Should you wait for the elections to invest in the markets?

The just-concluded state elections have vindicated the market’s stance on the anti-incumbency factor. Even as experts draw multiple scenarios for the 2014 General Elections, what with state elections shaping the permutations and markets remaining euphoric in the short term, all this may not really matter much to you as a long-term equity investor. Why?

Whatever be the outcome, economic reforms and fiscal improvement are the only ways out for any ruling government given the current state of affairs; failing which, the outcome can be too harsh to face for the nation. Hence, while the governance style could change, the direction of reforms may not vary much, come NDA or UPA or a third front.

Yes, sentiments do play a pivotal role in changing the investment climate, both internally and for foreign inflows. To this extent, the State Elections appear to be setting the stage for positive sentiments.

Still, as has historically been the case, markets do not wait for events to happen. They anticipate events and discount them. And here, we are not talking of just the elections; we are talking of the host of domestic macro and market factors that are slowly but steadily turning favourable. So, we are talking of markets reading into these changes.

It is not for nothing that the equity market rallied 14% between September 1 and now – an indication that it was not just anticipating election results (too early then) but reading into early signs of what could be an economic recovery.

And these are some of the conspicuous signs:

– After nearly 10 quarters, GDP growth in the September quarter was marginally higher than expectations. And more importantly, the demand side of the GDP, especially gross fixed capital formation (representing investment demand) and consumption demand grew better than the previous quarter after a slump.

– Inflow of dollars has considerably eased the liquidity tightness and ensured better money availability for short-term borrowing. Huge dollar addition to the forex reserves through the swap window for FCNR (B) and bank borrowing has also helped stabilize the rupee at around Rs 62 to a dollar.

– The current account deficit has drastically fallen to 1.2% of GDP from 6.7% not long ago on the back of higher exports and lower imports.

– FII flows have remain buoyant through 2013, notwithstanding the constant fear of a US tapering.

– While US Fed tapering may be a factor that could continue to weigh on markets, it is widely believed that this has been discounted to a large extent by the debt market, which saw large FII withdrawals in the second half of 2013 thus far.

– While corporate earnings have been lack lustre for several quarters now, the September quarter earnings of Sensex grew in double digits, compared with the 4% decline in the June quarter.

Simply put, the market has been spotting green shoots and making slow moves, punishing itself harshly every time a key data point goes out of kink by a small margin from what it factored.

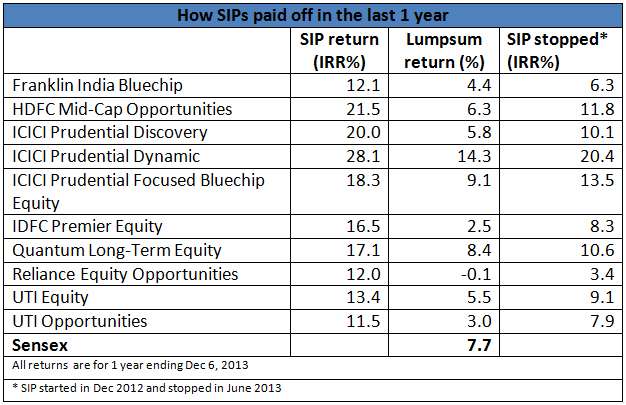

It is such times that provide opportunities for investors to average costs. While you might wonder if the 10% return over the last 1 year is a big deal, you just have to see the data below to know how much more better your SIPs would have done had you been investing over the past one year. The data of some of the schemes from FundsIndia’s Select Fund list shows how SIPs scored over lump sum investing as well as over markets.

And for those who stop SIPs at every high or hope to revive SIPs after there is clarity on the political and economic front, there is a bigger lesson. Just take a look at how your returns would have fared a year ago till date if:

1) You had continued SIPs, and

2) You had stopped SIPs midway in June and just held on to investments made thus far.

Clearly, continuing SIPs generated far superior IRRs than stopping midway and holding on.

The same is likely to play out over the next 6 months at least, based on macro indicators that are flashed every month and until one key sentiment driver – General Elections – play out. Hence, avoid the mistake that you may have made in the last 6 months.

Meanwhile, we will, in the coming weeks, spot some sectors/themes that are likely to lead an economic recovery and identify which funds (diversified and theme funds) are ready to ride such a wave.

Happy investing!

Hello Vidya ma’am. I want to invest a lump-sum of 24 lacs in Large Cap funds like Franklin India Bluechip and ICICI Prudential Focused Bluechip Equity. My time horizon is 10-15 years. I am thinking of doing a STP over 12 months but current all time market highs makes me a little bit hesitant. Should i go for it or should i wait for another 6 months till the General Elections are over?

Thanks

Hello sir, As the article suggests you may miss out on opportunities while waiting. If you are investing systematically and for the long term it is best to kick start. If you need any advice in this regard, request you to complete your FundsIndia account activation so that you can use our ‘Ask Advisor’ feature (under help tab) in your FundsIndia account to seek our advice free of cost. thanks, Vidya

Hello Vidya ma’am. I want to invest a lump-sum of 24 lacs in Large Cap funds like Franklin India Bluechip and ICICI Prudential Focused Bluechip Equity. My time horizon is 10-15 years. I am thinking of doing a STP over 12 months but current all time market highs makes me a little bit hesitant. Should i go for it or should i wait for another 6 months till the General Elections are over?

Thanks

Hello sir, As the article suggests you may miss out on opportunities while waiting. If you are investing systematically and for the long term it is best to kick start. If you need any advice in this regard, request you to complete your FundsIndia account activation so that you can use our ‘Ask Advisor’ feature (under help tab) in your FundsIndia account to seek our advice free of cost. thanks, Vidya