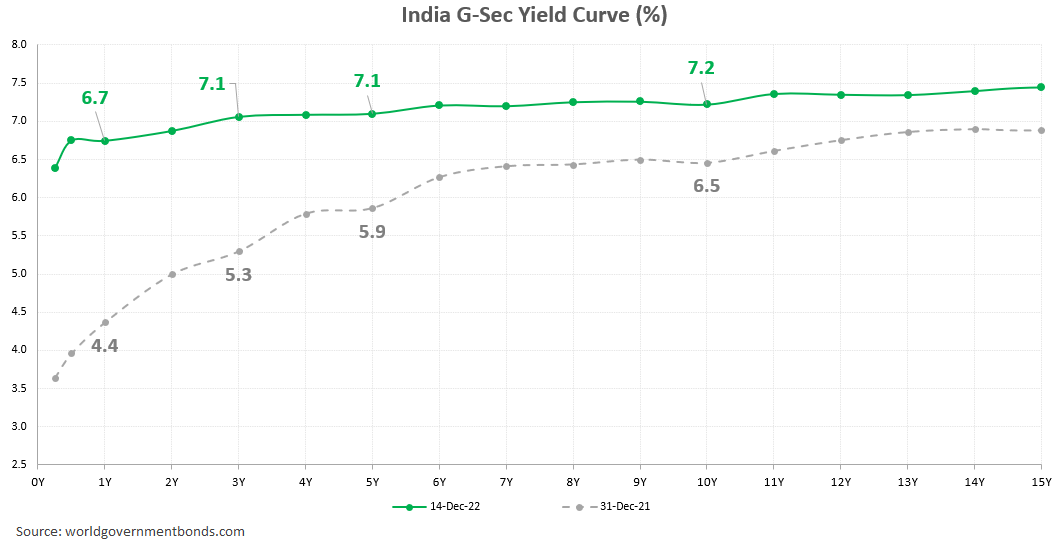

On 14-Dec-2022, IDFC CRISIL Gilt 2027 Index Fund had a YTM of 7.19% and an expense ratio of 0.41%. It means that investments made on that day will have returns pretty close to the net YTM of 6.78% if you hold till the time of maturity.

But, how are the target maturity fund returns predictable?

Imagine you are lending Rs. 1,000 to someone who will pay you Rs. 70 interest at the end of every year for five years and will return the borrowed money at the end of the fifth year.

So, your annual returns over the five-year period would be 7% (there is something called reinvestment risk which we will ignore for the time being).

Simple, right?

Target maturity funds do pretty much the same thing. They buy bonds (i.e. lend) with the money you invest and then hold those bonds until maturity. So, your returns will roughly be the net YTM at the time of investment.

However, the actual returns might differ when the following happens…

1. When investments are exited early

As the investments are currently made in Sovereign & AAA-rated papers where the chances of a default are very low, target maturity funds do not carry any notable credit risk. (Though this is the case now, it is always a good practice to keep a check on the underlying credit risk before any investment)

While credit risk is not a problem, the returns are prone to interest rate risk. The open-ended structure of target maturity funds gives you the option to redeem your investments at any time. If exited before maturity, your returns may differ from the original yields depending on the interest rates prevalent at that time.

This is the most important risk and may impact your actual returns positively or negatively. But the good news is you can avoid this risk by simply holding the funds until maturity.

2. When interest received is reinvested at significantly different yields

When target maturity funds receive interest from their bond investments, they go ahead and buy more bonds with the interest money. These reinvestments can happen at yields higher or lower than the original yields depending on the interest rate environment.

Though this cannot be avoided, the resulting positive or negative impact of this reinvestment risk is likely to be very small, particularly for funds with shorter maturities (up to 5 years).

3. When there are other operational changes & challenges

As bonds have lower liquidity (traded volumes are lower), the funds might face some difficulties in replicating the index portfolio. Further, funds hold a small portion of their assets in cash which will have lower yields. There can also be other operational changes such as revision in expense ratio.

Again, these cannot be avoided. However, the impact (+ve or-ve) is likely to be very minimal.

The odds of these possibilities resulting in significant differences in returns is too low (especially when the investments are held till maturity). Therefore, target maturity funds can be preferred to ‘lock-in’ yields at a given time.

This brings us to the question, is now a good time to lock in yields?

In order to address high inflation, RBI has been increasing interest rates.

Due to this, the bond yields have risen sharply in 2022.

In our view, bond yields especially those in the 3-5 year segment are attractive. We believe we are close to the peak policy rates and there may not be a large up-move in yields from here.

Therefore, the current high yields offer a good entry point.

How to invest?

We prefer Target Maturity Funds with a 3-5 year maturity for the following reasons

- Bond yields in the 3-5 year segment are currently attractive

- Tax efficiency kicks in after 3 years

If you have goals coming up in the next 3-5 years and need a predictable low-risk investment option, you can go for target maturity funds. The investments can be made either as a lump sum or can be staggered over the next 1-3 months.

Summing it up

Target Maturity Funds are passively managed debt funds that mature at a specific date. The returns of these funds will be closer to the Net YTM at the time of investment if you stay invested until maturity.

As the bond yields have risen in recent months, now might be a good time to invest and lock in yields.

Note: The taxation part that appeared in the original version has been edited out due to debt fund taxation changes effective FY24