The government, last week, passed a new ordinance to change the Banking Regulations Act, towards empowering the RBI to deal with bad loans. Broadly, the change will mean that the RBI can now:

- direct banks to begin insolvency procedure against defaulting companies

- direct banks to expedite resolution processes in case of specific borrowers, in case of stressed assets

The changes allow RBI to basically price the distressed assets and make commercial decisions. The ordinance also ensures that lack of a consensus among lending consortium banks is not a reason for delayed resolution proceedings. For any decision on bad loan clean-up, 75% of the consortium (group of banks lending to a company) lenders in terms of value and 60% in terms of number of lenders needed to agree. This is now reduced to 60% of lenders by value and 50% in terms of number of lenders.

Why the recent moves?

We had, a couple of weeks ago, discussed about some of the RBI notifications that tightened the norms for bad loan provisioning by banks. Seen together with the latest ordinance, it is becoming evident that the RBI and the government are earnest about cleaning up the non-performing loan book of banks – an issue ailing the sector for close to 4 years now. With gross non-performing asset value of over Rs 7 trillion rupees or about 10% of total bank credit (from about 4% 3 years ago), the NPA numbers have become worrisome.

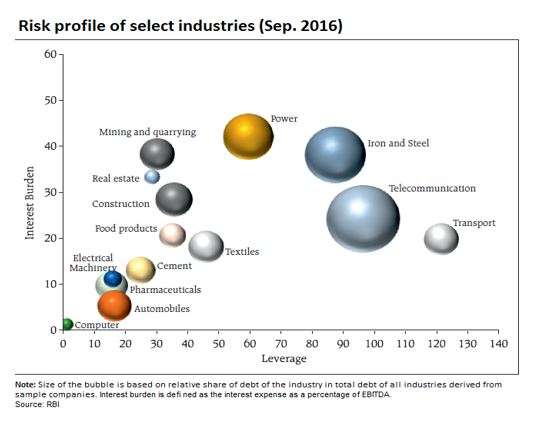

Also, the graph below will tell you about the looming risk in different sectors. When these sectors are doing well, they will sail through. But in stressed times, early identification of stress (using metrics such as interest burden explained in the graph below) would ensure bad loans do not build up over time and are identified and provided for or eliminated early. For example, in the graph below, it is evident that sectors such as telecom and iron and steel not only account for a larger chunk of lending but also carry high interest burden for companies in these sectors.

With banking space being the largest segment in the economy and a driving force for all economic growth, stagnation in this space can lead to prolonged slowdown and a ripple effect in terms of hurting multiple sectors. It is with the intention of curtailing further damage and to revive credit in the economy have the recent measures been implemented.

The extent of the issue

Look at the graph below to understand that it is a few sectors that account for a bulk of the problem. Even within these sectors, the trouble is reportedly from 40-50 large companies in sectors such as metals, infrastructure, power, construction and textiles. According to reports, these sectors account for over 50% of the stressed assets and close to a fifth of the total banking credit. Given the somewhat focused nature (in terms of few sectors and few companies) of the issue, and that it is large companies within these spaces that are stressed, at this juncture, it is not impossible for RBI to assess these (as the volume is not large) and resolve the issues prudently.

What the recent measures can do

The Ordinance combined with the RBI notifications will basically ensure that banks do not sit with poor quality lending for long – without resolving them. This will basically mean that prolonged pain from non-performing assets may be a thing of the past. But that is in the long term.

Selective re-rating: In the medium term though, there can be hits taken by individual banks, based on their NPA levels. However, we think markets may have already factored these in as issues of lower margin, poor lending ratios, capitalisation issues have already been punished by markets. Analyst reports suggest that public sector banks are already at a 25% discount to their average price to book valuations and in fact 55-60% lower than their peak valuations; at a time when the market’s valuation is above average. That means, while there may be individual cases of negative impact based on RBI’s intervention, overall there may not be sector-wide impact. In fact, select corporate banks that were shunned thus far (as markets preferred the retail banks) may see some interest at such low valuations if there is recovery in large lending taking place swiftly with RBI intervention.

Consolidation: However, where there are huge write downs, especially in smaller public sector banks, the question of recapitalising them will arise. Banks such as Indian Overseas Bank, UCO Bank, IDBI Bank and United Bank of India– for instance, have anywhere between 15-22 percent of gross NPAs. Given that the government has earmarked just Rs 10,000 crore overall for these banks for this year, the question of whether these banks may have to be consolidated may arise. And many of these names also figure in the list of banks with very low capital adequacy. The question therefore arises whether banks will go through a consolidation phase.

Consolidation may come outside of banks too. Selling of large assets by some of the stressed sectors may see few players commanding a bigger chunk of the market pie in their respective sectors. This too may mean a re-rating or de-rating in those sectors and stocks.

What to expect

We are already beginning to see earnings downgrades by several large broker institutions citing expensive valuations in sectors which were over-rated or are expected to see more shocks. For example: the metals and oil and gas space rallied on strong commodity price expectations but the actual price trend turned out to be more tepid. The rupee played spoilsport to estimates of IT, pharma and to some extent the oil space earnings. The banking space may see higher provisioning coming from the requirement of providing more for stressed sectors.

These, together with a huge clean up act in banks could mean quite a bit of volatility in the markets for the next 3 quarters at least. While domestic liquidity and global news have kept the Indian market sentiments high, investors should not get too carried away by the good news.

The opportunity may lie where the news is least positive. Fund managers, of course, will keep looking for those opportunities. Rejigs in portfolios may happen at multiple levels:

- Funds that are underweight on banks may increase their exposure to select undervalued stocks

- Funds that have stayed away from corporate banks may now take selective exposure

- Some funds may take selective exposure to public sector banks if recovery action is swift in certain cases

- Sectors such as metals and oil and gas, where we felt there was potential (earlier this year) may no longer see a sector approach. The opportunities may become very stock specific

- Funds may choose to hold selective contrarian bets in IT and pharma or play the consolidation theme in sectors where distressed assets are sold

As investors, your job would be to invest steadily and temper expectations at this stage as the Bharat Banking system and consequently many other sectors get cleaned up. Do not try to second guess the market-favoured sectors or stocks. Instead, focus on investing in quality funds and holding them for long term.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis for investment decisions. To know how to read our weekly fund reviews, please click here.

{kind=link}