The US elections are over, and world markets simply seemed to signal that it’s no big deal, at least for now. What remained a bigger deal at the end of the day, for Indian markets, seemed to be the Indian government’s sudden move to curb the black economy. The latter is a significantly positive move over the long term.

If that is the case, are we ready for a full-fledged rally? We think not. Rather, we think there is still scope for event-based volatility that would afford reasonable averaging opportunities, before the market can take off.

The volatility on the US election result day is a case in point. A few such events would provide bargain buys for you. As investors, if you take advantage of these opportunities, you will likely have more than optimal returns on your portfolio.

Here’s why we think there could be volatile movements in the markets from here to the end of this financial year at least, and moving to even up to the first quarter of the next fiscal.

What’s the Trump plan?

While initial reactions suggest that the markets are unlikely to brood over the shocking success of Donald J. Trump, his nation-building plan and trade policy roll out will be watched for with keen interest; not only by nations but by the FII community as well. Given that there is a vacuum today on any news on this aspect, we believe some amount of reaction by the US market itself and by FIIs is inevitable when the story unfolds.

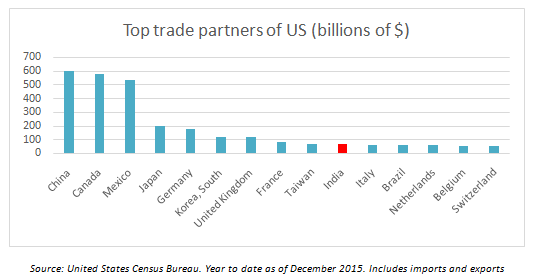

As far as India is concerned, while our trade relations with the US are far lower compared with other nations (see data on left), we rank 9 in terms of imports by US from India. IT and pharma being key Indian sectors that export to the US, it remains to be seen if Trump’s protectionist policies, if any, will hurt these sectors. To this extent, any news on this front may see reaction by the market. The roll out of plans on trade and international ties may also see FIIs reshuffling their portfolio, causing some short-term volatility.

As far as India is concerned, while our trade relations with the US are far lower compared with other nations (see data on left), we rank 9 in terms of imports by US from India. IT and pharma being key Indian sectors that export to the US, it remains to be seen if Trump’s protectionist policies, if any, will hurt these sectors. To this extent, any news on this front may see reaction by the market. The roll out of plans on trade and international ties may also see FIIs reshuffling their portfolio, causing some short-term volatility.

Indian economy reset – near term implications

The move to demonetize about 85% of currency in circulation is perhaps among the boldest moves a government can make, to curb fake money and bring black money into the mainstream economy. The positive implications of this in terms of easing inflation and fiscal burden, bringing in more money into the banking system and contributing to economic growth will likely happen over a couple of years.

But in the near term, there is bound to be short-term pain. First, the immediate impact on the cash economy may unfold itself slowly and market reactions could be only post facto. Impact on the real estate sector, jewellery and other luxury commodities would also unfold slowly.

As this would result in some amount of wealth destruction (black money or not, it is still wealth that would have been used by the individual), some amount of lowering of the propensity to consume, especially high-end goods and services – such as consumer durables, auto, travel and leisure is inevitable. Similarly, any dip in real estate activity can have a ripple effect on allied sectors that provide inputs. The market’s sector-specific reaction has also been on these grounds and further correction can be expected where valuations appear stretched.

Corporate earnings and governance

While it may seem that Corporate India has started expanding its revenue in the last couple of quarters, the earnings growth has not kept pace with valuations across market-cap segments. Take the 126 companies from the BSE 200 for which the September quarter results were out (as of Tuesday). The sales growth of 5.7% for the quarter ended September 2016 over quarter ended September 2015, and the earnings growth of 10% for the same period, may seem like a marginal improvement over previous quarters. However, when this universe is split into those companies with market cap of Rs 20,000 crore and below (midcaps), the picture changes. 53 of the 126 companies in this lower market cap segment not only saw lower sales growth (2.9%) but saw their net profits fall in the September 2016 quarter compared to the September 2015. The fall may be steep because of banks, but even after removing banks and financial service companies, some of which made losses, the bottom line fell.

| 126 of BSE 200 companies | Quarter ending Sep 2016 (YoY) | Quarter ending Jun 2016 (YoY) |

|---|---|---|

| Net sales | 5.71% | 0.41% |

| Adjusted PAT | 9.68% | 7.06% |

| 53 of BSE 200 companies* | Quarter ending Sep 2016 (YoY) | Quarter ending Jun 2016 (YoY) |

| Net sales | 2.90% | -6.20% |

| Adjusted PAT | -31.50% | -9.70% |

| *Companies with market cap of less than Rs 20,000 crore. List includes banks and finance companies. Adjusted PAT – adjusted profit after tax, adjusting for one-off income/expense. | ||

Simply put, the earnings have not kept pace with the valuation (P/E in early 30s for midcaps) that this segment is commanding and that means either a segment/stock specific correction or volatility in prices until such time earnings keep pace. Downgrade of earnings estimate, for stocks, by the end of the calendar (to be expected given the very optimistic forecasts made early this year) may also provide correction opportunities.

Impact of GST and the Budget

Even as markets may remain lackadaisical from the above, implementation of GST may see company-specific reactions. For instance, the impact of working capital can be initially significant on companies as all transactions, including stock transfers would be subject to GST. Besides, those companies which had units in certain tax-free ones will also have to pay GST and claim credit on tax paid. This would result in a higher need for working capital that may have impact on the bottom line (again for mid-sized companies) until such time the working capital cycle settles down. This means, further volatility to earnings.

While we do not expect any significant tax disincentives on issues such as capital gain exemption, the weeks leading to the Budget (expected in early February) may also provide some volatility, especially if FIIs book out.

Opportunity to buy

While we don’t think any massive correction can be expected, given the current state of the economy, volatility triggered by the above events can be expected to provide some opportunities for you to average on your holdings.

- For those of you running SIPs on large-cap funds (or diversified funds), we would recommend that you average on those stocks on dips in the next 6 months or run additional STPs on them if you have surplus. We think valuations are more reasonable in the large-cap segment, relative to earnings growth, and they afford better upside now.

- For those wanting to play it safe, funds such as Kotak Select Focus and SBI Bluechip which have relatively lower exposure to sectors such as IT and pharma (sectors that can be impacted from US trade policies) and higher exposure to internal-growth driven sectors can be options. Run weekly STPs until June 2017 if you have lump sums and review further course of action through your advisor. Do note that this is a tactical call and is only in addition to the existing long-term portfolios that you may run or plan to run. Avoid disturbing those.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis of investment decisions. To know how to read our weekly fund reviews, please click here.