Rainbow Childrens Medicare Ltd. – It takes a lot to treat the little

Rainbow Children’s Medicare Limited (RCML), incorporated in 1998 and headquartered in Hyderabad, is India’s largest pediatric multi-specialty hospital chain and one of the country’s leading perinatal care providers, operating through its “Rainbow Children’s Hospital” (pediatric and neonatal care) and “BirthRight by Rainbow” (obstetrics, fetal medicine and fertility) brands. The group runs an integrated, full-time consultant-led network of 24 hospitals and 5 clinics across 9 cities in 6 states, aggregating 2,435 capacity beds (including the recently commissioned 60-bed HRBR hospital, Bengaluru), organised on a hub-and-spoke model. Its clinical focus spans pediatric secondary, tertiary intensive (NICU, PICU, ECMO) and quaternary care – including pediatric cardiac surgery, haemato-oncology, neurosciences, nephrology and organ transplantation (liver, kidney and bone marrow) alongside comprehensive maternity and fertility services. The network is anchored by JCI-accredited flagship hubs at Banjara Hills, Hyderabad and Marathahalli, Bengaluru.

Products and Services

The services offered by the company fall primarily under two main divisions:

- Paediatric services – Includes newborn and paediatric intensive care, paediatric multi-specialty services, paediatric quaternary care (including organ transplantation) under “Rainbow Children’s Hospital brand.

- Women care services – Under the “Birthright by Rainbow” brand, the company offers services such as perinatal care services which include normal and complex obstetric care, multi-disciplinary foetal care, perinatal genetic and fertility care along gynaecology services.

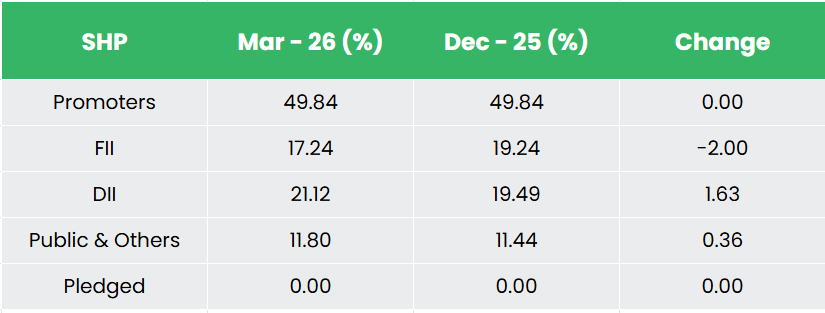

Subsidiaries – As of FY25, the company has 6 subsidiaries and no other joint venture or associate companies.

Investment Rationale

- Capacity Expansion – Platform Built, Execution Phase Begins: FY26 marked one of the most aggressive capacity-building year in Rainbow’s history, with the company adding nearly 500 beds (the highest annual addition on record), taking total capacity to 2,375 beds. This included the commissioning of Warangal (100 beds), Guwahati’s Pratiksha Hospital (150 beds), Rajahmundry (~100 beds), Electronic City Bengaluru (~90 beds), HRBR Bengaluru (~60 beds), and a dedicated IVF centre in Mahadevapura. With the current expansion cycle now complete, Rainbow’s next pipeline of ~900 beds spanning Gurugram’s Sector 44 hub (~325 beds) and Sector 56 spoke (~125 beds), Coimbatore (~130 beds), Pune (~150 beds), Seegehalli Bengaluru (~80 beds), and Indore (~100 beds) is in active execution, with most facilities targeted for commissioning in the next 1-3 years. The Gurugram projects alone carry an estimated incremental capex of ₹400 – 500 crore, while the remaining pipeline is guided at ~₹65 – 70 lakh per bed. Critically, management confirmed that the full pipeline will be funded through internal accruals, with a cash and liquid investment balance of ~₹594 crore and zero debt on the balance sheet as of March 2026, eliminating near-term equity dilution risk. Bengaluru’s build-out – now six hospitals, one OPD clinic, and two dedicated fertility centres positions Rainbow as the largest paediatric and perinatal care network in the city, validating the hub-and-spoke replication thesis beyond Hyderabad.

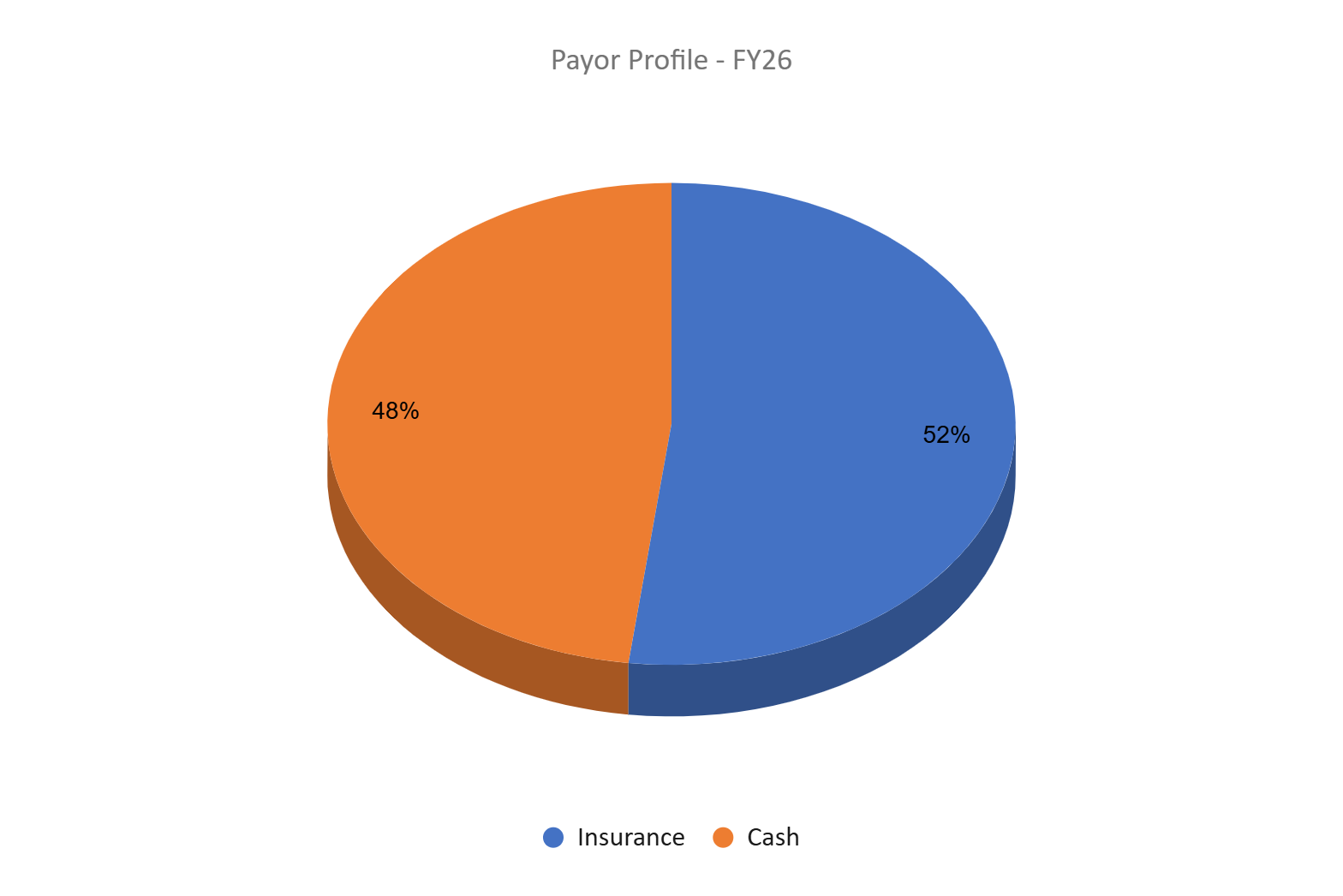

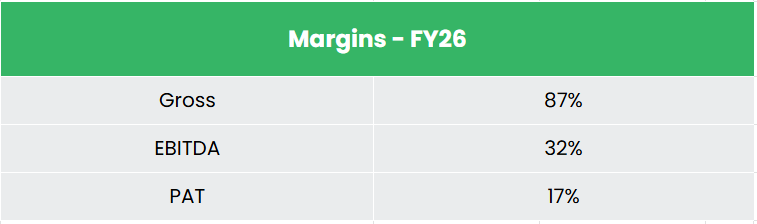

- Operational Metrics – Volume Momentum Intact Amid Dilution from Ramp-Up: Rainbow’s volume trajectory in Q4FY26 reflects a business operating with healthy underlying demand – inpatient discharges grew 18% YoY, outpatient consultations 19%, and deliveries 22%, with organic IP discharge growth at ~9 – 10% and the balance from acquired units. ARPOB expanded 8% YoY to ₹62,464, supported by a richer case mix, an increasing share of obstetrics (~32% of revenue vs. ~28 – 30% historically), and a fast-growing IVF business that contributed ₹61 crore in FY26 (3.7% of revenue, rising to 4.1% in Q4) and is guided to grow ~25% annually over the next three years. Occupancy at 46.3% for FY26 is optically lower than FY25’s 50.5%, but the 427 bps decline is arithmetic – the company absorbed ~440 incremental weighted operational beds through the year; mature hospitals exited Q4FY26 at ~52% and management is targeting a recovery to ~60% for the mature cohort in FY27, with blended network occupancy guided at 56 – 57%. ALOS at 2.71 days is structurally lean, and operating cash flow conversion at ~72% post-tax confirms that margin and cash quality have held – EBITDA margin stood at 31.5% in Q4FY26 despite ramp-up drag from six newly commissioned hospitals.

- Q4FY26 – During Q4 FY26, the company reported consolidated operating revenue of ₹460 crore, up 24% YoY from ₹370 crore in Q4 FY25. EBITDA rose 26% YoY to ₹145 crore from ₹115 crore, with EBITDA margin expanding to 31.5% from 31.0%, aided by a richer case mix, higher quaternary/surgical complexity and a growing fertility contribution. Net profit grew 38% YoY to ₹78 crore, though adjusted for a one-time deferred-tax credit (~₹13 crore relating to subsidiary Rosewalk) underlying PAT growth was ~17%; the quarter was supported by broad-based volume growth (inpatient discharges, outpatient volumes and deliveries up 18%, 19% and 22% YoY respectively), an 8% rise in ARPOB, and the ramp-up of newly commissioned units (Rajahmundry, Electronic City, and the Mahadevapura IVF centre) alongside the integration of the acquired Warangal and Guwahati hospitals.

- FY26 – During FY26, the company reported consolidated operating revenue of ₹1,703 crore, a 12% YoY increase over ₹1,516 crore in FY25, with EBITDA up 11% to ₹544 crore at a broadly stable 32.0% margin (vs 32.3%) and net profit up 15% to ₹282 crore.

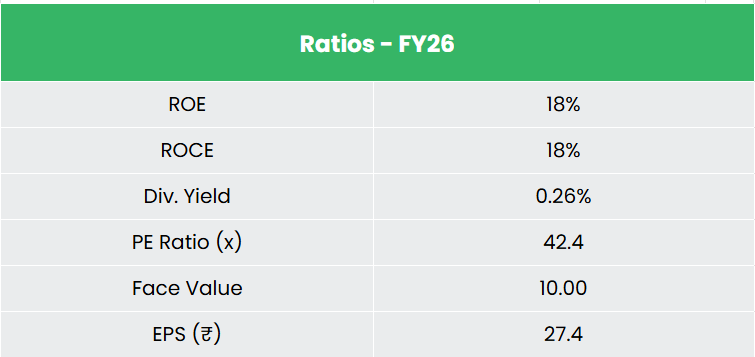

- Financial Performance – The 3-year revenue and net profit CAGR stands at 13% and 10% respectively between FY24-26. The company has a debt-to-equity ratio of 0.54. The 3-year average ROE and ROCE are around 18% and 19% for FY23-25 period.

Industry

The Indian healthcare sector is among the fastest-growing segments of the domestic economy, supported by favourable demographics, rising income levels, and improving access to medical services. The sector is has seen unprecedented growth in the recent years, driven by expansion across hospitals, pharmaceuticals, diagnostics, and digital health. Within this, the hospital segment remains the largest and most capital-intensive vertical. Healthcare spending in India continues to trend upward, with total expenditure expected to rise from 3.34% of GDP in 2023 to ~5% by 2030, while public sector support remains meaningful, reflected in a ₹1,06,530 crore allocation in the Union Budget FY27. The combination of structural demand growth, capacity constraints, and policy support continues to provide long-term visibility for organised hospital operators.

Growth Drivers

- Capacity Shortfall & Infrastructure Gap – India continues to face a shortage of hospital infrastructure relative to its population, with bed availability remaining below global benchmarks and policy targets. This structural gap, combined with rising utilisation of organised healthcare, supports sustained demand for capacity expansion by private hospital operators.

- Policy Support & Public Healthcare Spending – Government initiatives such as Ayushman Bharat and PM-ABHIM, along with a ₹1,06,530 crore allocation in the Union Budget FY27, continue to improve healthcare affordability and utilisation across public and private systems.

- Private Capital & FDI Inflows – The sector benefits from liberal investment norms, with 100% FDI permitted under the automatic route for greenfield projects, and cumulative FDI inflows of US$ 12.73 billion into hospitals and diagnostics between January 2000 and December 2025.

Peer Analysis

Competitors: Global Health Ltd, Krishna Institute of Medical Sciences Ltd, etc.

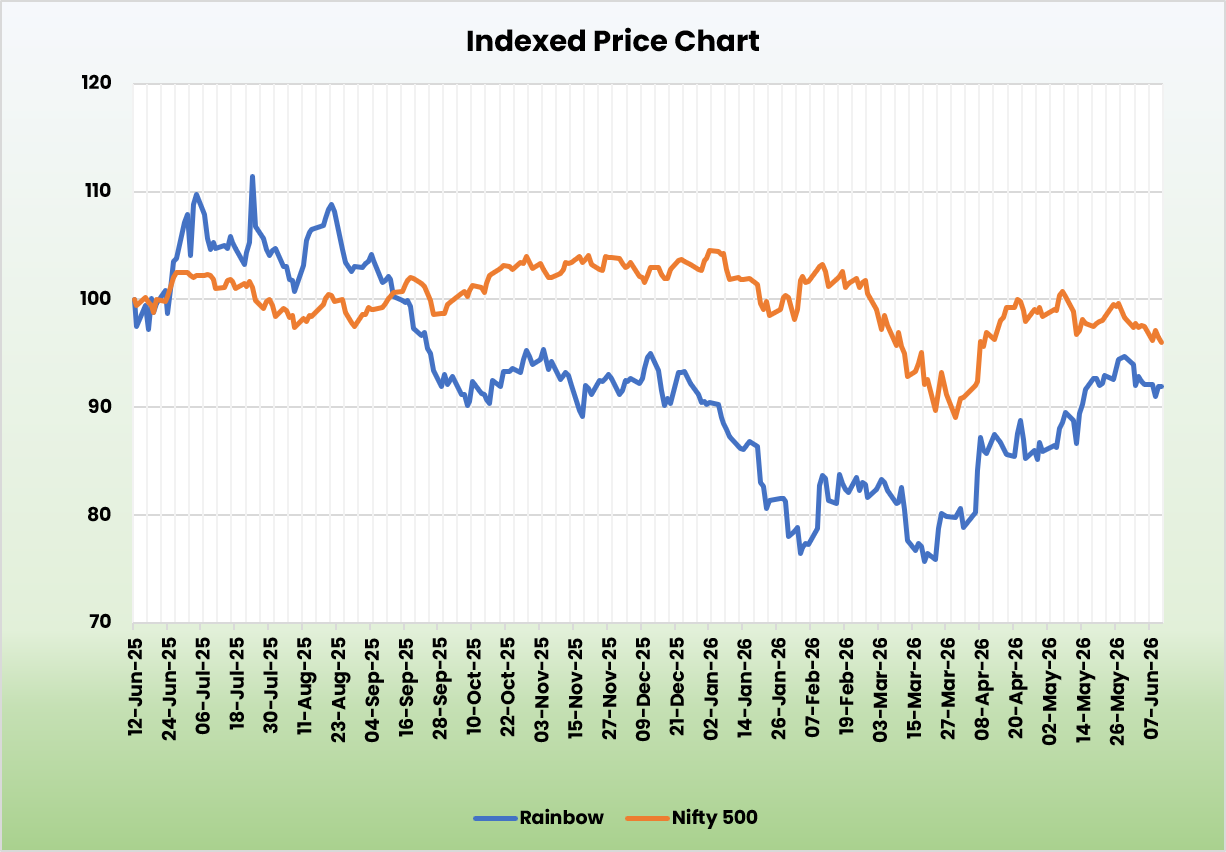

Compared with its peers, Rainbow stands out as the only listed pure-play pediatric and women-and-child hospital chain, with sector-leading EBITDA margins, a net-cash balance sheet, and healthy, un-levered return ratios.

Outlook

Rainbow is at an inflection point – the capital-heavy build-out phase is complete, and the next two to three years are about converting installed capacity into earnings. With mature hospitals targeted at ~60% occupancy in FY27 and a blended network occupancy guidance of 56–57%, operating leverage is the natural next leg of the story. Beyond the core pediatric and perinatal business, Rainbow is deliberately broadening its revenue mix through fertility and IVF services – a segment that contributed ₹61 crore in FY26 and is expected to grow at ~25% annually, adding a high-margin, less seasonal income stream that structurally de-risks the business over time. Geographic diversification into NCR, Maharashtra, and Central India through the ~900-bed pipeline further reduces the South India concentration that has historically defined the company. Management’s guidance of ~17–18% revenue CAGR over a four-year period, backed by a zero-debt balance sheet and self-financing growth plan, provides a credible and low-risk path to value creation.

Valuations

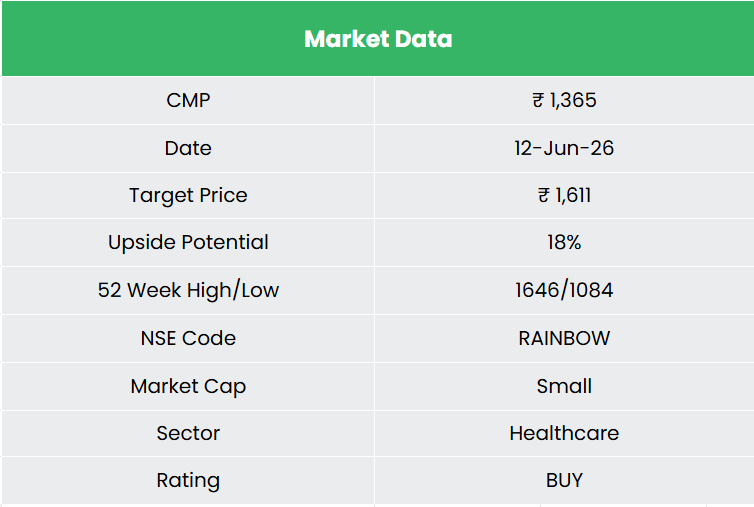

The paediatrics and maternity care market is poised for robust long-term growth, and Rainbow is expected to benefit from this trend given its leadership position and growth-focused business strategy. We recommend a BUY rating in the stock with the target price (TP) of ₹1,611, 50x FY28E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

SWOT Analysis

| Strength | Weakness |

|

|

| Opportunities | Threats |

|

|

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.