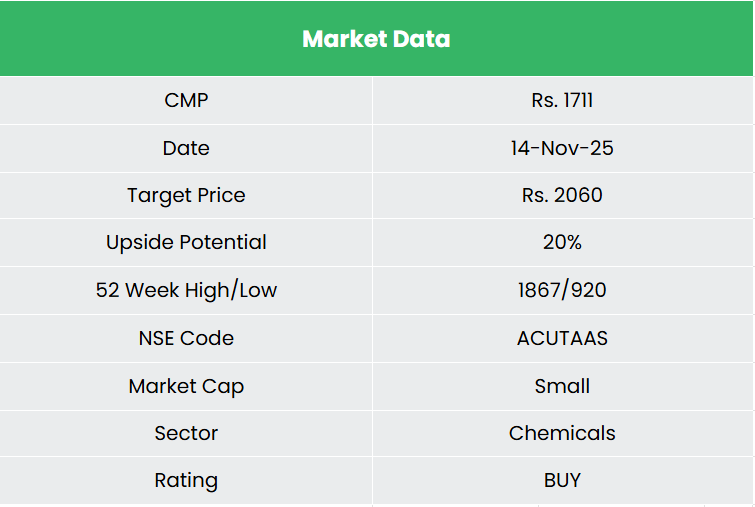

Acutaas Chemicals Ltd – At the Apex of Chemistry

Incorporated in 2007 and headquartered in Surat, Acutaas Chemicals Ltd. (formerly Ami Organics Ltd.) is a diversified specialty chemicals company with a presence across nearly 55 countries. The company is a leading player in chemical manufacturing delivering high-performance solutions for pharma intermediaries, semiconductors chemicals, battery chemicals, etc. As of FY25, it operates 4 manufacturing facilities located in Gujarat and Uttar Pradesh, with a total installed capacity of ~1,100 KL. With a portfolio of over 610 commercialized products, the company leverages strong R&D capabilities and process innovation to deliver sustainable, value-added solutions to its global clientele.

Products and Services

The company’s product offerings can be categorized under the following 2 business segments:

- Advanced pharmaceutical intermediaries – The company creates advanced intermediates for both regulated and generic Active Pharmaceutical Ingredients (APIs) as well as New Chemical Entities (NCEs).

- Specialty chemicals – Supplier of wide range of specialty chemicals to diverse industries such as battery chemicals, semiconductors, agrochemicals, commodity chemicals, cosmetics and polymers.

Subsidiaries: As of FY25, the company has 4 subsidiaries and 1 joint venture.

Investment Rationale

- Entry into new segments – Acutaas is entering high-value new segments through a structured expansion across battery and semiconductor chemicals. In the battery segment, the company has secured multiple customers across geographies, commercialised new products, and is set to begin production of electrolyte additives – an essential input for battery electrolyte solutions – once its ongoing capex is completed in Q4FY26. Market development is already in place, with customer contracts signed and initial revenues expected from FY27. In the semiconductor segment, Acutaas has added customers in Korea, Japan, and Taiwan, backed by new product introductions and the formation of a JV in South Korea with J & Materials Co. Ltd. The JV will manufacture advanced semiconductor chemicals used in photoresist, lithography, and other chip-making applications, with the new plant expected to contribute from H2FY27. These initiatives position the company to tap into structurally higher-margin, value-added growth areas.

- Strong CDMO Pipeline – Acutaas’ CDMO business continues to gain strong traction, with a healthy rise in customer enquiries and multiple new molecules added to the development pipeline. The company aims to deepen its CDMO footprint and is targeting Rs.1,000 crore in CDMO revenue by FY28, supported by a robust and expanding project pipeline. Beyond the already disclosed CDMO project announced last year, three additional projects are expected to be commercialised by the end of the current financial year. For one of these molecules, the company has already supplied validation quantities in Q4FY25, and post regulatory approvals, revenue is expected to commence from H2FY26. With CDMO offering structurally higher margins than the non-CDMO portfolio and execution progressing in line with internal projections, the company remains well-positioned to achieve its FY28 CDMO revenue goal.

- Q2FY26 – During the quarter, the company reported revenue of Rs.306 crore, an increase of 24% YoY compared to Rs.247 crore in Q2FY25. Gross profit rose to Rs.171 crore, up 59% YoY, supported by a gross margin expansion of 1,232 bps to 55.8%. EBITDA increased to Rs.95 crore, nearly 2x the Rs.49 crore reported in Q2FY25, with EBITDA margin improving from 19.8% to 31.1%, aided by a better product mix and operating leverage. The company delivered a net profit of Rs.72 crore, up 91.3% YoY from Rs.38 crore in the corresponding quarter last year. PAT margin expanded from 15.2% to 23.5%, reflecting improved profitability across segments.

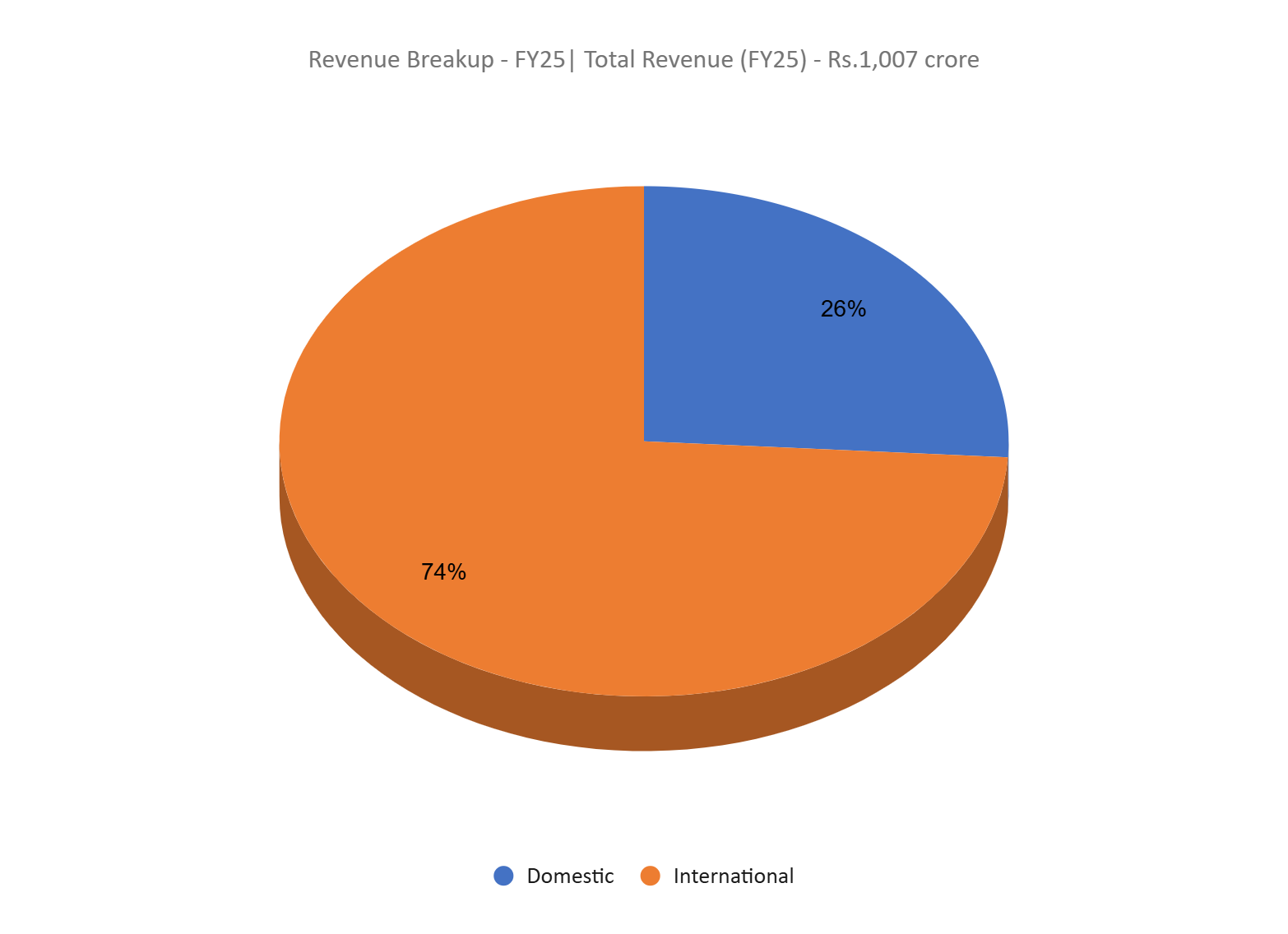

- FY25 – During FY25, the company generated revenue of Rs.1,007 crore, an increase of 40% compared to the FY24 revenue. EBITDA is at Rs.232 crore, up by 81% YoY. The company reported a net profit of Rs.160 crore, an increase of 98% YoY (adjusted for exceptional items).

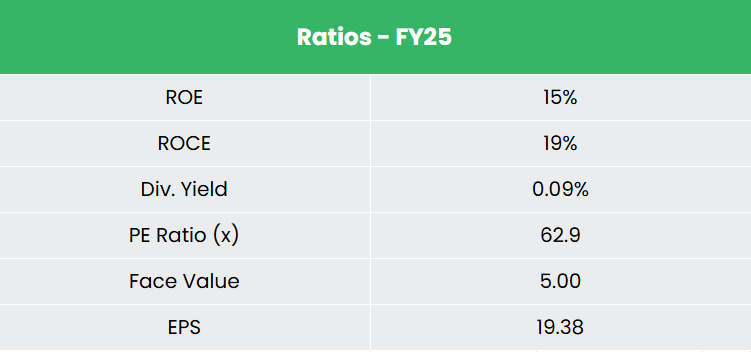

- Financial Performance – The 3-year revenue and net profit CAGR stands at 25% and 30% respectively between FY23-25. The company has a debt-to-equity ratio of 0.01. Average 3-year ROE and ROCE is around 14% and 19% for FY23-25 period.

Industry

India’s chemical industry is entering a phase of sustained expansion driven by rising domestic consumption, accelerating industrial activity, and growing global reliance on India as a diversified and reliable supply base. The sector forms a critical pillar of the economy, contributing around 7% to the nation’s GDP and supplying products to over 175 countries. Supported by a broad manufacturing ecosystem spanning more than 80,000 commercial products, India has steadily strengthened its presence across specialty, agrochemical, and performance-chemical segments. Backed by policy support, increasing FDI participation, and a long-term government vision to build globally competitive chemical hubs through initiatives such as PCPIRs and quality-control reforms, the industry is positioned for multi-year growth. These structural enablers, combined with global supply-chain diversification away from China, are transforming India into a key participant in the worldwide specialty chemicals landscape.

Growth Drivers

- Rising consumption from pharmaceuticals, textiles, construction, packaging, and automotive is driving steady growth across chemical categories, supported by a broad base of 80,000+ commercial products.

- The government allows 100% FDI under the automatic route and continues to develop PCPIRs and enforce quality-control norms to strengthen domestic manufacturing capacity.

- India exports chemicals to 175+ countries, and global firms diversifying away from China are increasing outsourcing to India, supporting specialty chemical growth.

Peer Analysis

Competitors: Akums Drugs & Pharmaceuticals Ltd, Aether Industries Ltd, etc.

Compared to its peers, the company demonstrates strong revenue growth and disciplined capital allocation, as reflected in its consistent sales performance and financial metrics.

Outlook

The management has guided for ~25% revenue growth, supported by a planned FY26 capex of Rs.250 crore, which is expected to be fully funded through internal cash reserves. Of this, around Rs.40 crore is earmarked for maintenance, with the balance allocated toward growth initiatives. Management expects EBITDA margins to remain in the 28–30% range, driven by an improving product mix. A major component of the capex is the Rs.140-crore investment at the Jaghadia site, primarily focused on the electrolyte additives project, while its Sachin facility will see the addition of a new pilot plant. The Jaghadia unit is scheduled to commence operations in Q4FY26, and the Sachin pilot plant is expected to be operational by Q3FY26, reinforcing the company’s medium-term growth visibility.

Valuations

With the management maintaining its guidance on revenue growth and margin improvement, coupled with the timely rollout of expansion projects, we believe Acutaas Chemicals Ltd. offers a compelling investment opportunity. We recommend a BUY rating in the stock with the target price (TP) of Rs.2,060, 44x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

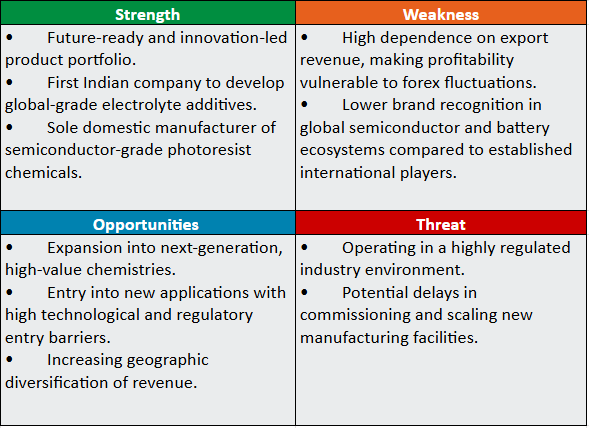

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.