Not so great recent performance…

Intuitively most of us like to buy a fund with a strong recent performance or high star rating (which is significantly influenced by strong recent performance).

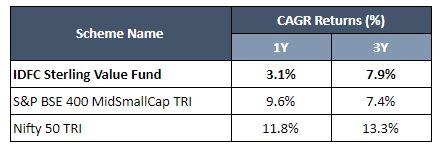

Let us check what IDFC Sterling Value Fund’s recent performance looks like…

Oops! Nothing to write home about.

So our natural response is to conclude: ‘Weak performance means not-so-good fund. Hence let me ignore this fund’

But what if we told you that, this is an interesting offering that you must consider!

This is exactly where we want you to take a pause and evaluate this fund with an open mind.

The lure of past performance…

While the ultimate endeavour is to outperform benchmark market indices over the long term, there are different approaches fund managers/funds adopt to achieve this.

Some funds are large-cap oriented, some are mid-cap focussed, some are small cap oriented, and some are a combination of the above and so on. Some follow the growth strategy, some are momentum-driven, while some are value-oriented and some are a mix of these.

As investors, you must realize that different approaches to generating long-term returns also imply different trajectories of returns. Each approach will lead funds to periods where they do well and occasional periods where they underperform.

Any approach to long-term outperformance is guaranteed to have occasional short-term underperformance.

If you only go for funds with strong recent performance, there is a high likelihood of ending up with a portfolio of funds having a similar investment approach. This means all the funds in your portfolio will rise and fall together at the same time, thereby not providing any diversification benefit.

This approach becomes particularly dangerous during bubble phases as the highest returns are earned only by products that take high levels of risk – either in terms of sectoral concentration or high valuations or dilution in balance sheet quality.

Diversified portfolio construction approach to the rescue…

In our view, an equity portfolio should be constructed using a few good funds that follow different investment approaches.

This reduces the overall volatility of the portfolio without compromising on long-term outperformance.

As long as the respective fund managers are sticking to their stated mandates, investment approach and are managing risk in a logical manner, this approach should help us achieve a successful investment outcome in the long run.

So this leads us to the next logical question:

Which investment approach has a proven long-term outperformance record but is currently out of favour (read as going through the occasional but expected underperformance)?

Over the last few years, these are the investment approaches that have been going through tough times

- Midcaps

- Smallcaps

- Value

What would be your return expectations for the last few years from a fund exposed to all the above three strategies?

This is where things get interesting.

IDFC Sterling Value Fund is exposed to all three!

No wonder the fund has underperformed in recent times.

We also know from history that these three investment styles mid, small and value have delivered outperformance over long periods not just in Indian markets but also in global markets.

While it is difficult to exactly time when there will be a reversal of performance towards these three styles, from a 3-5 year forward-looking perspective, going by history the odds are tilted in our favour.

If you buy this logic, then you should definitely consider some exposure to these three currently underperforming styles in your equity portfolio allocation.

This is where we find IDFC Sterling Value Fund as an interesting opportunity.

IDFC Sterling Value Fund – An underrated fund at the helm of a reputed fund manager…

-

Backed by a veteran fund manager with a 17-year proven record in mid and small cap space

- The fund is managed by Anoop Bhaskar and Daylynn Gerard Pinto

- Anoop Bhaskar, a market veteran with 29 years of market experience is the Head – Equity, IDFC Mutual Fund and has been managing the fund since Apr-2016

- Daylynn Pinto has been managing the fund since Oct 2016 and has 14 years of mutual fund industry experience

What’s the big deal?

- Anoop Bhaskar has only been managing the IDFC Sterling Value Fund for less than 4 years.

- But he has a solid and probably the longest track record for any Indian fund manager in small and midcap funds across 3 fund houses (around 17+ years as a fund manager)

- Under his helm:

- UTI Midcap Fund generated a return of 16.2% (CAGR) vs the benchmark’s 12.8% during his tenure (Apr 07 – Jan 16)

- Sundaram Midcap Fund generated a return of 54% (CAGR) vs the benchmark’s 32% during his tenure (Apr 04 – Mar 07)

-

Uniquely Positioned to capture recovery in Value, Small and Mid Caps

- Well-positioned to benefit from a mid and small cap recovery driven primarily by a revival in domestic cyclicals such as infra, construction, cement, metals once the broader economy picks up

- Small (37%) and mid cap stocks (46%) accounted for 83% of the fund’s portfolio as on 31-Jan-20.

- Cyclicals accounted for 60% of the fund’s portfolio as on 31-Jan-20

-

Strong pick up in earnings growth but still at reasonable valuations

- Strong Earnings Growth: Earnings growth for the fund portfolio companies in the last 1 year has been 43% vs 14% for the benchmark companies

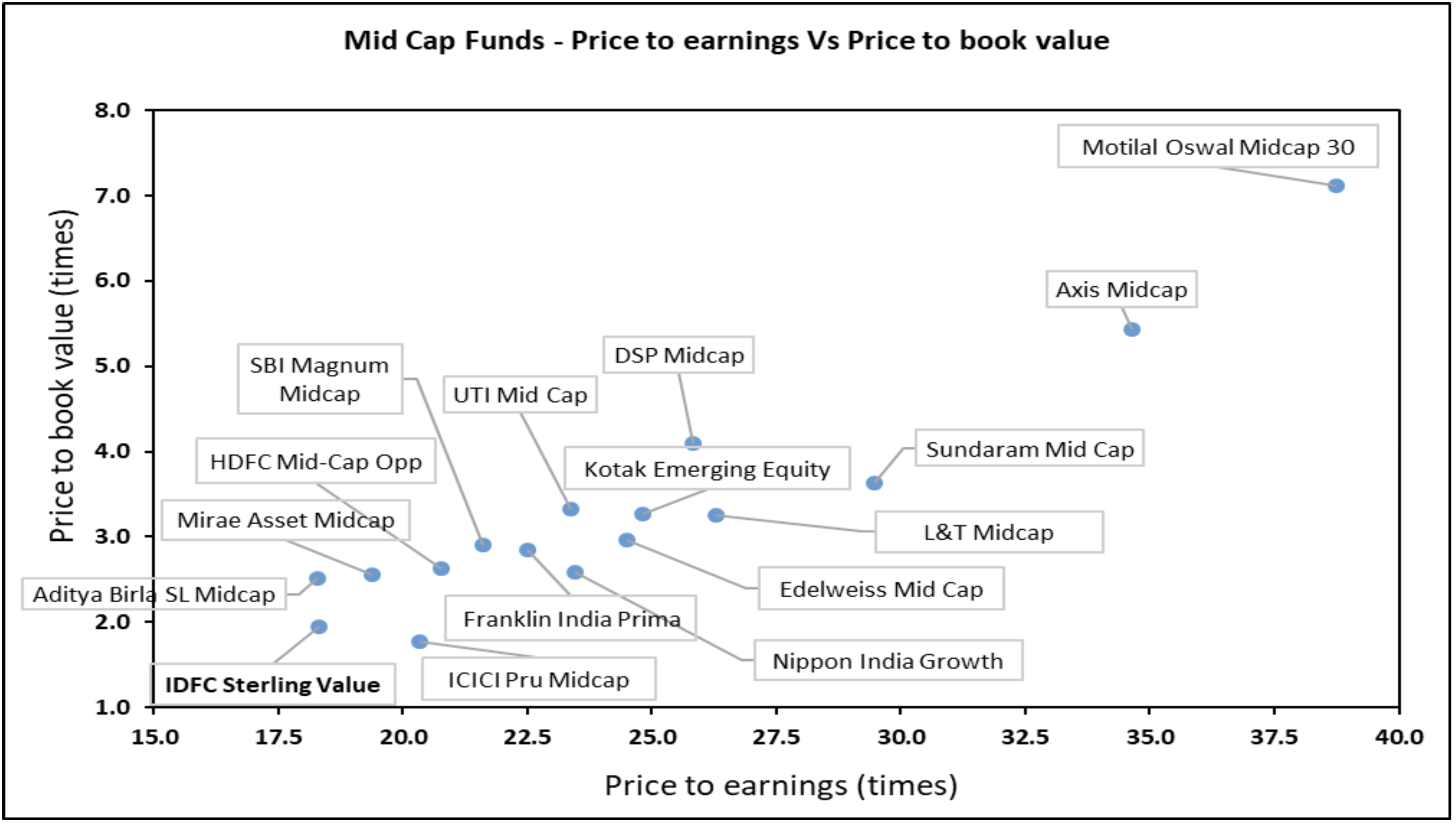

- Attractive valuations: The fund follows the ‘value’ style and its current Price to Earnings ratio (19.2 x as against 26.5 x for the benchmark) and Price to Book ratio (2.0 x as against 2.4 for the benchmark) are lower than those of the benchmark index

- What is also worth noting is that IDFC Sterling Value is the most attractive fund across the midcap fund space from a valuation perspective. Its PE and PB ratios are among the lowest in the midcap fund category. See the chart (bottom left)

-

Reasonably sized AUM provides the required flexibility for navigating mid and small cap space

- The fund’s reasonably sized AUM of Rs. 3,220 crore as on 31-Jan-20 gives it better flexibility in portfolio construction compared to say some of the ’large’ small and mid cap funds

-

Fund managers continue to stick to their stated mandates and investment approach

- The fund has not diluted its investment style and strategy despite the testing times which is a key positive

-

Who should invest?

- Risk Appetite: High risk appetite

- Holding Duration: Minimum 5-7 years

- Strategy: Invest in lumpsum and follow up with 6-12 month STPs

-

What can go wrong?

- The expected mean reversion takes longer than 3-5 years to happen and the current market preference for ‘Quality and Large Caps’ continues for an extended period.

Summing it up..

Given the fund manager’s short time span at IDFC Sterling Value Fund and the underperformance of value, small and mid cap approach in recent times, the fund usually does not come in the radar of most investors.

However, in line with our portfolio construction logic of having a mix of products with proven but different long-term investment approaches, we urge investors (though it is emotionally painful) to consciously have some degree of exposure to investment approaches going through temporary underperformance.

Going by history, we believe the future return potential is significant from these pockets when there is a mean reversal of performance in these ‘currently out of favour’ approaches

The current underperformance (while it is obviously annoying), occurring in an environment where the strategy is expectedly struggling is actually good evidence of the fund managers staying true to their process and mandate.

We like the fund for the following factors:

- Fund manager with a proven track record

- Well-positioned portfolio – to capture recovery in value, mid caps and small caps

- Reasonable AUM size

- Sticking to the investment approach even during tough times

The discipline from the investment manager to stick to his investment process while has been demonstrated, the key for us as investors is to stick with the manager and the approach, to participate in the future return potential.

As always, Happy Investing 🙂