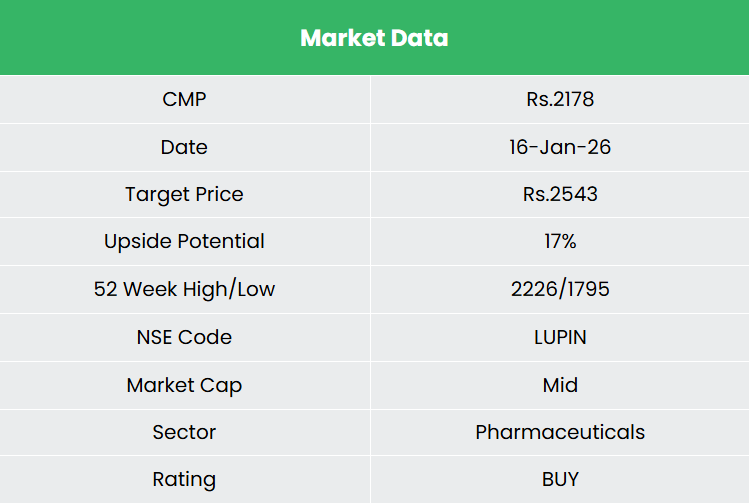

Lupin Ltd. – Healing and Health

Lupin Limited, incorporated in 1983 and headquartered in Mumbai, is an innovation-led transnational pharmaceutical company manufacturing branded and generic formulations, biotechnology products, and active pharmaceutical ingredients (APIs). As of September 2025, Lupin ranks 3rd in the U.S. generic market by prescriptions, and 8th in the Indian market, 4th in Australia, and 7th in South Africa, by sales. The company operates through a geographically diversified business model spanning developed markets including the United States, India, Europe, Canada and Australia, Other Emerging Markets including Latin America, South Africa and Philippines. The company maintains 15 manufacturing sites and 7 research centres across India, the U.S., Mexico, and Brazil, supported by 24,000+ employees and an R&D spend of 7.5% of sales in Q2FY26.

Products and Services

The company operates across the pharmaceutical value chain with a diversified product portfolio

- Therapeutic focus – Cardiovascular, diabetes, respiratory, gastrointestinal, women’s health and tuberculosis.

- Generics – In the U.S., 70%+ of products rank among the top three in their respective segments; in India, multiple brands feature in the top 300 IPM brands.

- Biosimilars – Flagship asset Etanercept, targeting chronic immune-mediated inflammatory diseases; broader pipeline under development.

- Specialty – Focused on women’s health in the U.S. and rare diseases in Europe as core specialty growth areas.

- OTC – Portfolio spans bowel health, women’s hygiene, men’s wellness and personal sanitisation products.

- API – Leading Indian API manufacturer with supplies to regulated markets and government institutions across 70+ countries.

Subsidiaries: As of FY25, the company has 32 subsidiaries and a joint venture.

Investment Rationale

- Global growth engines are driving both scale and earnings visibility – Lupin’s Q2FY26 performance clearly highlights a decisive shift in growth drivers toward higher-margin and more predictable geographies. The U.S. business delivered ~41% YoY growth, driven by specialty and complex launches such as Tolvaptan, Mirabegron and inhalation products, reinforcing that growth is now coming from differentiated portfolios rather than base generics. Other Developed Markets grew ~19% YoY, with Europe outperforming at ~27% YoY, supported by strong respiratory traction (Luforbec®) and providing a strategic base for scale-up post the VISUfarma acquisition in Italy and Spain. Emerging Markets reported a sharp ~45% YoY growth, led by Brazil (diabetes-led turnaround) and South Africa, demonstrating strong operating leverage once portfolios stabilise. In contrast, India grew a modest ~3.4% YoY, impacted by tender volatility and LOE, underscoring why Lupin’s increasing dependence on developed and select emerging markets meaningfully improves earnings quality and reduces cyclicality over the medium term.

- New product launches support growth and margins – Lupin is entering a phase where growth is being driven by complex, high-barrier launches rather than volume-heavy generics, materially improving earnings durability. In Q2FY26 alone, the company reported approvals and launches across complex injectables (Glucagon, Liraglutide, Risperdal Consta®) and biosimilars, validating sustained R&D intensity of ~7.5–8% of sales, among the highest in Indian pharma. Management has outlined ~80 product launches over the next few years, including GLP-1s, respiratory products, long-acting injectables and biosimilars, with over 50 U.S. filings planned, largely in complex categories. Importantly, the injectable portfolio is expected to turn into a meaningful growth driver from H2FY26 and scale into FY27, reducing reliance on any single product. This launch cadence, combined with a higher share of in-house products and declining in-licensed mix, supports structurally higher gross margins and lowers the risk of sharp post-exclusivity earnings compression.

- U.S. growth is increasingly supported by multiple scalable drivers – The U.S. business delivered ~41% YoY growth in Q2FY26, driven by Tolvaptan exclusivity, Mirabegron, Spiriva® and early contributions from complex injectables; however, management guidance indicates that growth sustainability extends well beyond this exclusivity window. Lupin expects to close FY26 with >USD 1 billion in U.S. revenues, with a normalized quarterly run-rate of USD 275–300 million, supported by upcoming launches such as Risperdal Consta®, Liraglutide, Pegfilgrastim and Ranibizumab. The company also plans biosimilars to start contributing meaningfully from FY27, providing a second growth vector alongside inhalation and injectables. Strategic investments in U.S. manufacturing (Coral Springs facility) and supply-chain localisation further de-risk regulatory, pricing and tariff uncertainties. As a result, the U.S. franchise is increasingly underpinned by multiple overlapping growth drivers, reducing earnings volatility and improving long-term visibility.

- Q2FY26 – During the quarter, the company reported consolidated total revenue of Rs.7,048 crore, up 24.2% YoY compared to Rs.5,673 crore in Q2FY25. EBITDA stood at Rs.2,138 crore with a margin of 31.3%, up from Rs.1,308 crore (23.8% margin) in the same period last year, a growth of 63.4% YoY. Net income reached Rs.1,478 crore, up 73.3% YoY from Rs.853 crore in Q2FY25.

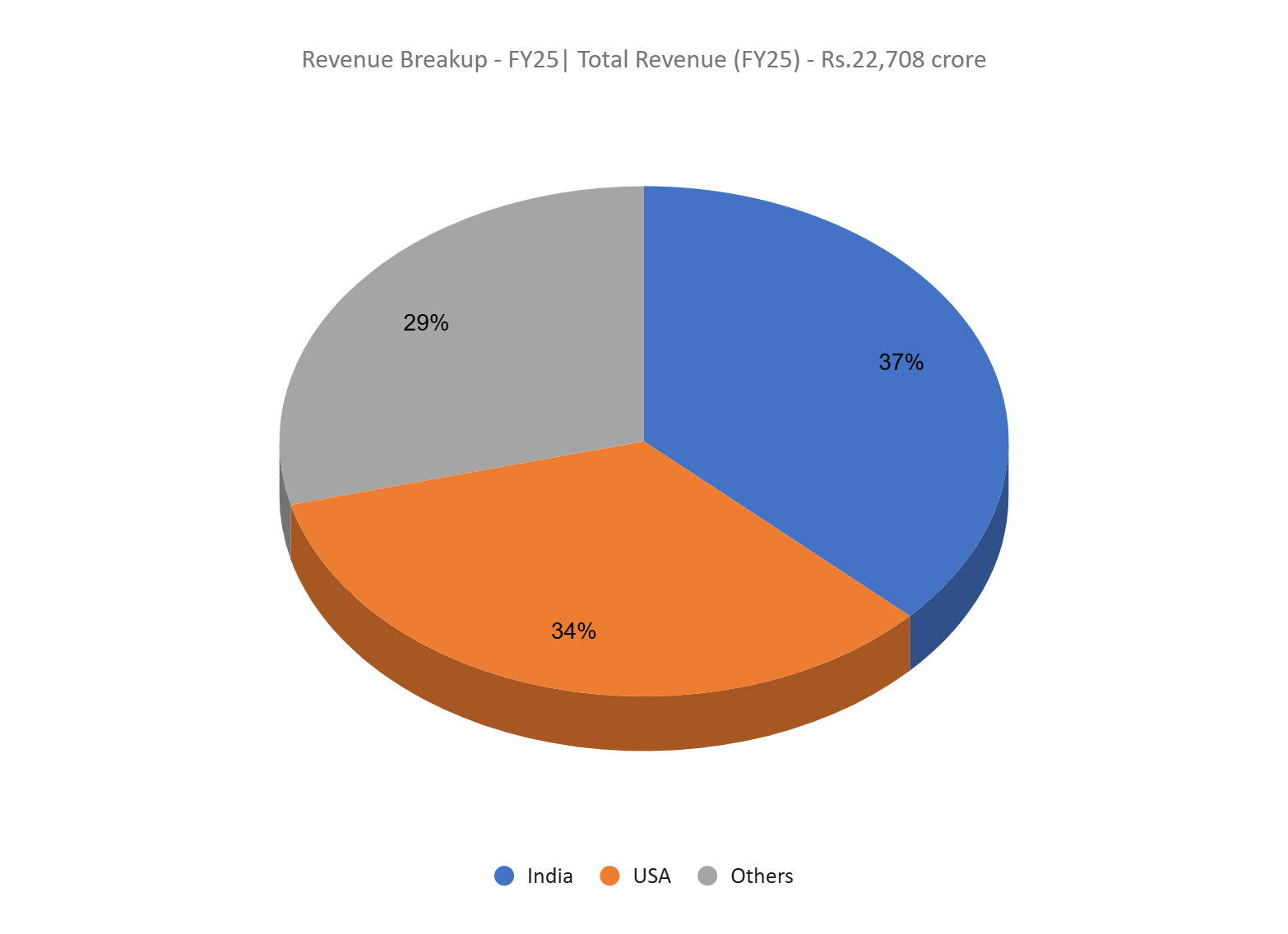

- FY25 – During the FY, Lupin generated net sales of Rs.22,708 crore, up 13% YoY. EBITDA of Rs.5,479 crore, posting a 40% growth over FY24, and net profit grew 71% to Rs.3,282 crore.

- Financial Performance – The 3-year revenue and net profit CAGR stands at 11% and 60% respectively between FY23-25. The company carries a healthy capital structure with a debt-to-equity ratio of 0.32 and the 3-year average ROE and ROCE are around 13% and 14% for FY23-25 period.

Industry

The Indian pharmaceutical industry is the third largest globally by volume and 14th by value, with the domestic market valued at Rs.4,71,295 crore (US$55 billion) in 2025 and projected to reach Rs.10,28,280-11,13,970 crore (US$120-130 billion) by 2030. In August 2025, the industry registered a growth rate of 8.7%, maintaining a robust annual growth trajectory of over 10% for the past five years (2020-25). India is recognized as the “pharmacy of the world,” supplying 20% of global generic medicines and ranking third in pharmaceutical production by volume. The sector’s pharmaceutical exports reached Rs.2,59,658 crore (US$30.38 billion) in FY25, up from Rs.2,43,119 crore in FY24, and are projected to touch Rs.30,76,500 crore (US$350 billion) by 2047. India maintains the second-highest number of US FDA-approved plants outside the U.S. and over 2,000 WHO-GMP approved facilities, exporting to 150+ countries.

Growth Drivers

- Manufacturing incentives and policy support – The Production Linked Incentive (PLI) scheme with an outlay of Rs.15,000 crore (US$2.04 billion) from FY21 to FY29 aims to boost domestic manufacturing of critical bulk drugs, KSMs, and APIs, with Rs.604 crore disbursed in H1FY25 and allocation of Rs.2,444.9 crores for FY26.

- Liberalized FDI framework – FDI of up to 100% is permitted via automatic route for Greenfield pharma projects and up to 74% for Brownfield projects, with cumulative FDI inflows of Rs.2,10,940 crore (US$24.62 billion) from April 2000 to June 2025.

- Policy-led support for the industry – Allocation of Rs.5,268.72 crore (US$ 602.90 million) in the Union Budget 2025-26 towards Department of Pharmaceuticals (DoP).

Peer Analysis

Competitors – Cipla Ltd, Dr Reddys Laboratories Ltd, etc.

Compared to its peers, the company demonstrates strong overall financial performance, and disciplined capital allocation.

Outlook

Lupin is expected to deliver steady growth, supported by ongoing launches in complex generics and injectables, particularly in the U.S. Near-term performance may continue to benefit from recent product introductions, while medium-term visibility is underpinned by a healthy pipeline and planned filings. Margins are likely to remain stable, aided by a gradual improvement in product mix, although higher R&D spending could limit near-term expansion. Growth in Europe and select emerging markets should support revenue diversification over time. Regulatory compliance, pricing pressure and competitive intensity remain key monitorables. Overall, Lupin’s evolving portfolio mix and geographic diversification provide reasonable earnings stability over the medium term.

Valuations

We believe an improving mix and operating leverage are likely to underpin margin resilience despite elevated R&D spends for Lupin. We recommend a BUY rating in the stock with the target price (TP) of Rs.2,543, 31x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

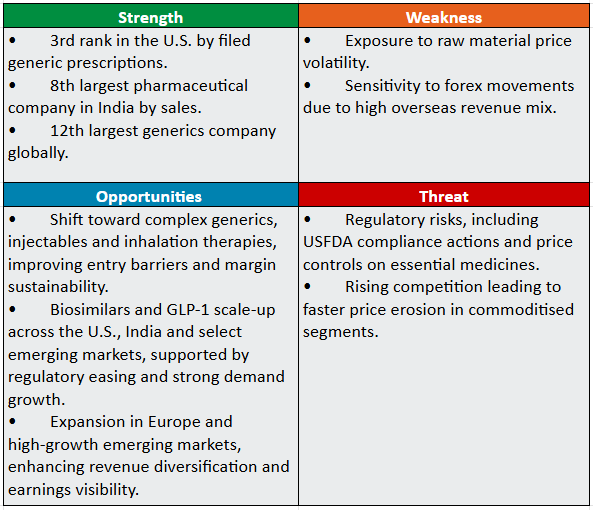

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.