Sharda Cropchem Ltd – Factory-to-Farmer

Sharda Cropchem Limited, incorporated in 2004 and headquartered in Mumbai, is a global, asset-light agrochemical company focused on marketing and distributing generic crop protection products across 80+ countries. Its portfolio spans fungicides, herbicides, insecticides, and biocides, supplemented by a non-agricultural business in belts, dyes and industrial chemicals. The company’s competitive strength is built on its regulatory portfolio of 2,994 product registrations and 1,068 applications under review, enabling scalable participation in regulated markets such as Europe, NAFTA and LATAM. Manufacturing is fully outsourced, ensuring flexibility and cost efficiency with a strong on-ground network of over 525 distributors supporting its Factory-to-Farmer distribution model.

Products and Services

- Agrochemicals – A global portfolio of fungicides, herbicides, insecticides, and biocides, marketed and distributed across 80+ countries, supported by a strong base of regulatory registrations.

- Non-Agrochemicals – Rubber and conveyor belts, dyes and dye intermediates, and industrial chemicals supplied to customers across international markets.

Subsidiaries: As of FY25, the company has 39 subsidiaries and no associates or joint ventures.

Investment Rationale

- Repeatable, asset-light regulatory engine built for scale – Sharda operates a differentiated business model centred on acquiring product registrations for generic agrochemicals in tightly regulated markets such as Europe, North America and Latin America. Instead of inventing molecules or owning manufacturing capacity, the company focuses on building dossiers for off-patent molecules and securing long-term approvals in its own name, then outsourcing production to third-party partners. This approach transforms one-time regulatory investments into recurring, monetizable assets. Each approved registration enables multi-year selling rights, allowing the company to repeatedly scale up product lines across geographies. By targeting molecules with known market demand and piggybacking on the innovator’s expired IP, the company significantly de-risks R&D while maintaining pricing power.

- High-entry-barrier platform with durable operating advantages – The company’s core competitive advantage lies in its regulatory portfolio and global distribution network. Its presence in Europe and NAFTA regions with strict agrochemical regulations offers defensibility against low-cost rivals. Products are registered in Sharda’s name, giving it direct control over approvals and renewals. On the ground, the company reaches 80+ countries through a hybrid model of over 525 third-party distributors and a direct sales team of over 500, allowing efficient scale-up post-approval. Procurement is fully outsourced to long-standing partners, supporting variable cost flexibility. Gross margins of ~34% and improving working capital (stood at 84 days as on 30 September 2025, showing an improvement of 34 days as compared to March 2025) reflect the strength of this platform. Together, the company’s IP assets, sourcing depth and channel control form a repeatable, defensible model with embedded margin leverage as volumes scale.

- Large pipeline and clear earnings visibility – As of H1FY26, the company had 2,994 active registrations and 1,068 applications in progress across herbicides, insecticides and fungicides (in addition to biocides), backed by a planned registration-linked capex of Rs.450 – 500 crore in FY26. This provides a long runway for new product launches and revenue growth across its core geographies. Each approved registration grants Sharda the right to sell that product in the respective market, which it can rapidly monetise through its established distributor and on-ground sales network. In the non-agro segment, comprising mainly conveyor belts and other industrial chemicals, the business operates largely on a made-to-order basis with high customer stickiness and the ability to pass through tariffs, especially in North America, supporting margins even amid volume volatility.

- Q2FY26 – During the quarter, the company reported revenue of Rs.929 crore, up 20% YoY compared to Rs.777 crore in Q2FY25, on account of a strong volume growth of ~35%. EBITDA rose to Rs.139 crore, a 71% increase from Rs.81 crore in the corresponding quarter. Net profit stood at Rs.74 crore, growing 75% YoY from Rs.42 crore in Q2FY25.

- FY25 – During FY25, the company generated revenue of Rs.4,320 crore, an increase of 37% compared to the FY24 revenue. EBITDA was recorded at Rs.682 crore, up by 114% YoY. The net profit grew by 850% to Rs.304 crore.

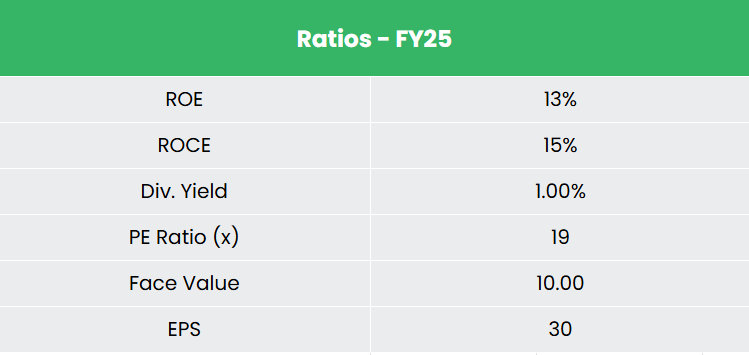

- Financial Performance – The 3-year revenue and net profit CAGR stands at 6% and -5% respectively between FY23-25. Notably, the TTM revenue and net profit growth have improved to 33% and 107%. The company carries no interest-bearing debt. The 3-year average ROE and ROCE are around 10% and 14% for FY23-25 period.

Industry

India’s chemicals industry is a large and fast-growing sector, contributing 7% to national GDP and positioning the country as the 6th largest producer globally and 3rd in Asia. The industry reached US$278.1 billion in FY24 and is projected to expand to US$300 billion by FY28 (5.4% CAGR FY19–28), supported by rising domestic consumption and export opportunities driven by agriculture, construction, automotive, packaging and personal care. Within this, agrochemicals remain a key demand pillar, India being the 4th largest global producer, with the market valued at US$15.5 billion in 2024 and expected to grow to US$23.3 billion by 2033 (4.28% CAGR), while agrochemicals are anticipated to account for ~40% of India’s chemical exports by 2040.

Growth Drivers

- 100% FDI permitted in the chemicals sector under the automatic route.

- Competitive manufacturing base with skilled and lower-cost labour and strong R&D infrastructure (over 200 national labs and 1,300 R&D centres).

- Shift in global supply chains benefiting India as companies diversify procurement away from China.

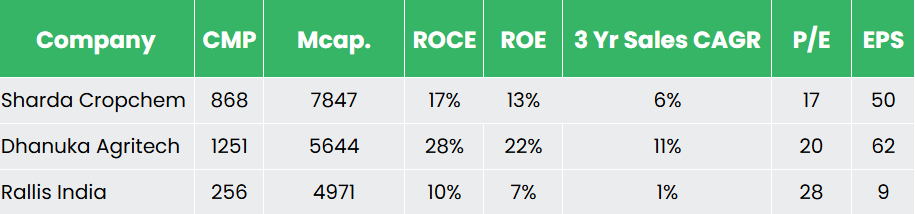

Peer Analysis

Competitors: Dhanuka Agritech Ltd, Rallis India Ltd, etc.

Compared to its peers, the company demonstrates disciplined capital allocation and strong overall financial performance.

Outlook

Management expects performance to improve in H2FY26, consistent with the seasonal uplift seen in the crop protection industry. Gross margins are expected to remain around 34 – 35%, supported by product mix optimization and pricing actions, while EBITDA margins are guided in the 15 – 18% range. The company continues to strengthen its regulatory pipeline, with Rs.450–500 crore in registration-linked capex planned for FY26 to drive future product approvals across key regulated markets. In the non-agro business, particularly conveyor belts with strong exposure to North America, the made-to-order model and ability to pass on tariffs provide margin resilience despite end-market volatility. Overall, the company is poised to sustain its growth momentum in the medium-long term.

Valuation

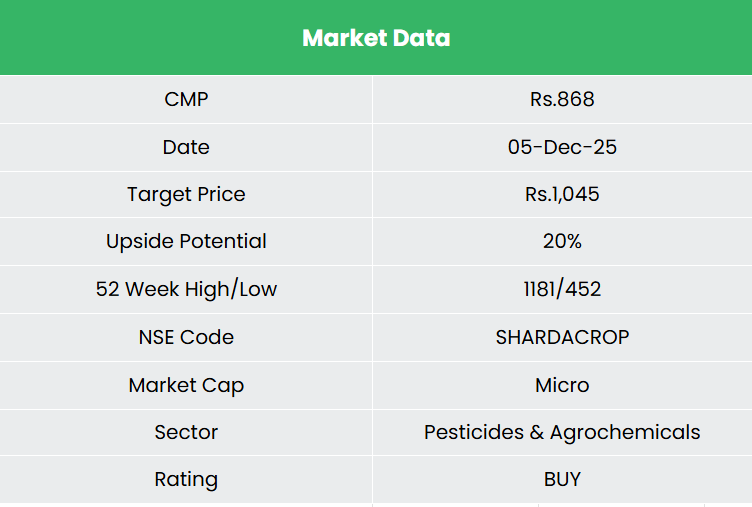

The company’s strong pipeline and market positioning enable it to sustain its growth momentum. We recommend a BUY rating in the stock with the target price (TP) of Rs.1,045, 19x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

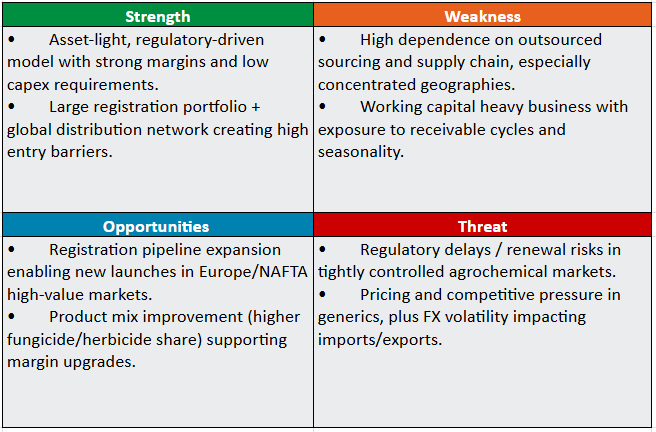

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.