At a time when most of us are worried about our health and safety, the equity markets are not making it any easier for us.

All of us are worried about the same question…

What will happen to the equity markets next?

Instead of us boring you with jargons such as valuations, earnings growth blah blah, what if we take the help of our neighbourhood maths teacher to find out the answer.

But, before our maths teacher reveals the answer, she has a few questions for you.

1. Do you think equity markets will recover in the future?

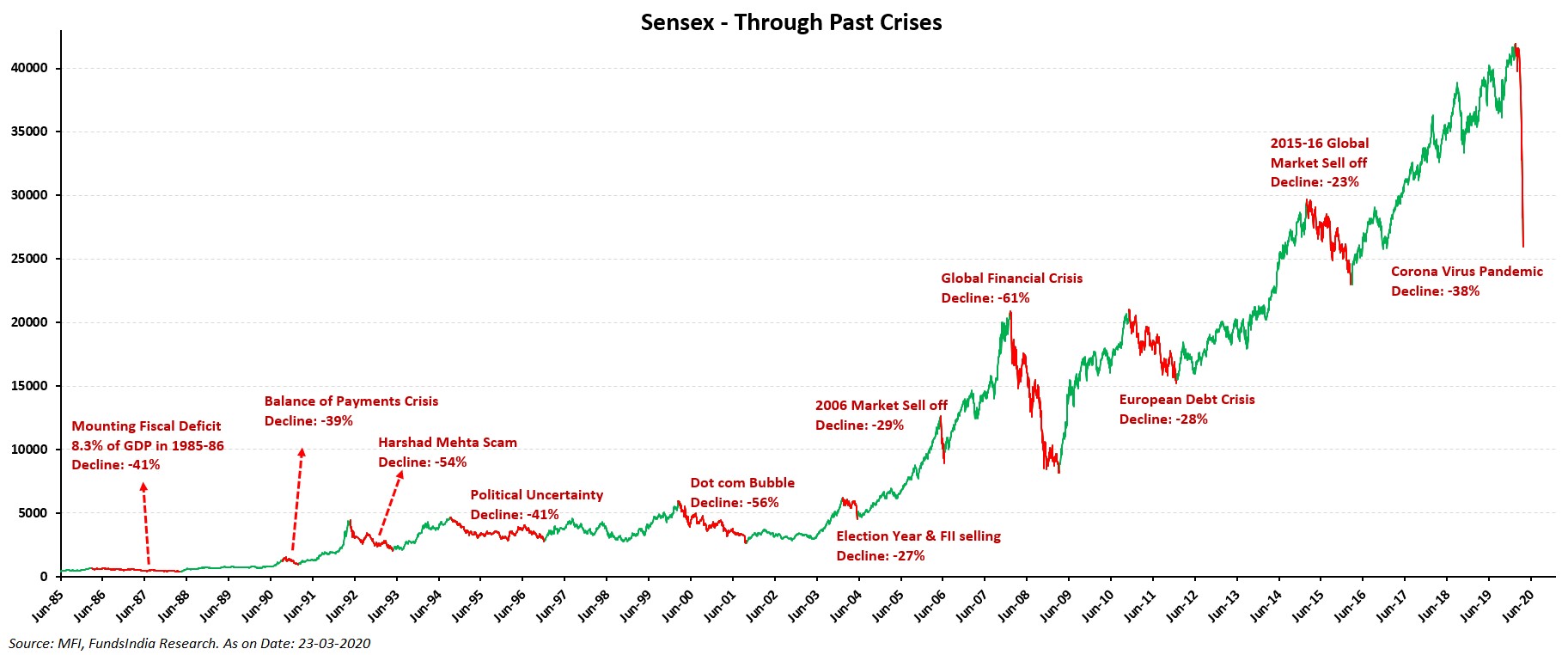

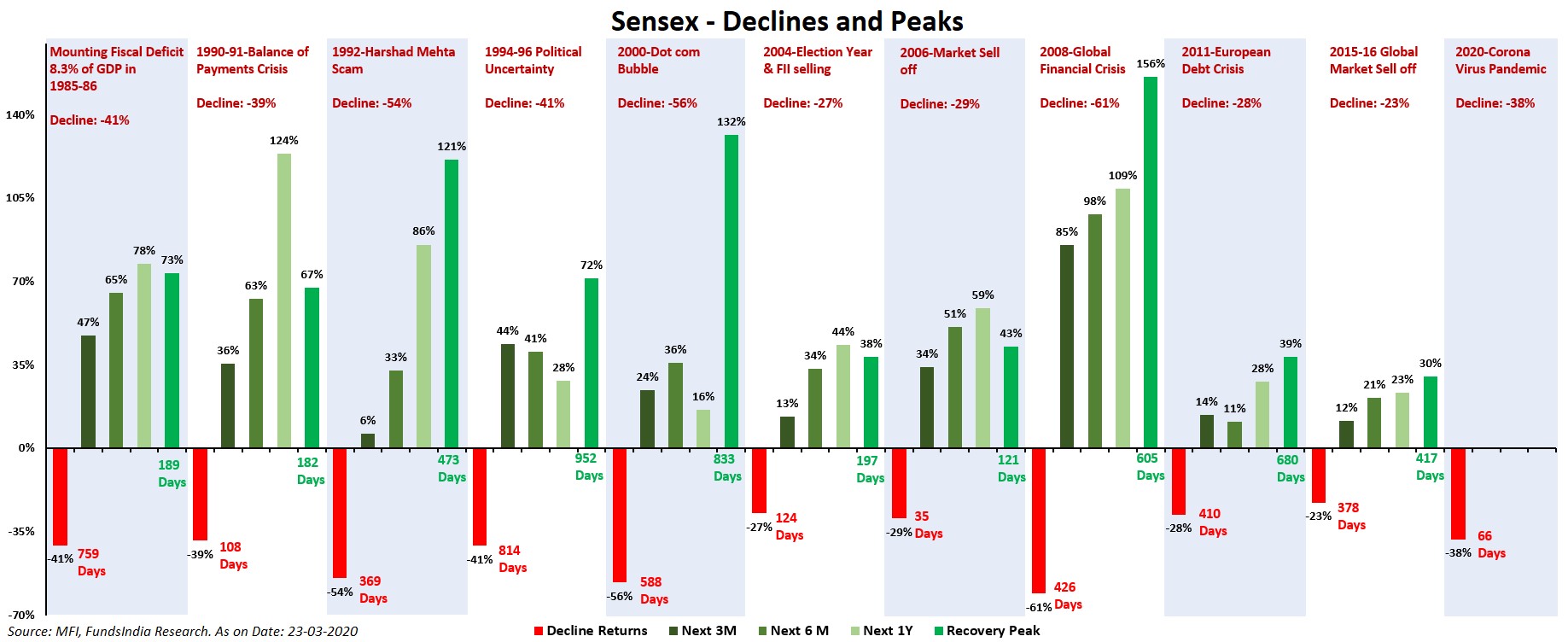

In the last 40 years since 1980, there have been 6 instances where markets have fallen more than 40% and only 3 instances where the fall was more than 50%.

Now if you are wondering what happened post these market crashes..

Inevitably, the markets always recovered.

Now that we have helped you with the clues, what is your answer? Do you think equity markets will recover in the future from their current levels?

2. How long does it normally take for recovery?

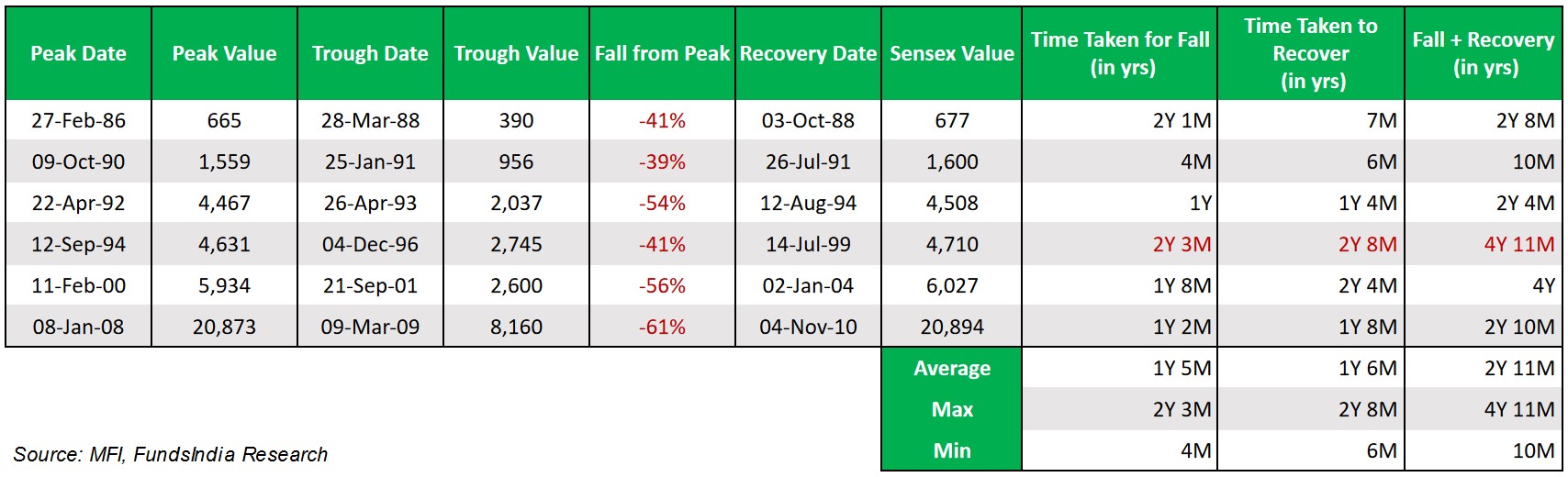

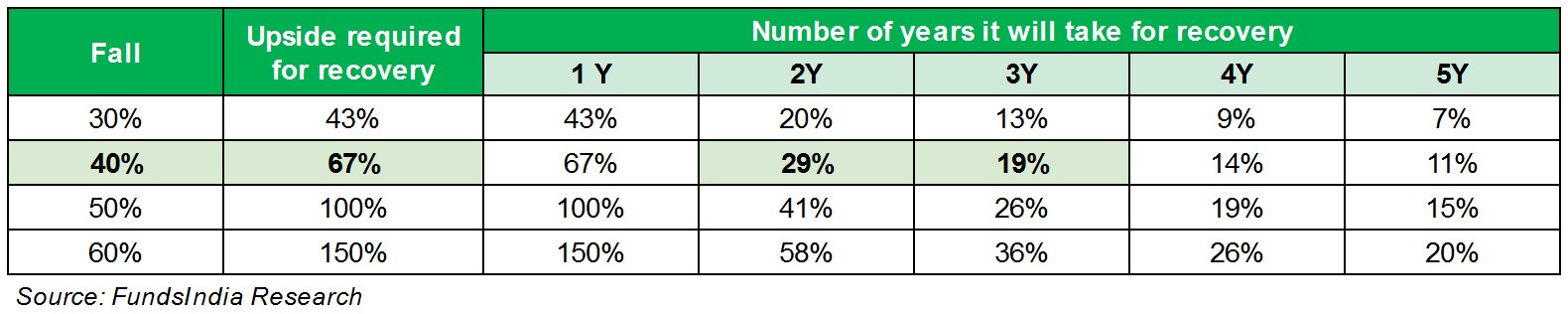

Historically, when the markets have corrected more than 40%, the average time for which the decline lasted has been 17 months. The longest period of decline has been around 2 years and 3 months.

In the past, from the point of 40% decline, the markets on an average have taken 2 years to recover to the previous peak level. While the shortest period of such recovery has been 6 months, the longest period has been 3 years and 3 months.

Now it’s time to refresh your high school math.

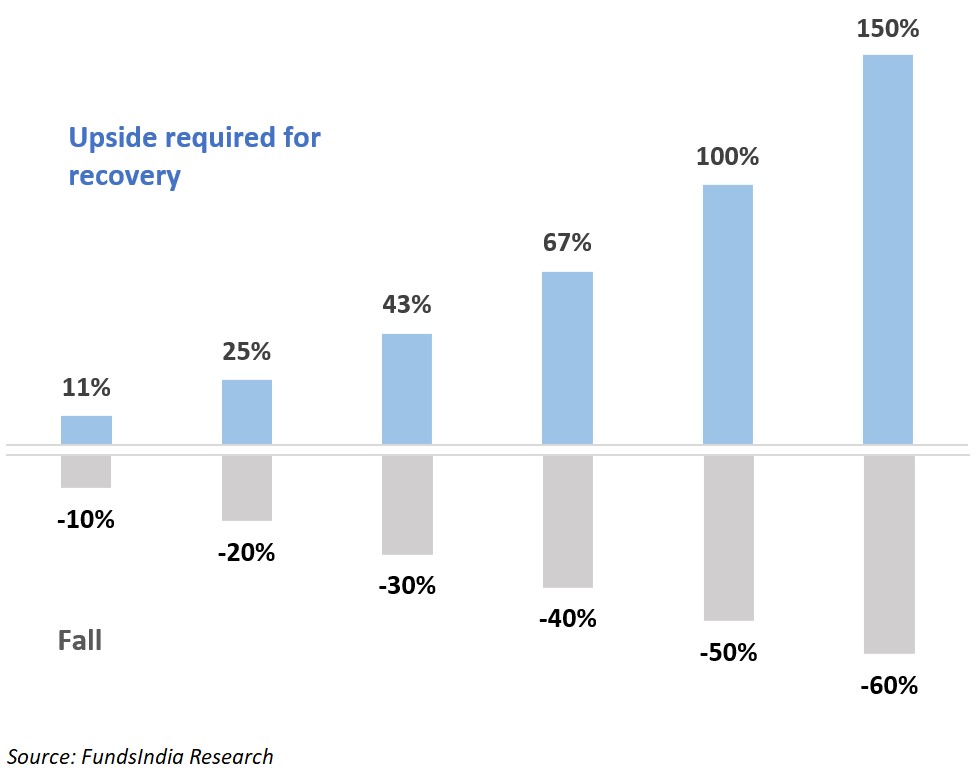

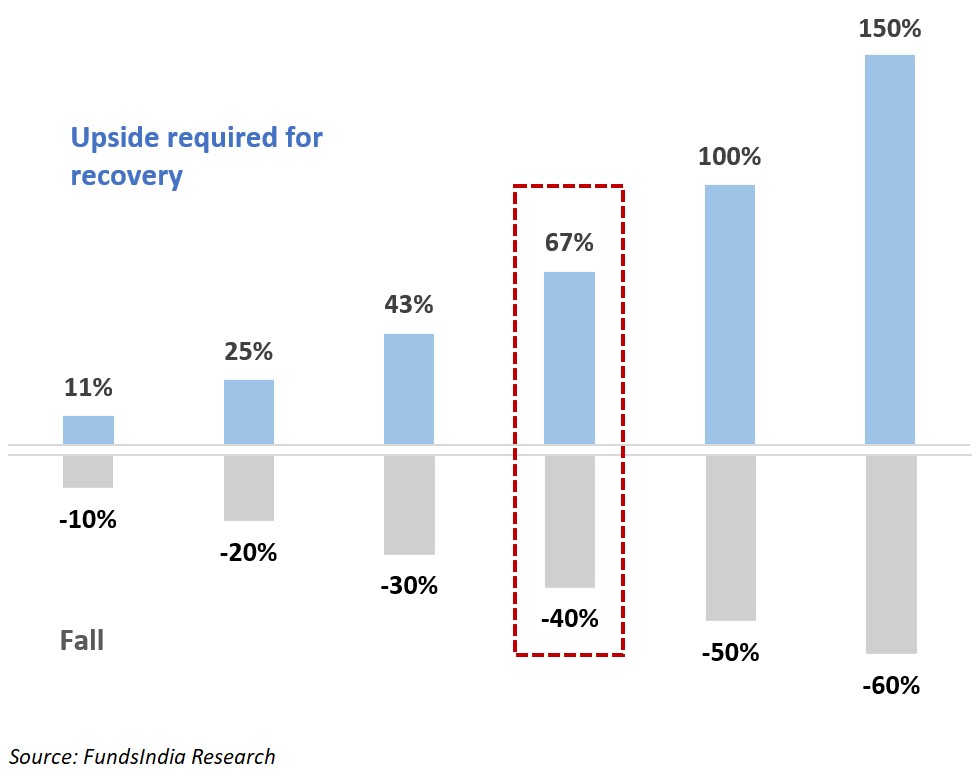

3. For a 40% fall, how much upside is required to recover the entire decline?

Got the answer? Did you notice something?

67% is the upside required to recover a 40% decline and it is dis-proportionally higher!

This reminds us of the simple math rule:

Every percentage loss requires an even larger percentage gain to recover the loss.

4. Where are we now?

Close to 40% decline from the highs. This means mathematically it requires 67% upside to recover back in the future.

We earlier agreed that markets have always recovered and this time won’t be an exception.

Let us plug in the average and longest time period of recovery – 2 years and 3 years and find out the annualized return expectation.

Going purely by the math, we are looking at whopping CAGR returns of 19% to 29% from equities.

To put that in context – Debt returns at current yields are positioned at 6-7%.

If you agree that this recovery won’t take too long (more than 3 years), then you can work with the above assumptions or you can modify them as per your views.

5. What does our maths teacher recommend?

Now if you have a 5 year plus time frame and the ability to tolerate further downside, then our maths teacher has her recommendation ready for you.

Increase Equity Allocation – The math is in your favour!

But wait. You still have another question…

6. What if it falls further?

Unfortunately, our maths teacher feels, this is a question for which she doesn’t have an answer. But again with some quick maths, here is what she has to share:

- % of times Sensex has traded below 40% decline from the peak: 9% (844 out of 9428 trading days since 1980)

- % of times Sensex has traded below 50% decline from the peak: 2% (200 out of 9428 trading days since 1980)

- % of times Sensex has traded below 60% decline from the peak: 0.04% (4 out of 9428 trading days since 1980)

With markets (Sensex) having spent only 4 days in the last 40 years below 60% decline, this is too rare an event.

To minimize regret – split your current investments into two equal tranches and invest at 40% and 50% decline.

Summing it up..

Now, these are times, where our emotions are screaming “Sell and get done with this pain”.

History has proven that we would be better off if we listen to our maths teacher instead.

It’s still not too late…

Stay safe and don’t forget the math!

P.S: At the current juncture Valuations are also very attractive via MCAP to GDP at 50% and Price to Book Multiple of Nifty at 1.9 times similar to the 2008 lows. Price to Earnings Multiple is trading at 14.7 – far below long term averages around 18 times.