Company Overview

CMPDI is a mining consultancy firm incorporated in 1975 and a subsidiary of Coal India Limited, recognised as one of the largest consultancy service providers in the coal and mineral sector in India. The company offers end-to-end consultancy spanning four business verticals:

1) Geological Exploration and Resource Evaluation (45.8% of 9MFY26 revenue) – Geological mapping, drilling, and resource evaluation.

2) Mine Planning and Design Services (19.7%) – Feasibility studies, mine design, and infrastructure engineering.

3) Environmental Planning and Monitoring Services (17.8%) – EIA/EMP preparation, mine closure planning, and pollution control;

4) Geomatics, Remote Sensing and Survey Services (16.7%) – Drone-based surveys, GIS mapping, and overburden volumetric measurement.

The company operates through seven regional institutes across major coalfield regions, supported by eight laboratories and one of the largest exploratory drill fleets for coal and minerals in India as of March 31, 2025 serving a client base of 76 clients as of December 31, 2025, spanning government bodies, public sector undertakings, and private sector entities.

Objects of the offer

The company is carrying out a 100% book-built Offer for Sale aggregating up to Rs. 1,842.12 crore. The company will not receive any proceeds from the Offer.

The objects of the Offer are:

- To carry out the Offer for Sale of up to 10,71,00,000 Equity Shares by the Promoter Selling Shareholder.

- To achieve the benefits of listing the Equity Shares on the Stock Exchanges.

Investment Rationale

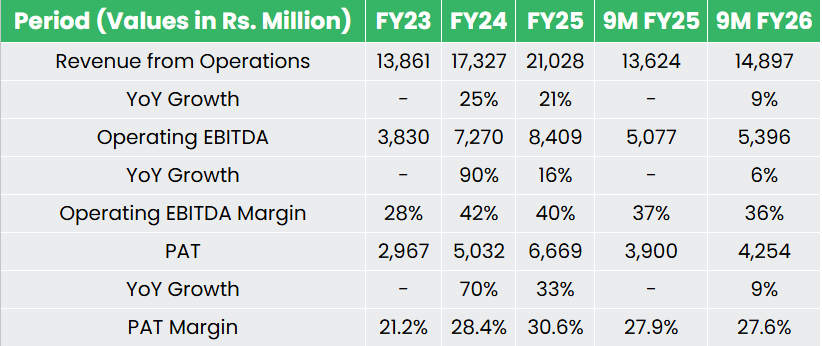

- Dominant Market position with structural demand visibility – CMPDI held approximately 61% market share in Indian mining consultancy in FY2025, with revenue growing at a 23.2% CAGR over FY23–25 against its peers – RITES (-8.1%) and EIL (-3.7%) over the same period. The structural demand anchor is Coal India’s planned capacity enhancement of approximately 787 MT through the opening and expansion of 50 mines by FY2030, each requiring CMPDI’s full-service spectrum before a single tonne of coal can be extracted. NMEDT (National Mineral Exploration and Development Trust) expenditure, a primary source of exploration assignment flow, has grown from ₹831 million in FY2021 to ₹11,140 million in FY2025, with CMPDI among the principal beneficiaries as the nodal exploration agency under the Ministry of Coal. CMPDI’s revenue visibility is effectively policy-mandated, making it one of the few consultancies where the demand pipeline is a function of government targets rather than market cycles.

- Non-CIL client base diversification – Revenue from non-CIL clients has grown 2.9x from ₹2,400 million in FY2023 to ₹6,921 million in FY2025, with external client share expanding from 17.3% to 32.9%, and the active client base expanding from 38 clients as of March 31, 2023 to 76 clients as of December 31, 2025.Two policy developments underpin the sustainability of this trend – 1) MMDR Amendment Act 2020, opening commercial coal mining to private players, resulting in 136 blocks auctioned to date, representing a pipeline of assignments for accredited agencies such as CMPDI; 2) National Critical Mineral Mission (NCMM), with an outlay of ₹163 billion aimed at improving self-reliance in the mining sector, creating a potentially new addressable market for CMPDI’s existing skillset.

- Asset-light model, high-margin operations and strong balance sheet – CMPDI operates an asset light business model with a high degree of operating leverage, evidenced by an annual capex of around ₹419 million in FY25, against FY25 revenue of ₹21,028 million, which implies a capex intensity of under 2%. Employee cost, the dominant fixed cost, has declined in absolute terms from ₹6,919 million in FY2023 to ₹6,085 million in FY2025, compressing employee cost as a percentage of revenue from 49.9% to 28.9% and driving EBITDA margin expansion from 27.6% to 40%. Notably, the company demonstrates strong economic profits, ROCE stood at 48.6% in FY2025, implying a value spread of ~35–36 percentage points (against an estimated weighted average cost of capital of 13%).

- Operational Performance – In FY2025, CMPDI undertook 10.12 lakh meters of exploratory drilling, growing from 6.85 lakh meters in FY23, and delivered 437.9 line kilometres of 2D seismic surveys, marking 87% year-on-year growth. Mine planning project reports submitted declined from 40 in FY2024 to 33 in FY2025 and 5 in 9M FY2026, even as overall revenue continued to grow, suggesting increasing contribution from exploration and geomatics verticals.

- Financial Performance

Operating cash flow converted at approximately 100.6% of PAT in FY2025 and 99.6% in 9M FY2026, reflecting strong earnings quality. Cash and bank balances stood at ₹12,148 million as of December 31, 2025, the company carries no long-term debt, with virtually 0 finance costs, leaving the balance sheet entirely unburdened.

Key Risks

- OFS-Risk – The IPO is entirely an Offer for Sale, implying no primary capital infusion into the business and a partial monetization of promoter shareholding.

- Buyer Dependency and Elevated Receivable Days – Coal India Limited and its subsidiaries accounted for 66.0% of revenue in 9M FY2026, reflecting a high degree of buyer dependency. Trade receivables stood at ₹9,246 million as of December 31, 2025 (~168 receivable days), and the auditor flagged overdue balances from CIL subsidiaries exceeding one year in each of the last three fiscal years, implying a recurring concern.

- Energy Transition Risk – If the energy transition from coal accelerates, CIL’s expansion plans could be curtailed, directly compressing CMPDI’s addressable market.

Outlook

CMPDI occupies a dominant position in India’s mining consultancy. While revenue dependence on a single government group limits pricing autonomy and the long-term trajectory of coal demand introduces uncertainty beyond the medium term, the company remains structurally poised for growth, with an asset-light, zero-debt model, demonstrating consistent margin expansion, with PAT margins widening from 21.2% in FY23 to 30.6% in FY25.

According to the RHP, the company’s listed peers are Engineering India Ltd (EIL) and RITES ltd (RITES). The peer group is trading at an average P/E of 22.6x, with the highest being 25.2x, and the lowest being 19.9x. At the upper price band, the listing market capitalization of CMPDI will be ₹12,280.8 crore, and the company is demanding a P/E of ~18.41x, based on the post issue market capitalization and FY25 diluted EPS. When compared to its peers, the issue seems to be fairly valued. Based on the above views, we provide a ‘Subscribe’ rating for this IPO.

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.