Key Highlights

1. Continuing on the path of Fiscal Consolidation

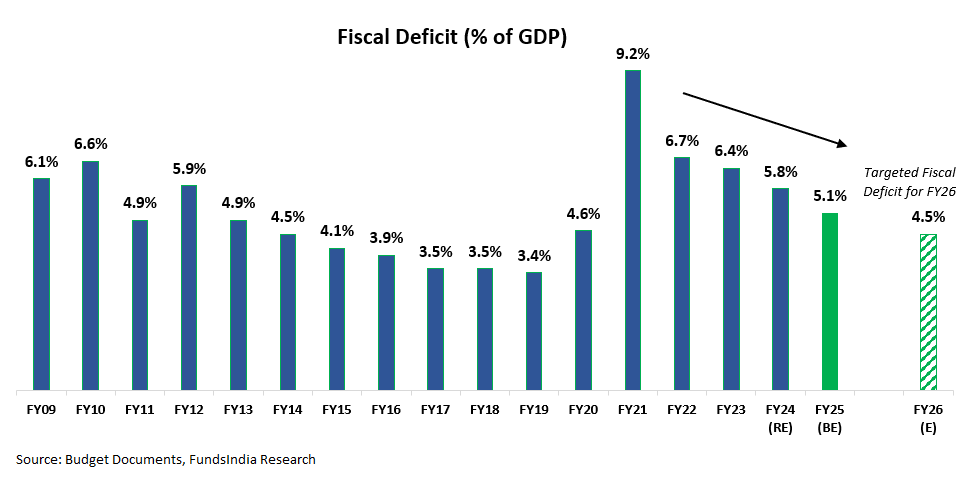

- Projected fiscal deficit at 5.1% of GDP for FY25 – in line with the original fiscal consolidation glide path – to reduce fiscal deficit to 4.5% of GDP by FY26

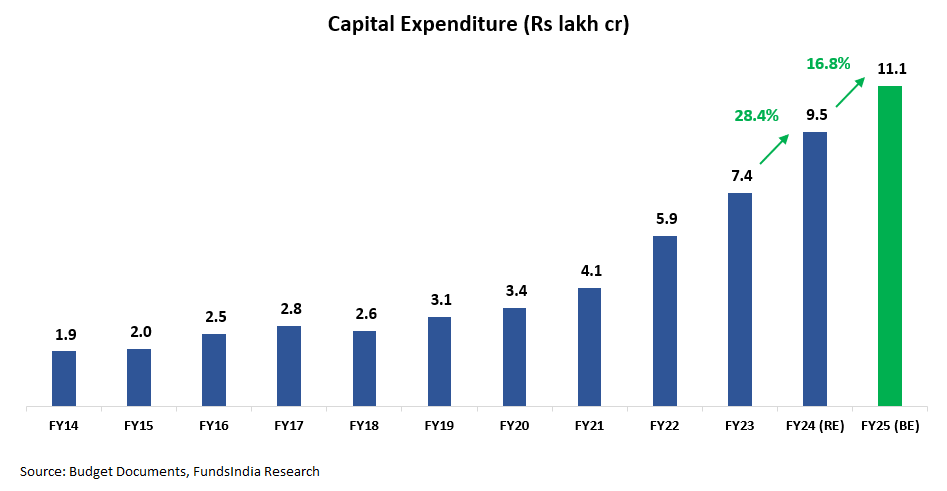

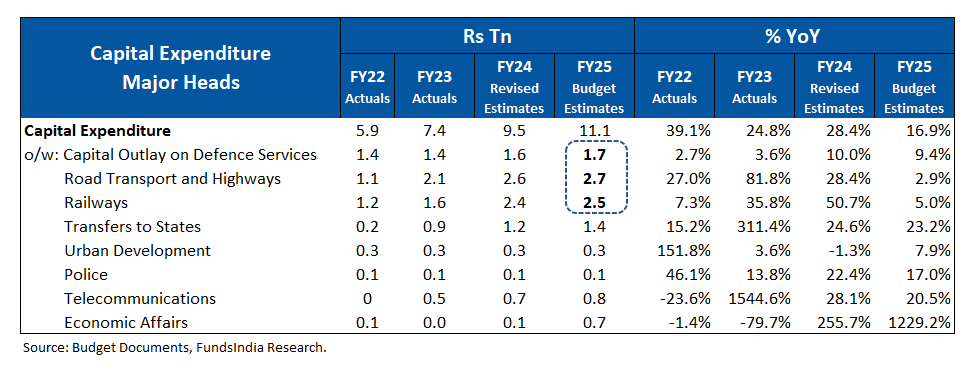

2. Strong thrust on Capital Expenditure (Infrastructure)

- 17% increase in Capital Expenditure from Rs 9.5 lakh cr in FY24 (RE) (i.e 3.2% of GDP) to Rs 11.1 lakh cr in FY25 (i.e 3.4% of GDP)

- Major focus is on: Roads & Bridges, Railways & Defence

3. No change in personal income tax slabs, both new and old regimes to continue

4. No changes to equity and mutual fund taxation

Budget in Visuals

Where does the money come from?

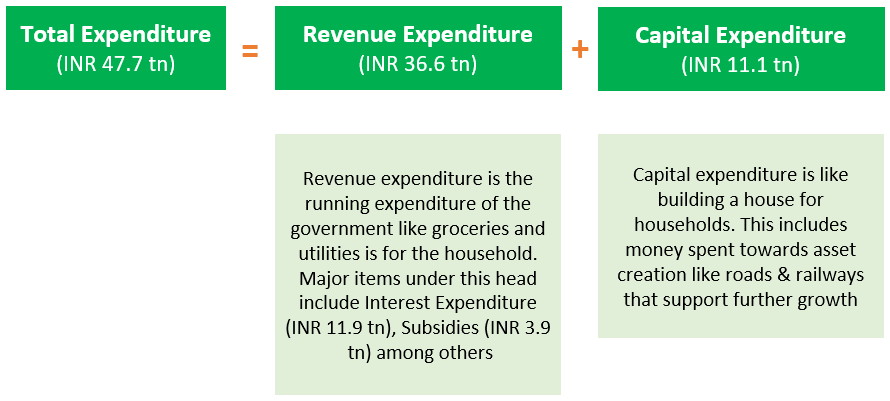

Where does the money go?

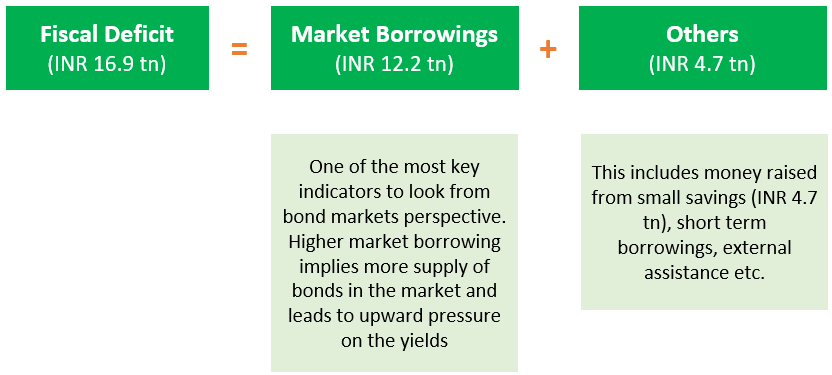

How is the deficit financed?

Fiscal Consolidation On Track

Tax Receipts as a % of GDP remains stable

Thrust on Capex Continues

With a focus on Defence, Roads and Railways

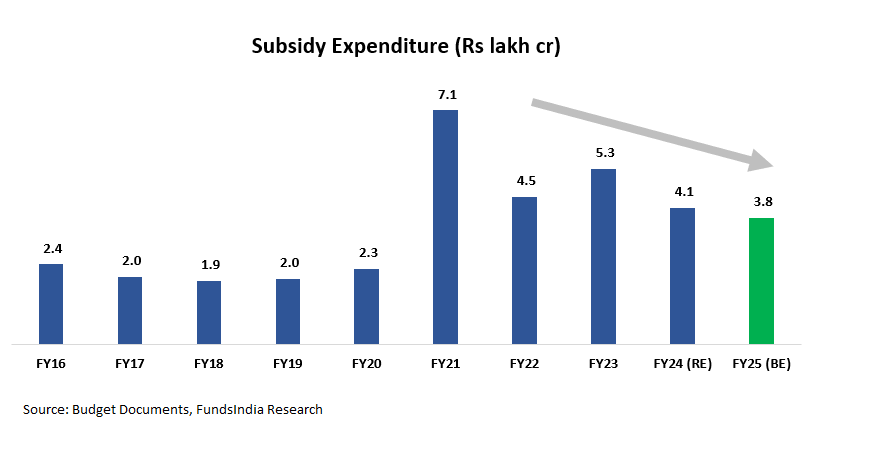

Food, Fuel and Fertiliser Subsidies fall to 5 year low

What’s in it for you?

1. No change in personal income tax slabs, both new and old regimes to continue

2. No change in Taxation for equity, equity mutual funds and other non-equity mutual funds

Equity View: Growth remains the priority – Positive for Equity Markets

The Interim Union Budget FY25 was a non-event for equity markets with no negative surprises.

We continue with our POSITIVE view on Equities with a 5-7 year horizon.

Our Equity view is derived based on our 3 signal framework driven by

- Earnings Cycle

- Valuation

- Sentiment

As per our current evaluation we are at

MID PHASE OF EARNINGS CYCLE + VERY EXPENSIVE VALUATIONS + NEUTRAL SENTIMENTS

- MID PHASE OF EARNINGS CYCLE

We expect a robust earnings growth environment over the next 3-5 years. This expectation is led by Manufacturing Revival, Banks – Improving Asset Quality & pickup in loan growth, Revival in Real Estate, Government’s focus on Infra spending (which continues in FY24 Budget), Early signs of Corporate Capex, Structural Demand for Tech services, Structural Domestic Consumption Story, Consolidation of Market Share for Market Leaders, Strong Corporate Balance Sheets (led by Deleveraging) and Govt Reforms (Lower corporate tax, Labour Reforms, PLI) etc. - VERY EXPENSIVE VALUATIONS

FundsIndia Valuemeter based on MCAP/GDP, Price to Earnings Ratio, Price To Book ratio and Bond Yield to Earnings Yield has reduced from 95 last month to 91 (as on 31-Jan-2024) – but remains in the ‘Very Expensive’ Zone - NEUTRAL SENTIMENTS

This is a contrarian indicator and we become positive when sentiments are pessimistic and vice versa - DII flows continue to be strong on a 12-month basis. DII Flows have a structural tailwind in the form of

- Savings moving from Physical to Financial assets

- Emerging ‘SIP’ investment culture

- EPFO Equity investments

- FII flows continue to be negative. Between Oct-21 and Jun-22, FIIs took out Rs 2.6 lakh cr from Indian equities. Of this, Rs 2.4 lakh cr has come back since Jul-22 – indicates significant scope for higher FII inflows. FII flows can improve in CY24 led by 1. Peaking USD and interest rates 2. May’24 elections and 3. Rising significance of India in global markets.

- Periods of weak FII flows have historically been followed by strong equity returns over the next 2-3 years (as FII flows eventually come back in the subsequent periods).

- IPOs – Sentiments has slowly started to revive with most recent IPOs getting oversubscribed. But no signs of euphoria except for the SME segment.

- Past 5Y Annual Return is at 16% (Nifty 50 TRI) – in line with long term averages and nowhere close to what investors experienced in the 2003-07 bull market (45% CAGR)

- Overall the sentiments are neutral and we see no signs of ‘Euphoria’

Fixed Income View: Fiscal Consolidation continues + Lower Market Borrowing -> Positive for Debt Markets

Fiscal Consolidation continues:

The Fiscal Deficit for FY25 at 5.1% of GDP adheres to the fiscal glide path. The finance minister reiterated the government’s commitment to bring it down to 4.5% of GDP by FY26.

Lower Market Borrowing compared to previous year:

Gross Market Borrowing in FY25 is lower at INR 14.1 lakh crores vs 15.4 lakh crores in FY24.

-> FundsIndia View: Budget is positive for Bonds. Expect interest rates to gradually come down over the next 12-18 months

Why do we expect interest rates to come down?

- Inflation under control:

- India’s Dec-23 CPI inflation at 5.7% is within RBI’s tolerance band (2-6%). Core CPI (excl Food & Energy) remains comfortable at 3.9%. RBI forecasts FY25 inflation to be much lower at 4.5% led by global growth slowdown and broad-based moderation in the domestic core inflation basket.

- India’s Dec-23 CPI inflation at 5.7% is within RBI’s tolerance band (2-6%). Core CPI (excl Food & Energy) remains comfortable at 3.9%. RBI forecasts FY25 inflation to be much lower at 4.5% led by global growth slowdown and broad-based moderation in the domestic core inflation basket.

- Interest Rates well above expected inflation:

- Repo Rate at 6.50% is comfortably above the RBI’s expected inflation (4.5% for FY25) – leaves the positive real policy rates at an elevated 200 bps giving enough room for RBI to reduce interest rates by ~50-75 bps over time.

- Repo Rate at 6.50% is comfortably above the RBI’s expected inflation (4.5% for FY25) – leaves the positive real policy rates at an elevated 200 bps giving enough room for RBI to reduce interest rates by ~50-75 bps over time.

- FED expected to cut interest rates:

- Global growth slowdown & Early signs of US inflation easing increase the odds of FED reducing interest rates

- Fed has already hinted at few rate cuts this year

- Favorable Demand-Supply Equation:

- Demand -> Higher FII inflows -> Indian Government Bonds included in JP Morgan’s global bond market index with expected inflow of ~USD 20-25 bn in FY25 + possibility of inclusion in Bloomberg and FTSE indices

- Supply -> Gross Market Borrowing in FY25 is lower at INR 14.1 lakh crores vs 15.4 lakh crores in FY24.

How to invest?

3-5 year bond yields (GSec/AAA) continue to remain attractive.

We prefer debt funds with

- High Credit Quality (>80% AAA exposure)

- Short Duration or Target Maturity Funds (3-5 years)

Consider tactically investing in a debt fund with a long duration (7-10 years) and high credit quality (>90% AAA) if you have a higher risk appetite and anticipate declining yields over the next 12-18 months. This strategy, with a 1-2 year timeframe, can potentially yield substantial gains in a falling interest rate scenario.