Glenmark Pharmaceuticals Ltd. – Redefining the Future

Glenmark Pharmaceuticals Limited, incorporated in 1977 and headquartered in Mumbai, India, is a research-led, global pharmaceutical company with a diversified presence across branded formulations, generics, and innovative biologics through its subsidiary Ichnos Glenmark Innovation (IGI). The company has a commercial footprint across more than 80 countries spanning India, Emerging Markets, Europe, and North America, operates 11 manufacturing sites globally, and employed a global workforce of ~17,000 as of April 2026. Glenmark maintains a focused presence across three key therapeutic areas – Respiratory, Dermatology, and Oncology.

Products and Services

Glenmark’s portfolio spans branded formulations, innovative products, and generics across its three core therapeutic areas of Respiratory, Dermatology, and Oncology.

Subsidiaries – As of FY25, the company has 43 subsidiaries and no other associates/joint ventures.

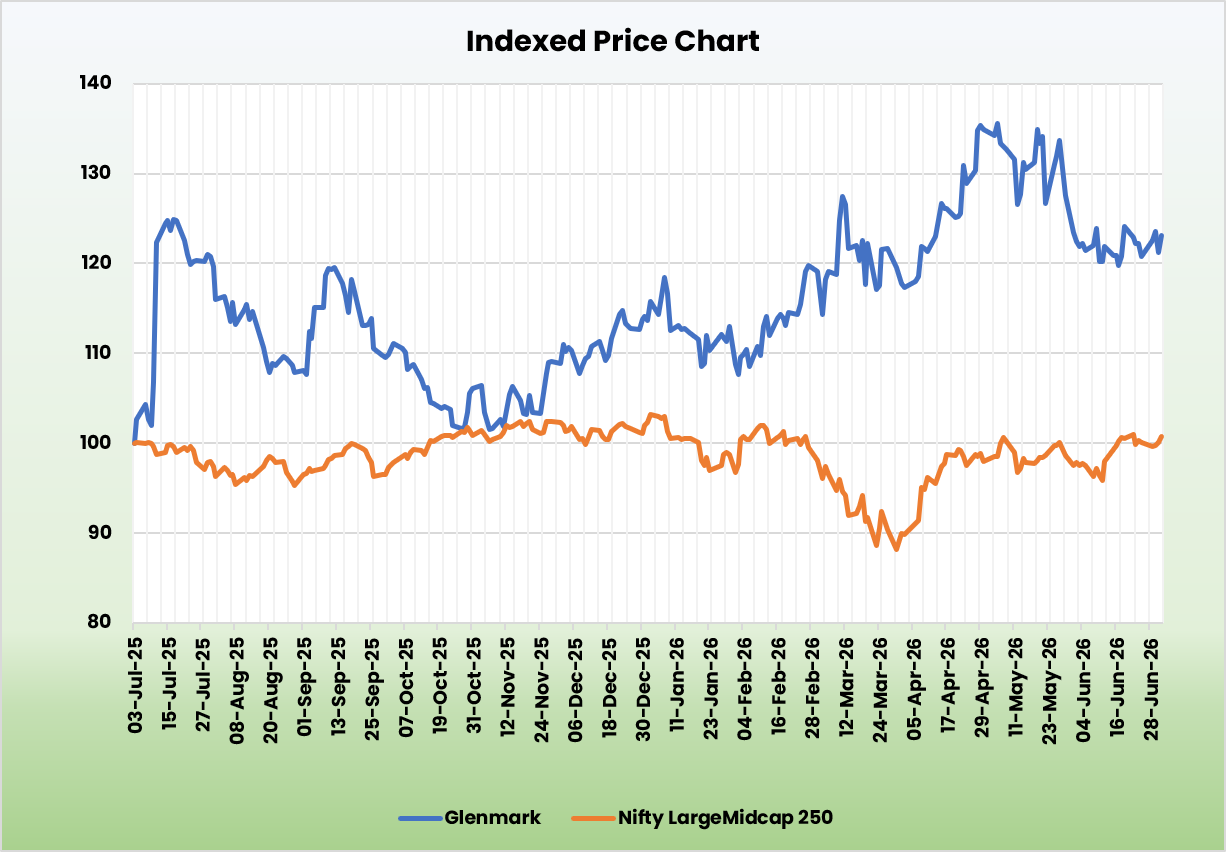

Investment Rationale

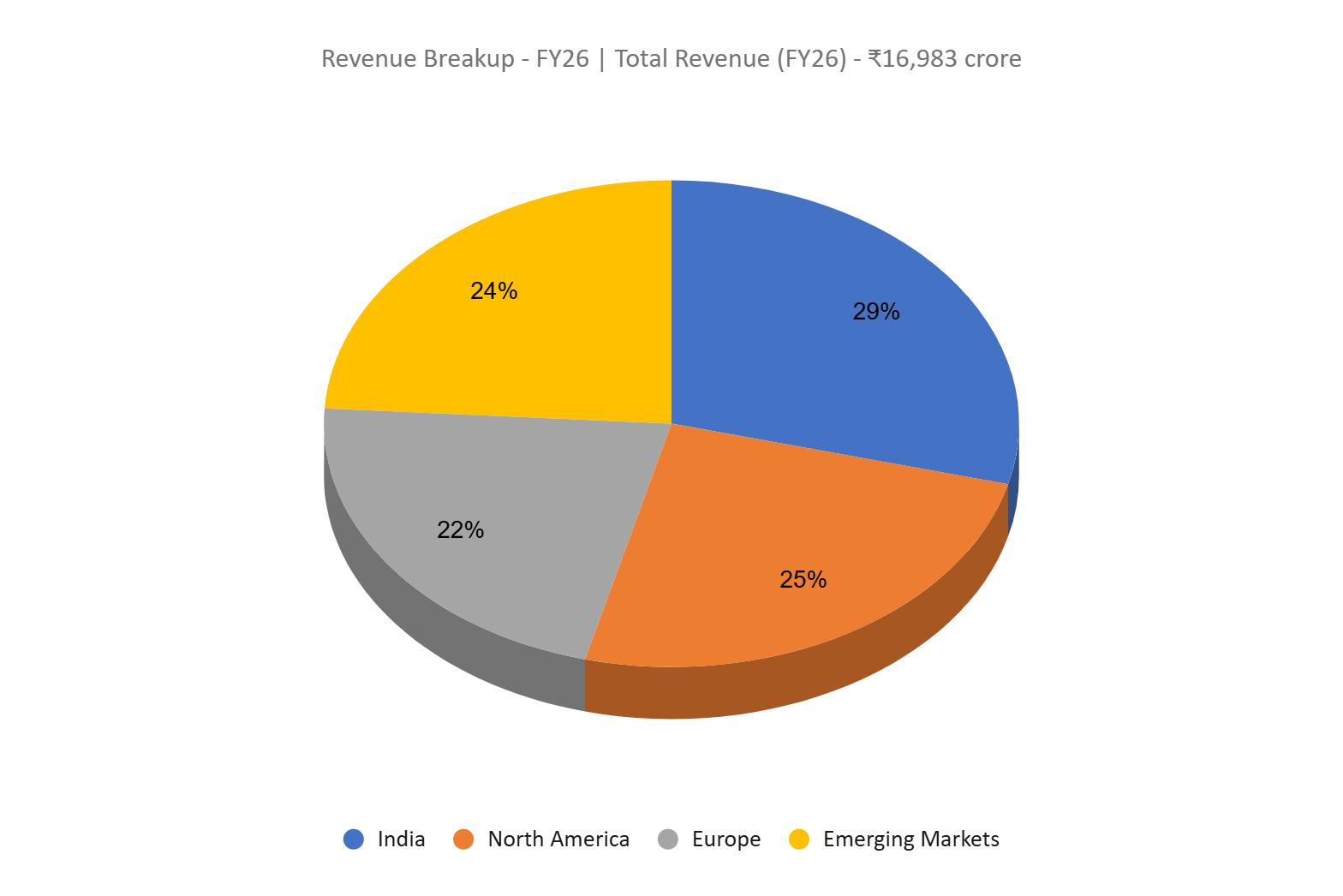

- Diversified Geographic Growth Underpins Earnings Visibility – Glenmark continues to deliver broad-based growth across its key markets, reducing dependence on any single geography while strengthening earnings visibility. During Q4FY26, India formulations revenue grew 8.2% YoY to ₹1,020 crore, with the company outperforming the Indian Pharmaceutical Market (IPM) in secondary sales. Europe and Emerging Markets recorded robust growth of 21.4% YoY and 13.7% YoY, respectively, driven by the strong performance of its branded portfolio. In the U.S., Glenmark launched 13 products during FY26, filed 5 ANDAs, and received an Establishment Inspection Report (EIR) for its Monroe manufacturing facility, enabling the restart of commercial production and supporting future growth in injectables and institutional products. The company’s decision to directly commercialize RYALTRIS in the U.S. is also expected to strengthen market penetration and improve profitability over the medium term.

- Innovation and Specialty Portfolio to Drive Long-Term Value Creation – Glenmark’s strategic shift towards specialty therapies and innovation is expected to enhance its long-term growth profile while reducing dependence on the commoditized generics business. The company’s innovation arm secured a landmark licensing agreement with AbbVie for ISB-2001, valued at up to US$1.93 billion, including an upfront payment of US$700 million, validating Glenmark’s proprietary BEAT platform and creating a significant future revenue opportunity through milestone payments and royalties. Simultaneously, the company is expanding its oncology portfolio through partnerships with Hengrui Pharma and Hansoh Pharma, while strengthening its India franchise with differentiated launches such as TEVIMBRA, BRUKINSA, NEBZMART (the world’s first fixed-dose triple therapy nebulizer for COPD) and GLIPIQ (semaglutide). Additionally, RYALTRIS recorded over 50% growth in global secondary sales during FY26, highlighting the growing acceptance of Glenmark’s specialty portfolio and supporting a more profitable product mix going forward.

- Q4FY26 – On a consolidated basis, Glenmark reported revenue from operations of ₹3,771 crore in Q4FY26, up ~16% YoY from ₹3,256 crore in Q4FY25. EBITDA grew ~36% YoY to ₹763 crore, with margins expanding by ~300bps to 20.2% (17.2% in Q4FY25). Reported PAT stood at ₹301 crore (7.99% margin) versus ₹5 crore (0.14% margin) in Q4FY25; both quarters carried material exceptional charges – largely relating to US antitrust/consumer-protection litigation settlements and other one-off items in FY26, and IGI TSA restructuring and litigation costs in FY25.

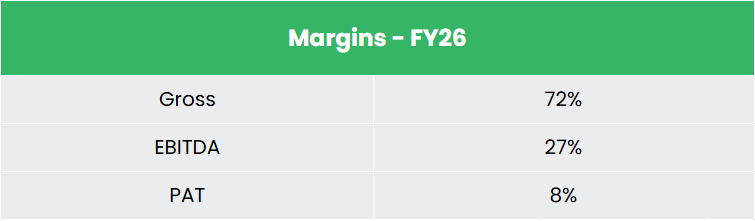

- FY26 – In FY26, consolidated revenue from operations grew ~27% YoY to ₹16,983 crore. EBITDA grew ~94% YoY to ₹4,572 crore (26.9% margin, up from 17.6% in FY25), aided by an improving mix toward branded and innovative products and the contribution from IGI’s out-licensing income. PAT grew ~30% YoY to ₹1,362 crore (8.02% margin, up from 7.86% in FY25), despite the year absorbing ₹2,266 crore of exceptional charges – primarily litigation settlement provisions, post-GST 2.0 inventory-related provisions, and other one-off items.

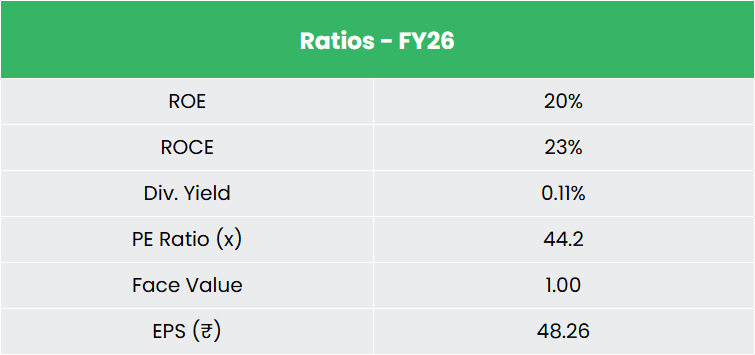

- Financial Performance – The 3-year revenue and net profit CAGR stand at 14% and 76%, while TTM revenue and net profit growth have improved to 27% and 124%, respectively. The 3-year average ROE and ROCE are around -0.8% and 24%, and the company carries a debt-to-equity ratio of 0.06, serviced by an interest coverage ratio of 21.4x.

Industry

The Indian pharmaceutical industry is a global leader in generic medicines and low-cost vaccines, ranking as the world’s 3rd largest market by volume and 14th by value. According to Mordor Intelligence, the Indian pharmaceutical market stood at ₹4,97,000 crore (US$ 57.61 billion) in 2025 and is expected to grow to ₹6,89,000 crore (US$ 79.74 billion) by 2031, at a CAGR of 5.74%. India’s drugs and pharmaceuticals exports stood at ₹2.74 lakh crore (US$ 31.11 billion) in FY26, and the country remains the largest global supplier of generic medicines, providing 20% of world supply alongside 55-60% of UNICEF’s vaccine requirements, underscoring its manufacturing depth and cost advantages.

Growth Drivers

- Increasing Exports & Global Demand – Indian drugs and pharmaceuticals exports reached ₹2.74 lakh crore (US$ 31.11 billion) in FY26, supported by strong demand from NAFTA, Europe, and Emerging Markets, with India remaining the world’s largest supplier of generic medicines (20% of global supply).

- Patent Expiry & Blockbuster Opportunity – Indian pharmaceutical firms have a ₹85,690 crore (US$ 10 billion) opportunity by 2029, as 15 blockbuster drugs with combined revenue of ~₹9,59,728 crore (US$ 112 billion) go off-patent between 2023 and 2029 – a meaningful tailwind for generics- and injectables-led players such as Glenmark.

- Policy Support for R&D & Self-Reliance – The Union Budget 2026-27 proposes a ₹10,000 crore (US$ 1.08 billion) outlay over five years under the ‘Biopharma SHAKTI’ initiative to strengthen India’s biopharmaceutical ecosystem, alongside a ₹60,000 crore (US$ 7 billion) API-push announced in December 2025 to boost domestic manufacturing and cut import dependence.

Peer Analysis

Competitors: Cipla Ltd, Torrent Pharmaceuticals Ltd, etc.

Compared to peers, Glenmark runs a more diversified model spanning branded formulations, US generics, and an emerging innovative-biologics franchise through IGI.

Despite carrying exceptional litigation-related charges, Glenmark’s current-year return ratios rank amongst the best in the peer set, reflecting a lean, low-leverage balance sheet.

Outlook

Glenmark expects FY27 to be another strong year, driven by sustained growth across its core therapies, continued expansion of its branded business and increasing contribution from its specialty and oncology portfolio. The company is targeting revenue of ₹17,000 – 18,000 crore with an EBITDA margin of 21 – 22%, while continuing strategic investments in India and Emerging Markets. Growth in the U.S. is expected to be supported by the respiratory and injectables portfolio, aided by new product launches and the restart of manufacturing at the Monroe facility. The company also plans to advance IGI’s innovation pipeline over the next four to five years while maintaining a debt-free balance sheet, disciplined capital allocation and net working capital of 115 – 120 days, providing financial flexibility to support long-term growth initiatives despite geopolitical and currency-related uncertainties.

Valuations

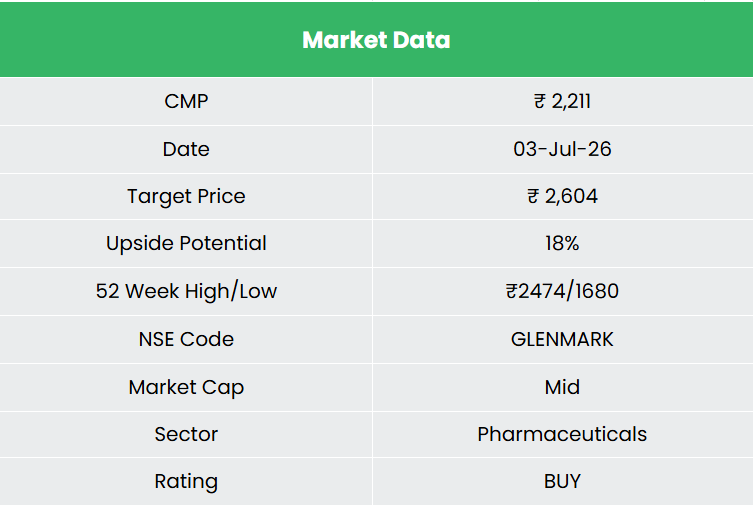

We believe Glenmark’s transition towards specialty pharmaceuticals, coupled with a healthy balance sheet and expanding global footprint, provides a strong platform for future value creation. We recommend a BUY rating in the stock with the target price (TP) of ₹2,604, 33x FY28E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

SWOT Analysis

| Strength | Weakness |

|

|

| Opportunities | Threats |

|

|

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.