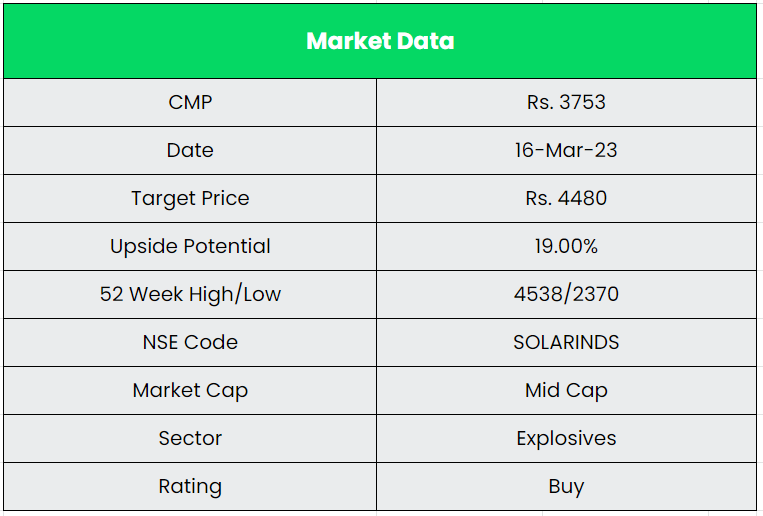

Solar Industries India Ltd. – Explosive Stock

Established in 1995, Solar Industries India Ltd. (SIIL) is the largest manufacturer of industrial explosives and explosive initiating systems in India and has the world’s largest manufacturing facility for packaged explosives. The company initially commenced trading of explosives in 1983 and ventured into explosive manufacturing in 1996. It has more than 25 years of excellence in the field of Explosives. With a licensed explosives capacity of over 300,000 MT/annum, the company has ~30% market share in India.

SIIL, exports to 65 countries around the world with around 36 manufacturing facilities worldwide. Economic Explosives, a 100% subsidiary, manufactures detonators. Apart from India, the company has global manufacturing presence in 7 countries namely Nigeria, Zambia, South Africa, Turkey, Tanzania, Ghana, and Australia. The company further aims to expand to 10 countries in next 2-3 years.

Products & Services:

The company has various products under its two main segments such as Industrial explosives and Defence explosives.

Industrial Explosives – It consists of various products under Packaged explosives, Bulk explosives and Initiating systems. These products are used in several industries like Construction, Mining, Road, Quarries, Tunnelling, Hydro projects, etc.

Defence – Military explosives like TNT, RDX, Ammunitions, etc.; Bombs and warheads for rockets and missiles; warhead for drones and Initiating systems like Ignitors, detonators, etc. are manufactured under Defence explosives.

Subsidiaries: As on 31st Mar 2022, the Company has 6 (Six) wholly owned Subsidiaries and 18 (Eighteen) Step down subsidiaries.

Key Rationale:

- Robust market position – The company is the largest manufacturer of Industrial explosives and explosive initiating systems in India with a market share of ~30% in India. It also leads the exports share from India, which is around 70% in industrial explosives and initiating systems. Solar’s key clientele includes Coal India ltd. (CIL) and its subsidiaries, contributing to ~17-18% of its revenues in the recent years from contributing more than 25%, 5 years back. The company’s diversification process resulted in the reduction of revenue share though the revenue from CIL in absolute value is increasing YoY. Its other major customers are the Ministry of Defence (Government of India), Singareni Collieries Company Limited (SCCL) and infrastructure players.

- Q3FY23 – In Q3FY23, the company had a revenue growth of massive 78% YoY and 16% QoQ at Rs.1812 crs. Explosive segment revenue was up by 71% from Rs.513 crs to Rs.876 crs. Revenue from initiating system was also up by 32% that is from Rs.101 crs to Rs.133 crs. In the explosives segment, the domestic volume in the quarter has increased by 17% that is 1,22,000 metric tonnes compared to 1,04,700 metric tonnes and the realization is up by 46% that is Rs.71,745 tonnes versus Rs.49,000 per tonne. In respect to the customer breakup, revenue from defence sector crossed Rs.100 crs for the second consecutive quarter at Rs.110 crs in Q3FY23, an increase of 51% YoY and it is on the path to achieve the target of Rs.400 crs in FY23. Exports revenue increased by 93% YoY at Rs.729 crs in Q3FY23 which is around 40% of the overall revenue.

- Competitive Advantages – Majority of the raw materials (except ammonium nitrate) such as detonator components, emulsifiers, sodium nitrate and calcium nitrate are manufactured internally (backward Integration), results in cut down in operating costs, quality control and stable EBITDA Margin. The high entry barriers of the explosives industry such as Industrial licenses with multiple clearances, safety clearance from the Government and regulatory bodies acts as a competitive advantage for the company.

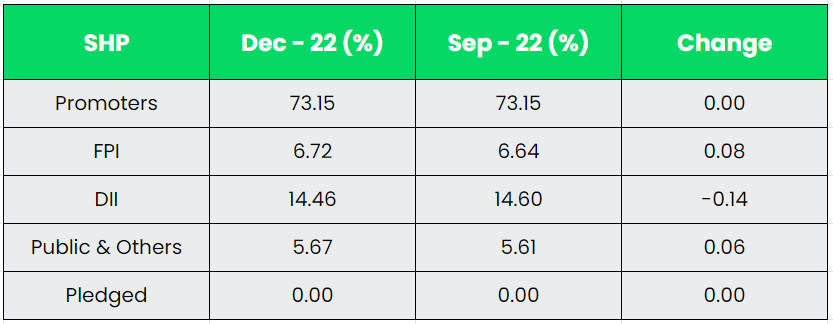

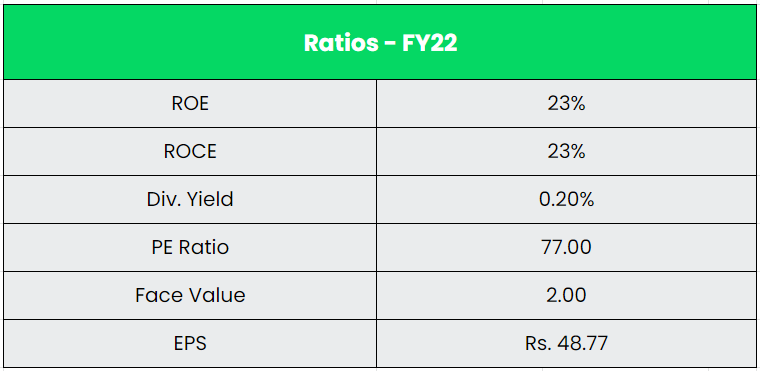

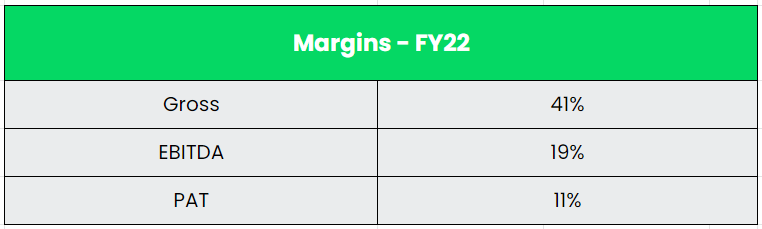

- Financial Performance – The sales grew at a CAGR of 20% for the period of FY17-22 and the profit after tax grew at a CAGR of 19% for the same period. The five-year average value of ROE and ROCE stand at 22% and 23% respectively. The company has a strong promoter holding of more than 70% with a less debt to equity ratio of 0.5x. EBITDA Margin of the company is maintained between 18-22% for the past 7 years.

Industry:

The Indian Defence sector, the second largest armed force is at the cusp of revolution. The Government has identified the Defence and Aerospace sector as a focus area for the ‘Aatmanirbhar Bharat’ or Self-Reliant India initiative, with a formidable push on the establishment of indigenous manufacturing infrastructure supported by a requisite research and development ecosystem. India is positioned as the 3rd largest military spender in the world, with its defence budget accounting for 2.15% of the country’s total GDP. The vision of the government is to achieve a turnover of $25 Bn including export of $5 Bn in Aerospace and Defence goods and services by 2025. Till October 2022, a total of 595 Industrial Licences have been issued to 366 companies operating in Defence Sector. The all-India coal production in the year 2021-2022 was 778.19 MT in comparison to 716.08 MT in the year 2020-2021. Further, in the current financial year up to January, 2023, the country has produced about 698.24 MT of coal as compared to about 602.49 MT during the same period of last year with a growth of about 16%.

Growth Drivers:

- To promote export and liberalize foreign investments, FDI in Defence Sector has been enhanced up to 74% through the Automatic Route and 100% by Government Route.

- Apart from the Atmanirbhar boost for the sector, the government has also put a ban on import of 411 items of Services and total 3,738 items of Defence Public Sector Undertakings (DPSUs) to support the sector.

- In FY2023-24, Ministry of Defence (MoD) has been allocated a total Budget of Rs.5.94 lakh crore, which is 13.18% of the total budget (Rs.45.03 lakh crore). Capital outlay pertaining to modernization and infrastructure development has been increased to Rs.1.63 lakh crore.

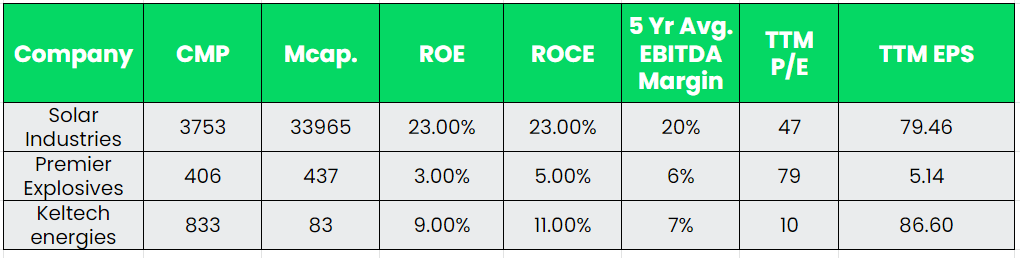

Competitors: Premier Explosives and Keltech energies.

Peer Analysis:

Solar Industries is a market leader with around 30% market share in the explosive industry followed by the other listed players like premier and keltech with a mere ~5% market share each. SIIL is also a strong player in terms of the company size and its financials. The return ratios and other fundamental metrics are strong enough for SIIL to easily outperform its peers in the comparison.

Outlook:

The company has a pending order book of Rs.3389 crs as on Q3FY23. The orderbook breaks into Rs.817 crs from defence and the rest Rs.2572 crs is from CIL and SCCL. The company expects the next contract from Coal India by October 2023 and from Singareni Coal by April 2024. Till then, existing contracts in hand will be executed. The Management has increased the revenue guidance for FY23 to a massive 65%+ growth from the earlier guidance of 45-50%. But the volume guidance remains unchanged at 15-17% for the same period. EBITDA Margins are expected to be hovering around 18-20% in the coming quarters. Capex till 9MFY23 is ~Rs.350 crs and for the current year is targeted at around Rs.450-500 crs and will continue at similar levels for the next couple of years. The company intends to offer its products for space application and it has started generating results after the successful launch of Vikram S and static test of PSOM-XL motors made for ISRO. They also intend to expand it further in the coming years.

Valuation:

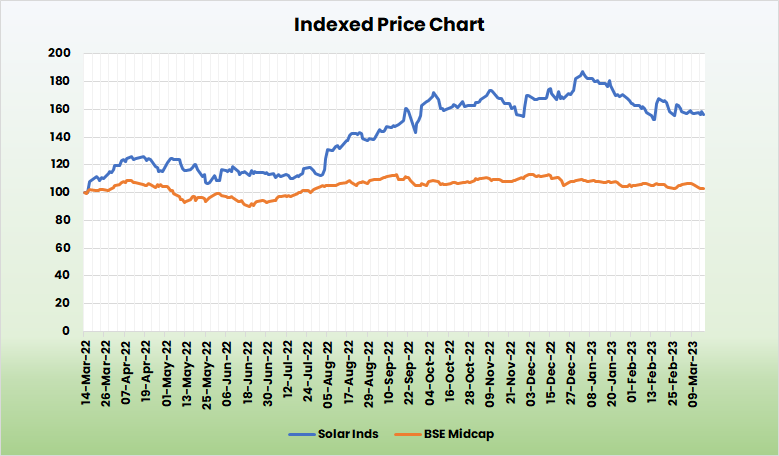

SIIL’s strong experience in explosives industry, robust demand, rising opportunities from the modern defence needs results in a massive earnings growth. We recommend a BUY rating in the stock with the target price (TP) of Rs.4480, 35x FY25E EPS.

Risks:

- Raw Material Risk – Any prolonged volatility in raw material (Ammonium Nitrate) prices, along with the inability to completely pass on higher prices due to stiff competitive intensity, can impact overall profitability.

- Demand Related Risk – Mining and infrastructure are the two key customer segments for SIIL. Any continued slowdown in these could impact the growth in revenues. These two customer segments also face regulatory risks in terms of Govt.’s changing policies.

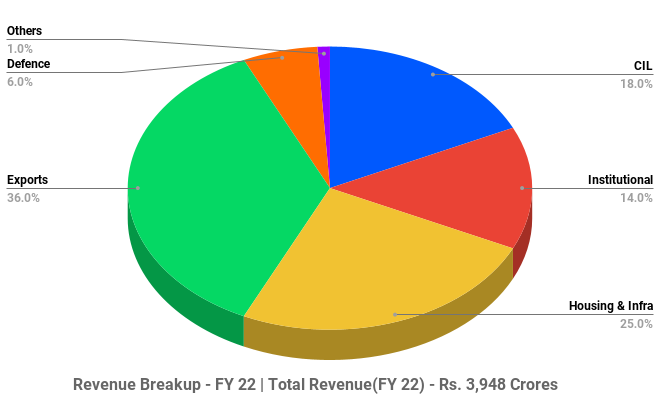

- Forex Risk – Exports and overseas segment contributes the highest with 36% of the overall revenue in FY22 from 50+ countries. So, Foreign exchange fluctuations i.e., any volatility in the currency rates will impact the financial position of the company.