If you are among the many FundsIndia investors who have started investing in mutual funds in recent months, here’s a ‘Playbook’ for all of you. It is simply about how we can, together, play the mutual fund game right! Playing the game this way will make your investing life simpler and needless to say, richer.

It’s a ‘long-only’ game

While mutual funds are not just about equity funds, you need equities to generate wealth in the long term. If you decide to invest in equity funds, long is the only way. Else, it is best to stay away.

Every time you feel confident that you can invest in mutual funds for a year, think of a year like 2008 when the markets fell much more than 50 per cent. That means you would have lost half your money and not recouped it at all (because you came in with a 1-year time frame). To add to it, you would probably shun this efficient wealth-building product forever, simply because you had a wrong time frame for it.

There are multiple fund categories in debt to suit you short-term needs. Go for it if you need money in the near term.

The long game means STAYING INVESTED

An elementary point, but not many seem to get it, going by the investment behaviour of many investors who do not hold their equity funds for even 6 months. Believe me, you cannot exit a fund even for poor performance in that short frame of time!

Added to it, the market fluctuations can easily force you to exit your fund, or stop your Systematic Investment Plans (SIPs), making you take decisions in fear. Avoid the fear (when market falls), or the temptation (when market rises) to exit unless you have use for the money. The best you can do is not to watch your fund movements daily. It is the biggest favour you can do for your own self.

Often times, we are so obsessed with returns (and not the actual value of money) that we lose sight of the wealth we need to build. Suppose you had invested Rs. 1 lakh in a fund, and it gave 60 per cent returns in a single year. Yes, you have Rs. 1,60,000 and you might be tempted to exit. Fine. But what next? Where do you propose to deploy it? Very likely, it will waste away in your savings account.

Instead, letting this money lie for say 10 years will have fetched you over Rs. 4 lakh (assuming a 15 per cent annual return). The question here is not just the returns, but the amount you will have in hand when you actually need it. Staying invested will add ‘wealth’; not just ‘returns’.

Non-stop SIPs

You can stop your SIPs and move to another scheme when a fund is not performing well. Stopping SIPs before your intended tenure with no further investment is the worst you can do for your portfolio.

We can only take a leaf from the fall of 2008 to tell you how much you lose by doing so.

Let us take an example of say Franklin Prima. Had you stopped SIPs by mid-2008 (started in mid 2007) but just held the fund, your returns by December 2009 would have been a measly 0.7 per cent annually (Internal Rate of Return – IRR). Had you continued the SIPs into 2008 and 2009, then by December 2009, your returns, in contrast, would have been 26 per cent annually. This is because the best period to average at low cost was the second half of 2008 and early 2009. By continuing your SIPs, you gave the fund a chance to average at really low market values.

But more than anything else, by stopping your SIPs, you are stopping your investment/saving process for your future, fearing near-term movements. And that means you stop saving for your goals. Avoid that at all cost.

If you are really worried about your fund performance (but do not expect your fund to do well when the market is down), then check with your advisor on whether you should change the scheme.

Risk = loss

Our advisors come across investors who say they are ‘willing to take risk’. They mean that they are willing to buy equity funds for a short period, or are fine with taking risky bets such as a large exposure to mid-cap funds, or sector funds, and so on.

But what does risk mean to you? For most of you, it means more returns. Sorry, risk is simply first about losing money – losing 50-60 per cent in a single year like 2008, and then waiting for a good while to build wealth. Your ability to take risk means your ability to lose money.

Believe me, most of you do not have that kind of risk appetite. A few days’ fall in your fund, and it makes you wonder whether you should redeem, or stop your SIPs. Many of you actually do so. That is a clear indication that you cannot take risks.

When you pick a ready-made portfolio from FundsIndia, or our advisory team customises one for you, we ensure that the risks are contained through right category allocation and asset allocation. When you choose to go overboard with some categories, especially based on the lure of the past 1-year returns, you are entering the risk zone. Read the next paragraph to know how it can be a slippery slope to depend on 1-year returns for your investment decision.

If it is short, it is slippery

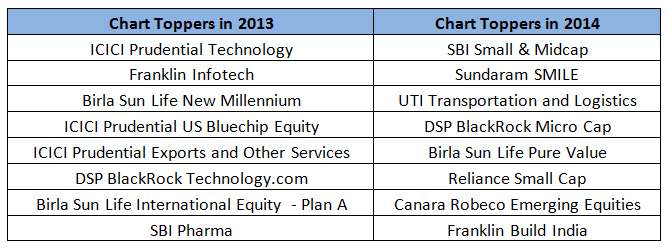

This is true not only in terms of time frame, but also for choosing funds based on short-term performance. Many investors get enamoured by short-term performance, especially when the returns look spectacular. The question is whether such a repeat performance is possible, more so, with sector funds. Look at the table below.

You will be surprised to know that the chart toppers in 2013, especially technology funds, were in the bottom quartile of 2014’s performance chart. Worse still, the international fund that was among the toppers in 2013 delivered just 1.3 per cent in 2014, what with the rupee appreciation also pulling down its returns.

2014 had all mid-cap funds hitting the roofs. But now in 2015, we know that they have already taken a bit of a knock.

So, what are we trying to say here? Go by consistent performers. How will you know a fund is consistent? They would be consistent if they do not swing wildly – that is if they don’t top charts in one year, and hit the dust the next. Of course, this is no easy task for you to decipher, which is why we have our Select Funds list – researched and handpicked after quantitative and qualitative filters.

This is your answer when you ask our advisors why we do not have some ‘top’ fund in our list: They happen to be top that year; that’s all. They are not consistent. They can pull down your returns the next year.

Finally, the playbook essential: If you want to build a lot of wealth, it is easy to do so in calculators, adjusting the annual returns from 15 to 20 to 30 or even 40 per cent. That’s a number game. If you want a lot of money, you need to save a LOT of money and for a long enough period. Elementary, but hard to follow.

While equities certainly deliver superior returns, it is unfair and unreasonable to expect the equity market to create miracles. Instead of upping your return expectations, try to up your savings. SIPs and step-up SIPs are a good way to do this regularly.

While none of us can, nor will we give you any guarantee on how much funds will deliver, I can say for sure, playing by these rules will certainly leave enough in your pocket to play your life – the way you’d like it.

Very Nice Article. 1 year returns are most misleading indicator to chose Mutual Fund.

Question : I have SIP in Hdfc top 200 since 2011. Currently I am not sure shoukd I stop and switch to some other large cap fund as its rating has been decreased in recent years?

Hi Madam,

Thanks for gifting us such a nice article. Specially I liked the section where you mentioned to stay invested in equity for 10 years @ 15% rather to withdraw the amount after 1 year with 60% return.

Madam, I’m also investing in MF through FundsIndia. Till now I’m investing in equity MFs. Currently I decided to move my some of my Bank FDs, Company FDs and Post Office TDs to Debt Funds.

However I’m confused regarding the Debt Funds. There are several debt funds exist in market like Long Term Debt Fund, Short Term Debt Fund, Ultra Short Term Debt Fund, Income Fund, Dynamic Bond Fund, Gilt Fund etc.

If you can share a topic regarding those funds(what is the significance, pros and cons of each type of fund), then it will be better for me to select the proper fund before investing.

Gourab, thanks. I shall re-publish one on debt funds soon. thanks, Vidya

Wow! This is an amazing article.

Yet another excellent article… well explained in simple language.

Hello,

Yet another very nice article, It’s a kind of patience in investing which reaps a hefty returns in future. I personally feel like being consistent and patience based upon your risk appetite will give best possible that market can offer you.

Many thanks for such articles and we follow your each post and rely on FI to keep us on track of wealth building.

Thanks

Satyendra

Thanks Satyendra. We will strive towards helping you in your wealth building mission 🙂 rgds, Vidya

Great article as always highlighting the importance of time in the market rather than timing the market.

Vidya – regarding your comment “If you want a lot of money, you need to save a LOT of money and for a long enough period.”, I’d also like to add that you need to earn a LOT of money to increase your savings potential. One can do that by focusing on developing their skills on a daily basis rather than reading about the markets, funds, news etc., which honestly are time-killers.

Great article as always highlighting the importance of time in the market rather than timing the market.

Vidya – regarding your comment “If you want a lot of money, you need to save a LOT of money and for a long enough period.”, I’d also like to add that you need to earn a LOT of money to increase your savings potential. One can do that by focusing on developing their skills on a daily basis rather than reading about the markets, funds, news etc., which honestly are time-killers.

Hello Yogesh, I think earning more has lot of ‘externalities’ to it. Besides, earning more does not automatically lead to saving more. In fact, evidence suggests that it mostly only leads to spending more 🙂 I would not put it as a top point to build wealth. Regular savings for sufficiently long periods is the key. Here is the article where one of our external writers makes the point: https://blog.fundsindia.com/blog/personal-finance/earning-more-and-more-is-not-enough-to-retire-well-2/7634

Hi Vidya, really thankful for all your wonderful articles and discussions on mutual funds. Few queries from my side.

1) In the case of existing investments value reduced by 30%, is it a better strategy to switch the existing investments to debt or liquid funds for the time being while the new SIPs/investments keep continuing?Or any other better approach to follow?

Hi Vidya, really thankful for all your wonderful articles and discussions on mutual funds. Few queries from my side.

1) In the case of existing investments value reduced by 30%, is it a better strategy to switch the existing investments to debt or liquid funds for the time being while the new SIPs/investments keep continuing?Or any other better approach to follow?

Hello Suresh,

I don’t quite get your query. If you mean you need to withdraw and park your money temporarily, then liquid funds are good. If you wish to book profits in equity and reallocate assets then go for long-term debt funds such as income funds. This you need to do only if you equity allocation has gone way ahead of where you started with. For instance you had a 70% equity allocation and itis now 75% or more then rebalance. thanks, Vidya

I think it all three factors are EQUALLY important – earning more, saving more, and having a long term plan. People should constantly look for ways to increase their earning capacity – via skill upgrade, acquiring new skills, having multiple sources of income etc. I think most of the ‘personal finance’ articles focus primarily on savings. One can only save practically up to a certain percent of their income, and hence increasing the income is becomes a key factor.

Hi Madam,

Thanks for gifting us such a nice article. Specially I liked the section where you mentioned to stay invested in equity for 10 years @ 15% rather to withdraw the amount after 1 year with 60% return.

Madam, I’m also investing in MF through FundsIndia. Till now I’m investing in equity MFs. Currently I decided to move my some of my Bank FDs, Company FDs and Post Office TDs to Debt Funds.

However I’m confused regarding the Debt Funds. There are several debt funds exist in market like Long Term Debt Fund, Short Term Debt Fund, Ultra Short Term Debt Fund, Income Fund, Dynamic Bond Fund, Gilt Fund etc.

If you can share a topic regarding those funds(what is the significance, pros and cons of each type of fund), then it will be better for me to select the proper fund before investing.

Gourab, thanks. I shall re-publish one on debt funds soon. thanks, Vidya

Very Nice Article. 1 year returns are most misleading indicator to chose Mutual Fund.

Question : I have SIP in Hdfc top 200 since 2011. Currently I am not sure shoukd I stop and switch to some other large cap fund as its rating has been decreased in recent years?

Wow! This is an amazing article.

Yet another excellent article… well explained in simple language.

Hello,

Yet another very nice article, It’s a kind of patience in investing which reaps a hefty returns in future. I personally feel like being consistent and patience based upon your risk appetite will give best possible that market can offer you.

Many thanks for such articles and we follow your each post and rely on FI to keep us on track of wealth building.

Thanks

Satyendra

Thanks Satyendra. We will strive towards helping you in your wealth building mission 🙂 rgds, Vidya

Hi Vidya, really thankful for all your wonderful articles and discussions on mutual funds. Few queries from my side.

1) In the case of existing investments value reduced by 30%, is it a better strategy to switch the existing investments to debt or liquid funds for the time being while the new SIPs/investments keep continuing?Or any other better approach to follow?

Hello Suresh,

I don’t quite get your query. If you mean you need to withdraw and park your money temporarily, then liquid funds are good. If you wish to book profits in equity and reallocate assets then go for long-term debt funds such as income funds. This you need to do only if you equity allocation has gone way ahead of where you started with. For instance you had a 70% equity allocation and itis now 75% or more then rebalance. thanks, Vidya

Great article as always highlighting the importance of time in the market rather than timing the market.

Vidya – regarding your comment “If you want a lot of money, you need to save a LOT of money and for a long enough period.”, I’d also like to add that you need to earn a LOT of money to increase your savings potential. One can do that by focusing on developing their skills on a daily basis rather than reading about the markets, funds, news etc., which honestly are time-killers.

Hello Yogesh, I think earning more has lot of ‘externalities’ to it. Besides, earning more does not automatically lead to saving more. In fact, evidence suggests that it mostly only leads to spending more 🙂 I would not put it as a top point to build wealth. Regular savings for sufficiently long periods is the key. Here is the article where one of our external writers makes the point: https://blog.fundsindia.com/blog/personal-finance/earning-more-and-more-is-not-enough-to-retire-well-2/7634

I think it all three factors are EQUALLY important – earning more, saving more, and having a long term plan. People should constantly look for ways to increase their earning capacity – via skill upgrade, acquiring new skills, having multiple sources of income etc. I think most of the ‘personal finance’ articles focus primarily on savings. One can only save practically up to a certain percent of their income, and hence increasing the income is becomes a key factor.