Liquid funds sported high returns through 2018, thanks to higher interest rates and bond yields and a liquidity crunch in the later part of the year. But returns for these funds are now ticking lower, as market rates and bond yields normalise and interest rates head southward.

Rolling their 3 month returns show that liquid funds returns are down more than 10 basis points to 1.74% on an average compared to just 2 months ago. With the market yields falling, it is natural for liquid funds to reflect the same.

What does this mean to investors who are looking to park their short-term money? Should they continue to look to liquid funds? The answer to that question continues to be ‘yes’. The steepness of the change has to do with how they delivered high returns the preceding year and is simply a factor of changing interest rates and yields. Here’s more on the trend.

Changing direction downward

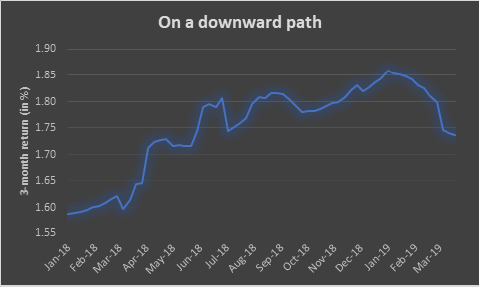

Rate moves are first felt in liquid funds. As they invest in papers which mature between 30 and 50 days, they adjust far more quickly to newer market rates than other debt fund categories. Therefore, it’s easier to see the impact on returns. The chart shows the 3-month rolling return for the liquid fund category since January 2018, and the dip from the climbing returns is clear from the start of this year.

Average 3-month rolling return for liquid funds

The interest rate cycle turned higher in 2018. The Reserve Bank hiked rates in June and August 2018 as inflation concerns mounted. Liquid funds, however, saw their returns improve well ahead. As the markets factored in a shift in stance by RBI, yields of short-term debt instruments were on the rise. By March 2018, 3-month CP and CD yields had crossed the 7% mark. This reflected in liquid fund returns.

In the later part of the year, the debt market went through a turbulent phase after the default of IL&FS. A confidence crisis squeezed liquidity, shrunk lending activity including short-term CP issuances, and sent yields soaring. 3-month CP yields jumped past 8.5% by October 2018. A few liquid funds were hit hard by the default. Others, though, benefitted from higher yields given that liquid funds invest only in short term papers

But with normalising of debt markets, change in rate expectations to rate cuts, and the RBI following through with a cut in January, yields have come down. Regardless of further rate cuts, this put a definitive end to the rapid rise in yields and liquid fund returns peaked out.

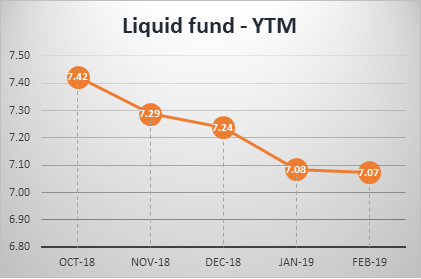

Portfolio yields drop

Yield-to-maturity (YTM) of portfolios measures the average yield if all the papers are held till their maturity. Average YTM of funds from the latest portfolio February 2018 stands at 7.07%, significantly lower than 7.53% in July 2018. From the graph, we can see that YTMs have been slipping gradually in the last 5 months.

Composition matters

Liquid funds invest in a mix of commercial papers, certificate of deposits, T-bills and other money market instruments. Funds mix and match combinations of CDs and CPs depending on where returns look optimal.

When the short-term yield spiked, commercial papers issued by corporates looked attractive. Funds had, in fact, strategically hiked exposure to CPs during this period. On an average, their exposure to CPs were around 65% in 2018, against 55% a year ago. Post the IL&FS crisis, however, this proportion came down. The latest portfolio average exposure to CP is 57% with the rest allocated to relatively less risky CDs and T-Bills.

In short, the high 2018 returns of liquid funds are turning lower as they adjust to changing markets. A recent regulation introduced by SEBI may also impact returns, even as it may lower the risk. Liquid funds will have to mark-to-market papers with residual maturity of more than 30 days. To guard against volatility that this move can induce, chances are that liquid funds reduce their average maturity which may further dent returns.

However, liquid funds remain an attractive alternative to savings bank accounts. As SBI decides to link its savings bank rate to repo rate, other major banks may follow suit. This means faster transmission of change in rates, leaving liquid funds the superior alternative for short term money. Debt funds with longer durations will also take time to reflect this trend as they continue to hold higher-yielding papers.