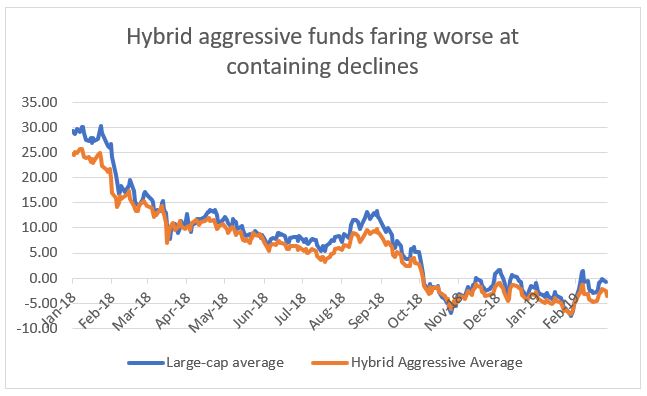

On a 1-year basis, hybrid aggressive funds are in the low single digits at just 1.2% on an average. Not just that, the category was clocking 1-year losses in preceding months. That’s not new – hybrid aggressive funds can well deliver losses on a 1-year timeframe. What’s surprising this time around is that this average is lower than the Nifty 100 TRI as well as the average for large-cap equity funds. This fund category is meant to contain equity losses. You may have also noticed flagging returns in hybrid aggressive funds that you hold in your portfolio. So, what gives?

It has to do with an unusual combination of a sell-off in the midcap and smallcap space while largecaps remained steadier and the volatility in bond yields. Here’s what happened.

Pulled down by broader market

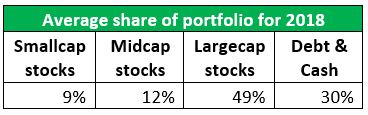

Hybrid aggressive funds put 65-75% of their portfolio in equity and the remaining in debt. In both allocations, funds juggle around to maximise returns. On the equity side, these funds picked up smallcap and midcap stocks over the years.

This allocation helped these funds post strong returns that matched up with or even beat large-cap funds during the earlier market rally.  This mid-and-smallcap share, though, pulled down returns over 2018. And while this segment was correcting, large-cap stocks were far steadier.

This mid-and-smallcap share, though, pulled down returns over 2018. And while this segment was correcting, large-cap stocks were far steadier.

The Nifty Midcap 100 and the Nifty Smallcap indices corrected 7.2% and 20.5% on a 1-year basis. The Nifty 100 on the other hand is up 7.6%. And remember, falls in the mid-cap and small-cap indices have been even steeper in earlier months. It is only in the past couple of weeks that the two indices clocked gains that is pulling up the 1-year return picture.

On an average, funds held about 20% of their portfolio in mid-and-smallcap stocks over 2018. This share may not seem high. But with the extent of midcap and smallcaps correction, even a smaller allocation can hurt. For example, take a simple blend of the Nifty 100, Nifty Midcap 100, Nifty Smallcap 100 and the Crisil Composite Bond index in the average proportion of hybrid aggressive funds. Even this combination resulted in 1-year losses and a steady lag of the Nifty 100 TRI.

Individual funds ranged much more across the marketcap curve. Some funds had a 55-61% large-cap allocation. This includes funds such as Mirae Asset Hybrid – Equity, ICICI Prudential Equity & Debt, Canara Robeco Equity Hybrid, and Franklin India Equity Hybrid. Others such as Aditya Birla Sun Life Equity Hybrid ’95, DSP Equity & Bond, Kotak Equity Hybrid, and UTI Hybrid Equity had a higher share of mid-and-smallcaps.

Individual funds ranged much more across the marketcap curve. Some funds had a 55-61% large-cap allocation. This includes funds such as Mirae Asset Hybrid – Equity, ICICI Prudential Equity & Debt, Canara Robeco Equity Hybrid, and Franklin India Equity Hybrid. Others such as Aditya Birla Sun Life Equity Hybrid ’95, DSP Equity & Bond, Kotak Equity Hybrid, and UTI Hybrid Equity had a higher share of mid-and-smallcaps.

Second, stock choices came into play. While large-cap stocks fared relatively better, the large-cap index itself has been held up by rallies in only a handful of stocks. Outside these, most stocks saw price falls. The indices, therefore, become a skewed benchmark as far as measuring performance goes. So though funds stayed cautious on the marketcap front, they still took a hit compared to the Nifty 50 or the Nifty 100 returns. For example, Reliance Equity Hybrid underperformed despite a high large-cap allocation as stocks it held saw price corrections.

Third, some funds also got more aggressive on the equity front as the correction threw up buying opportunities. Adding to equities at a time when stocks were falling exacerbated the impact.

Debt volatility hurts

If stock corrections were a sore point, volatility in bond yields added to the trouble. For most of 2018, expectations were that the rate cycle would trend upwards. Bond yields also spiked with the liquidity crisis. Though expectations revered towards the end of the year, bond yield volatility hurt debt returns for funds too. Yield movements affect AAA and government bonds more than others.

And this is where hybrid aggressive funds typically hold most of their debt. They held 5-8% of their portfolio in government bonds and 10-15% in corporate debt on an average for most of 2018. They didn’t hold much of commercial paper or bank CDs. Therefore, hybrid aggressive funds were hit on the debt side as well.

This combination of equity falls and debt volatility is not common. It’s not that only funds have faltered. For most of 2018, the Crisil Hybrid 35+65 Aggressive index (which blends the BSE 200 and the Crisil Composite Bond index) itself lagged the Nifty 100 TRI. Hybrid aggressive funds need a 3-year minimum holding period and have often delivered losses on a 1-year basis during market corrections. On the debt side, while yield movements do affect prices, the fund would still earn the coupon on those bonds and eventually reverse the price movement.

This article first appeared in Moneycontrol.com. It has been republished on this blog.