In a move to make choices for investors simpler, SEBI came out with categories with defined criteria. This means that funds within a category will henceforth be mandated to stick to basic tenets of the category. Earlier funds had the freedom to move around categories when it saw the opportunity. Funds will now be more predictable in terms of their strategy and investors will stay more informed about where they are investing. So how do you, as an investor, keep up with this change?

With some categories being renamed and new category names being added, some of you may be confused as to how to match your requirements with the new categories. This article will take you through the changes and where different categories stand relative to each other, in terms of risk and holding period.

Equity

The new categories in equity are either based on market-cap segment or strategy. And that, in turn, determines the risk level of the category.

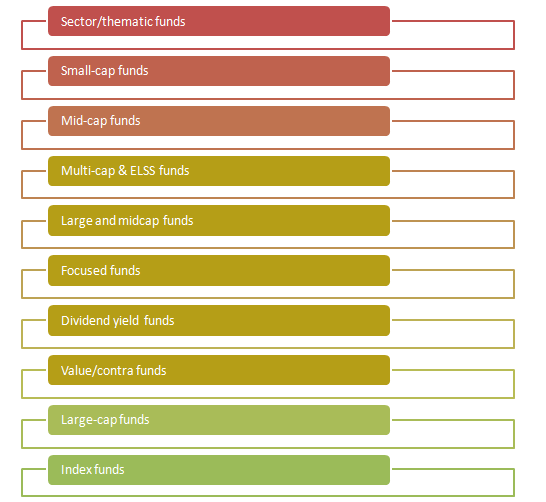

Major categories under equity have remained the same. The diagram below lists the categories in decreasing level of risk (red signifying higher risk and green signifying lower risk). Sector and thematic funds are the most risky because of their concentrated exposure to a sector which requires tactical calls by an investor. Index funds are the least risky as they merely track the broad market indices and are less risky compared to actively managed funds which tend to be more volatile.

As the average market cap of the category goes up, the funds in the category become less risky. Therefore small cap funds with lower average market cap will hold higher risk than a mid or a multicap fund. SEBI has introduced another category in this hierarchy, called ‘large and midcap’ category where a fund should hold at least 35% in large cap and mid cap each. This can result in funds which hold predominantly large cap ( upto 65%) and a relatively smaller portion in midcap (at least 35%) or predominantly midcap (upto 65%) and a relatively smaller portion in large cap (at least 35%) falling under this category. Since the category comprises both of the above, the risk level of the category is more or less the same as multicap. It is essentially above pure large cap and below pure midcap funds. However, some of them may be closer to midcap while others closer to large-cap.

There are additions of other new categories based on the strategy which funds follow. Categories such as focused funds, dividend yield funds, value funds, and contra funds define the strategy that a fund manager needs to follow for funds within the category. Since these funds do not have a market cap restriction, they will behave like a multi-cap fund going into different market cap segments based on the strategy it follows. The risk level of these funds also stand same as multicap funds.

Categories under equity should be looked at only for your long term needs. A period of at least 5 years is required for equity funds to give you optimal returns. In terms of holding period, categories within equity do not differ much. But high risk funds tend to be more volatile and may require a longer time to recover in the event of a market fall and therefore require a slightly longer time frame.

Debt

SEBI has classified debt funds based on two criteria – duration and strategy.

Based on the average Macaulay duration of the underlying instruments, funds have to be bucketed into categories such as, low duration, medium duration, etc. The Macaulay duration calculates the weighted average time before a bond holder would receive the bond’s cash flows. Macaulay duration is slightly lower than the bond’s maturity.

The second way of classification is to classify based on their strategy. For example, funds using low credit rated papers to generate returns will fall under credit risk funds; funds sticking to high credit profile to generate returns will fall under corporate bond and so on.

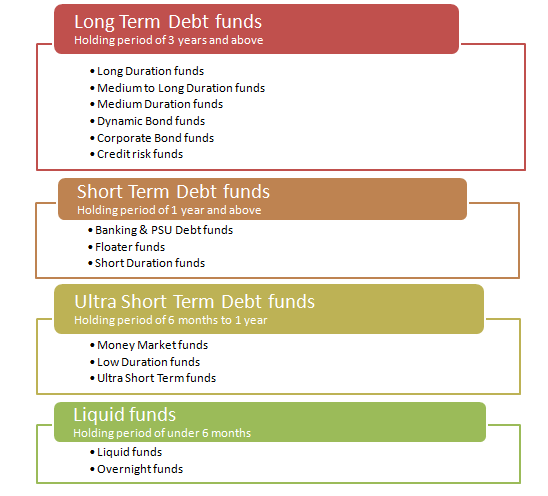

But for investors to align their requirements, we have bucketed the categories in terms of the time frame required for each category. The below diagram classifies the entire universe of debt funds into long term, short term, ultra short term and liquid funds.

Long term debt funds include categories with high average maturity such as long and medium duration funds as well as categories with strategies that require a longer term to play out such as credit risk and dynamic bond. This category requires a holding period of at least three years. These funds should be used only as part of your long term portfolios. They can well witness volatility and even negative returns in the short term.

Short term debt funds include categories which have a Macaulay duration of 1 year or above. These funds should be used when you have a holding period of above 1 year. This time frame requires low risk funds which can provide stable returns.

Ultra short term debt funds include low duration and ultra short term funds which are suitable for holding periods between 6 months to 1 year. These are low volatile funds with shorter maturity. These funds can be used to park money which you will need in the very near future.

Liquid funds are for parking money for really short term requirements such as a few days up to 6 months. These funds have maturity up to 91 days and least volatile. Overnight and liquid funds fall under this category.

Hybrid

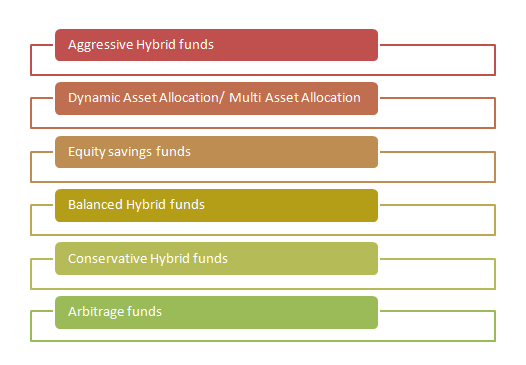

Funds which hold instruments from more than one asset classes will fall under hybrid category. The two most popular categories under hybrid are Balanced funds and Monthly Income Plans (MIPs). These two categories have retained their characteristics with a change in their names. Balanced funds which invest predominantly in equity (at least 65%) and the rest in debt will now be called Aggressive Hybrid funds. MIPs which invest predominantly in debt (at least 75%) and the rest in equity will now be called Conservative Hybrid funds.

Between these two ends of the spectrum fall other categories such as Dynamic/Multi Asset Allocation, Equity Savings and Balanced Hybrid funds.

Dynamic Asset Allocation and Multi Asset Allocation are similar in the sense that asset allocation in these funds are managed dynamically based on market conditions and they do not have to have specified allocation in a particular asset class at all times. Dynamic Asset Allocation manages between equity and debt whereas Multi Asset Allocation will include a third asset class, like gold, commodities,etc.

Equity savings funds have a minimum of 65% in equity and the rest in debt but a portion of their equity will be hedged making it less riskier than aggressive hybrid funds.

Balanced Hybrid funds will have about half their investments in equity and half in debt. This cushion of debt portion brings it in the bottom end of the risk spectrum after Conservative Hybrid funds.

Arbitrage funds continue to fall under equity category for tax purposes. However, the rules now clearly state that they need to hold at least 65% in equity. These funds typically hedge their entire equity position and take some exposure to money market as well. This can be considered the least risky in the hybrid category but with returns that are capped, given their hedged portfolio.