What happened?

In the last few days, global equity markets have fallen sharply on concerns of coronavirus, a respiratory illness first identified in Wuhan, China, and spreading globally.

The market decline came as the outbreak continued to spread outside of China; with Iran, South Korea and Italy reporting a surge in cases. At the current juncture, the total cases reported have crossed 81,000 globally and total deaths have been upwards of 2,750.

Investors globally are worried that this could lead to a prolonged economic slowdown across the world.

Looking at the Past…

Unfortunately, there are several uncertainties involved in the current situation – how quickly a vaccine can be created, where will the virus spread next, and most importantly, how quickly the virus can be contained.

The broad sense that we are getting at this juncture is it could still go ‘in any direction’.

This leaves us with a humble view:

That being said, we can, however, get a rough sense of how equity markets have behaved in the past during similar instances of epidemics.

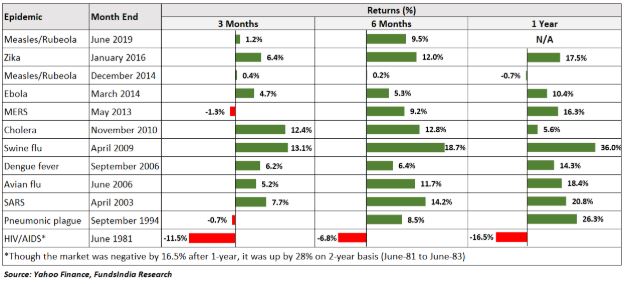

The below table shows how the US equity market (represented by S&P 500) had reacted to past epidemic outbreaks.

Obvious next question…

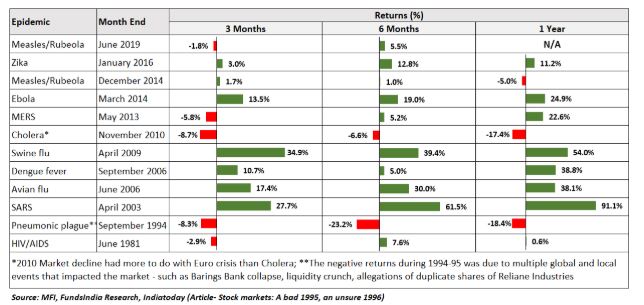

What happened in the Indian markets?

In the three months following an outbreak, the global markets and Indian equity markets have only seen small declines if any. Inevitably, equity markets have always recovered post that.

So the key takeaway for us is that,

How do we approach this situation?

For making a decision we have two perspectives to consider

- History indicates that epidemics of the past had very minimal short term impact

- The possibility of what if this time it’s different and more severe – leading to a sharp market decline

How do we come to terms with the view that – odds of a sharp fall are low and yet, we cannot completely rule out a sharp decline?

If you haven’t guessed still, it’s a roundabout way of being honest with you.

The answer is ‘We can’t precisely predict the future. Neither can anyone else’.

The paradox of accepting that things are not under our control is that suddenly we get better control over the situation. This is because now we start to ‘prepare’ for a ‘wider range of outcomes’ rather than trying to forecast a precise outcome and act based on it.

So how do we ‘prepare’?

There are possibly two paths the markets can take if the concerns on coronavirus persist:

Path 1 (with high odds): History Repeats… Markets have a small fall but recover quickly

Action to be taken:

- As long as your portfolio is well-diversified, aligned with your risk tolerance and in line with your long-term plan – NO ACTION is required

- You can continue to remain with your long term intended equity allocation

Path 2 with low odds but possible: This time it’s different – The coronavirus impact is significant and it impacts the global economy leading to a steep market decline.

Now before you think, this is going to be a straightforward path, there is a small twist to the plot…

Except for in retrospect, you won’t know if the market is on Path 1 or Path 2!

As with all previous market declines, it is impossible to know beforehand whether a 10% fall is a precursor to a prolonged steep fall or is just a normal temporary decline that is expected to recover immediately.

So, the overall idea is to humbly acknowledge this “I don’t know and I recognize that the world is a complicated place” stance and have a plan on when and what to act, if a crisis follows.

This will help us convert path 2 (a crisis), if at all it happens, into an opportunity!

A simple plan might look like (this can be customized based on your risk profile, time frame and plan):

- 10% fall – No action

- 20% fall – Move 20% from debt portion (intended for tactical allocation) to equities

- 30% fall – Move next 30% from debt portion (intended for tactical allocation) to equities

- 40% fall – Move next 40% from debt portion (intended for tactical allocation) to equities

- 50% fall – Move next 10% from debt portion (intended for tactical allocation) to equities

*If in case of extreme valuations for the market, this plan might need some adjustments. But at the current juncture, the valuations are close to long term averages for most measures such as MCAP to GDP, PB ratio (except for PE ratio where it is on the higher side) and hence our plan holds good.

This will ensure that you are better prepared to take advantage of the market without the need to predict the precise impact of how coronavirus plays out.

The lure of “I knew it all along. If only I had..”

The most likely failure point during market volatility periods usually happens at the period between 10-20% decline.

Why?

Because this is the juncture, where you are confused whether it is path 1 or path 2!

When the fall prolongs, there is a natural instinct to sell now and enter later which is nagging you at the back of your mind. While you might resist the temptation to act (assuming you are sold on the you-can’t-predict-but-only-prepare-philosophy), if the market continues to fall further then suddenly ‘regret’ kicks in.

Though there is overwhelming evidence that no one can predict, you feel that actually, YOU DID PREDICT THE FALL!

“If only I had listened to my own intuition and sold out” your inner voice is mad at you.

Any further fall and you are convinced – to hell with this “can’t predict” crap.

And you utter the most dangerous words, “Let me move out and enter later”.

And going by the experience of several million investors across the world, more often than not the story doesn’t end well…

The biggest issue in getting out is to again get back into equity markets. Even if you are right the first time, to get back in, you need to be right twice. And while we imagine the equity market trajectory to be a simple straight line, there are too many false upsides during a fall. This lulls you into complacency (read as “I have seen these temporary upsides before. It will fall again. I will wait”), and when the actual recovery happens, you think it’s yet another false start and by the time you realise this one is the real one, it is usually too late.

It is important to be aware of this failure zone as much of the success in sticking to your plan will be dependent on how you behave in this period.

Parting thoughts…

While it is impossible to predict the future impact of coronavirus, history indicates that usually the global economy and equity markets have been relatively immune to the effects of past epidemics.

However, if this one turns out to be different and has a significant negative impact, we are ready with our ‘what-if-things-go-wrong’ plan.

The idea is to be humble and accept that the world is an uncertain place. It will always be.

-Dan Kahneman, Psychologist and Nobel laureate

Equity markets, in the long run, are a proxy for human ingenuity and innovation. As long as you believe in this core premise – the simple answer remains ‘This too shall pass!’

From our side, as always, while we won’t be able to predict, we will continue to ‘Prepare’ our investors, come what may!

Happy investing as always 🙂

Excellent article for time and encouraging. Many Thanks Arun

Thanks Deepak for the kind words