The last few weeks have been pretty tough for most of us.

At the current juncture, while ‘Be Patient’ remains the best time-tested advice, let us be honest. This is far easier said than done.

Given the sharp declines in the equity market, there is a high likelihood of hasty decisions in panic, which can have long-term repercussions on our future goals and portfolio returns.

During times like these, while no one knows when it will end, there is a simple takeaway from studying past market corrections –

Inevitably equity markets have always recovered!

Napoleon Bonaparte had a great definition of a military genius –

The person who can do the average thing when everyone else around him is losing his mind.

This is exactly what is required from us at the current juncture.

If we can think through this and approach the correction with a logical plan, then the current decline can actually be a great opportunity to improve our overall long-term portfolio returns.

How do we do this?

Let me attempt to address this via answering several questions currently running in your mind…

Will markets continue to fall in the coming days, weeks, months? To what extent will they fall and when will they finally recover?

To predict the outcome we will need to know the answers to…

- How quickly a vaccine can be created for Coronavirus, where will the virus spread next, and most importantly, how quickly can the virus be contained?

- What will be the economic impact on different global economies and India?

- Where will oil prices settle and how will the current lower oil price impact the global economy and India?

- What will be the government and central bank action to stimulate the economy both globally and in India?

And assuming we luckily get all the above right, here is the final part we need to predict…

How will millions of investors with different goals, perspectives, risk appetite and time horizons react to all the above?

Given the fact that no one predicted Coronavirus two months back, we would reiterate our humble view – No One Knows.

There is no way to predict markets in the short term. There are simply too many moving parts and to predict each and every one of them consistently is next to impossible.

So if we don’t know what the markets will do over the short term, how do we act?

In times of extreme noise, we prefer taking the ‘first principles’ approach and going back to the fundamentals.

There are three things which drive market returns over time.

- Earnings Growth

- Dividend Yield

- Change in Valuation multiples – reflecting how much investors are willing to pay for those earnings

Equity Returns = Earnings growth + Dividend yield + Change in Valuation Multiples

Simply put, to predict future equity returns, we need to predict the above 3 things.

Let us get done with the easiest one. Historically, Dividend Yields have been around 1.5% for the Indian large cap index Nifty 50. This can be a fair assumption to make going forward.

Earnings growth for a diversified portfolio is reasonably predictable over longer time horizons. Long-term 10Y earnings growth in India has averaged around 10-12% CAGR. The last 5 years were at sub 4% and assuming that it gets back to long term averages, we can expect an above-average period of earnings growth for the next 5 years.

When it comes to short-term returns, the third factor ‘Changes in Valuations’ is where the problem lies.

Short-term returns are significantly driven by changes in valuations (read as “change in investor sentiments”). And as you would have guessed by now, predicting the future sentiments of millions of investors is a futile exercise.

Morgan Housel of Collaborative Fund, had this to say on the subject of valuation:

“Earnings multiples reflect people’s feelings about the future. And there’s just no way to know what people are going to think about the future in the future. How could you?

If someone said, “I think most people will be in a 10% better mood in the year 2023,” we’d call them delusional. When someone does the same thing by projecting 10-year market returns, we call them analysts.

However, the good part is, the impact of change in valuations (provided you haven’t entered at extremes) on equity returns, diminishes over the long run.

So while we can’t predict the markets over the short run because of the unpredictable nature of valuation changes, over long periods, markets are driven by earnings growth (and dividend yields) which are reasonably predictable.

This means, for a long term patient investor

- Earnings growth remains the key driver of returns – this is reasonably predictable for a diversified equity portfolio over the long run

- Entering at insanely expensive valuations can reduce returns below long-term earnings growth (as valuations revert back to their long-term averages)

- Entering at average valuations can produce returns mirroring long-term earnings growth

- Entering at cheap valuations can produce excess returns over and above long-term earnings growth (as valuations revert back to their long-term averages)

What do the earnings growth expectation and valuations indicate about long-term return expectation at this juncture?

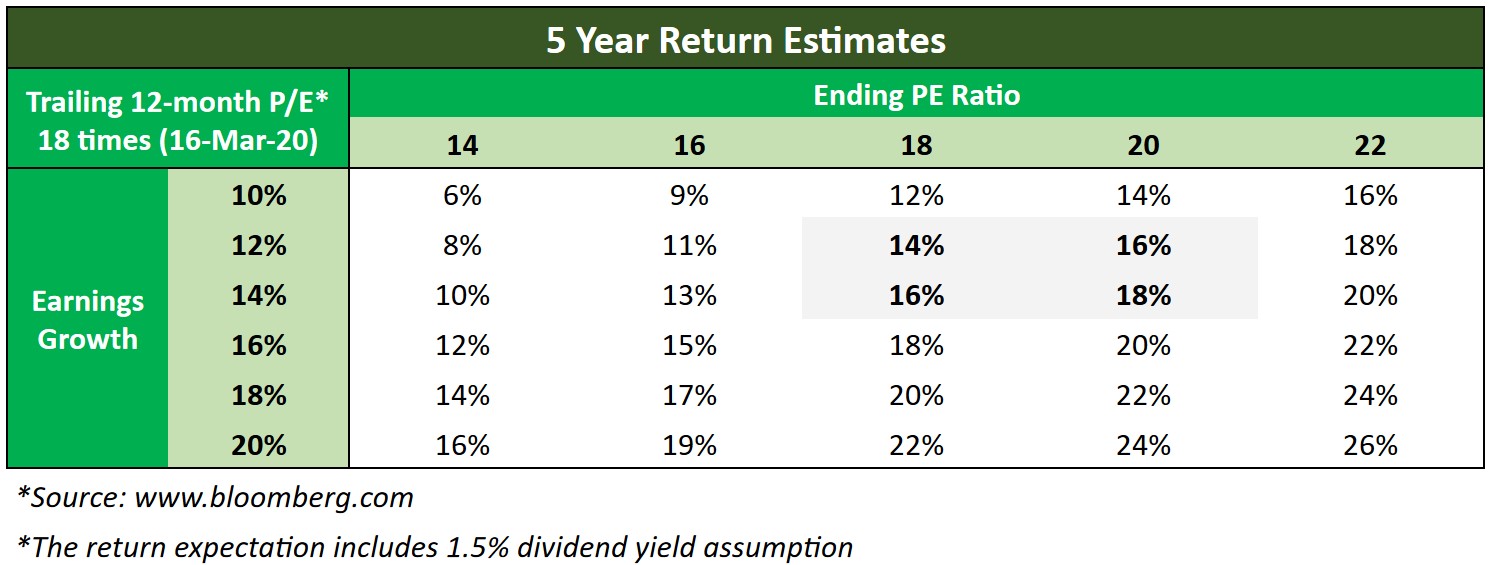

Valuations: The trailing 12 month PE multiple for the Nifty 50 has corrected from 23 times to 18 times in the last few weeks. The long term averages have been around these levels and we can assume 18-20 times as a sensible range for building our future expectations.

Earnings Growth: We were earlier building an estimate of around 14-16% earnings growth for the next 5 years factoring in the low base, recovery in profitability of corporate banks and the recent corporate tax cuts.

While it is still too early to quantify the impact of Coronavirus on 5-year earnings growth, assuming a lower earnings growth expectation of 12-14% (to be honest, no one knows the sanctity of this assumption at this juncture, however we believe it is a reasonable long term assumption to make based on historical trends), we are still positioned for a 14-18% return environment assuming the PE multiple stays close to historical averages of 18-20 times.

This implies the return environment has become very attractive and it makes sense to increase equity exposure at this juncture. Further correction will only imply equities get more attractive with higher return potential.

But what if markets decline further?

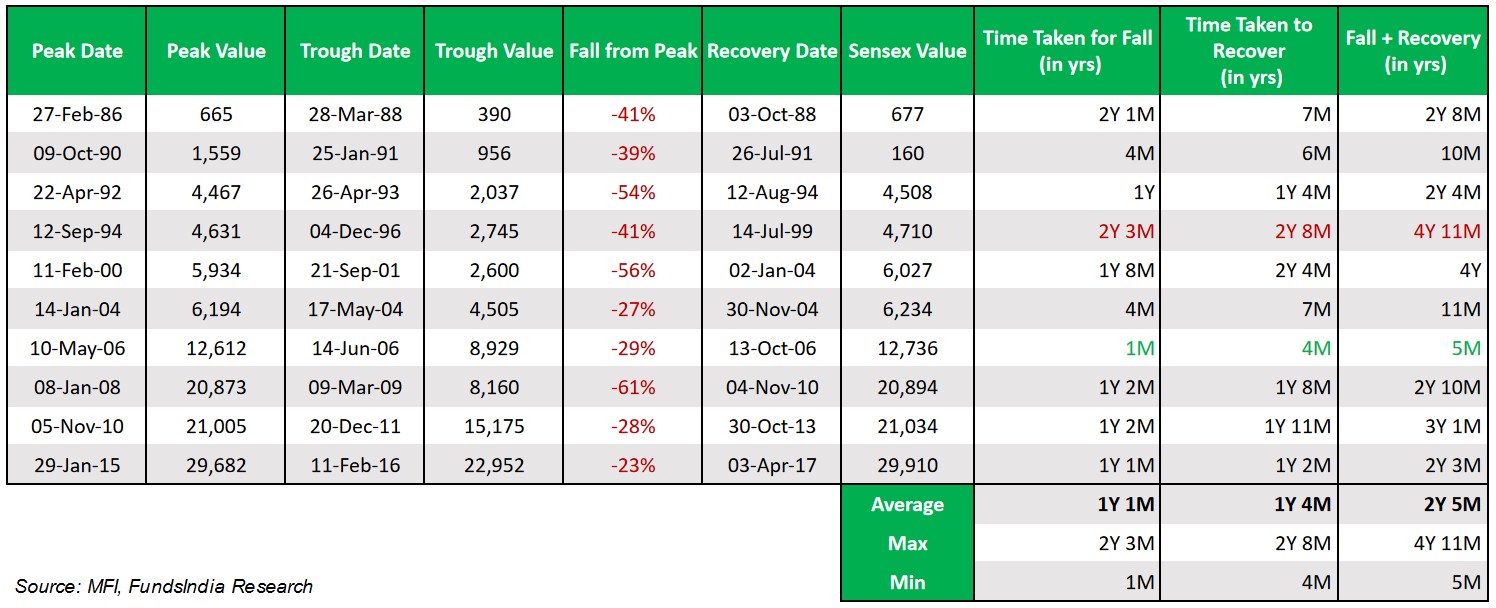

While we won’t be able to know that in advance, we can take a look at all the past declines (above 20%) and set reasonable expectations.

The average time for which a decline lasts is 13 months. The longest period of decline has been around 2 years and 3 months.

The longest period for a decline and recovery is around 5 years.

Given this, we would recommend investors wanting to make use of this opportunity in equities to at least have a 5-7 year time frame (accounting for the worst case).

Once the time frame is set, we will have to prepare for a wider range of outcomes rather than predicting a specific outcome and positioning for it.

What can be the different scenarios that can play out?

Broadly we can bucket this into three scenarios –

Optimistic Scenario: Coronavirus problem gets solved and everything is back to normal. The market recovers.

The Middle Path: Things are impacted significantly for a short period and the market falls further. Then things go back to normal. The market eventually recovers.

Doomsday Scenario: The virus spreads across the world taking a severe toll on human lives and businesses. The market crashes big time.

In the Doomsday Scenario, with our lives at stake, portfolio returns will be the last of our concerns. As an optimist and someone who believes in human resilience, this is something which in my personal view is least likely to happen.

So taking a pragmatic approach, we will put in place a ‘plan’ taking into account both the Optimistic Scenario and the Middle Path scenario.

What’s the plan?

The idea is to balance between – the regret of missing out if markets rally from here (optimistic scenario) vs regret of entering too early if markets correct further (middle path scenario).

Before you think it’s a very complex plan, this is how a rough plan looks like –

Decide the amount (from debt or extra money) that you want to deploy to make use of this opportunity in equities

- If market levels are at 20% decline from peak then move x% into equities

- If market levels are at 30% decline from peak then move x% into equities

- If market levels are at 40% decline from peak then move x% into equities

- If market levels are at 50% decline from peak then move x% into equities

You can customize the levels and actions (moving of x%) based on your preferences. The key is not to get bogged down by ‘precision’ but to have an approximate decent plan that you can stick to.

Since the valuations have corrected and have become reasonable, should I go ‘all in’ and invest everything in one shot?

Since no one knows where the bottom is, all we know is that currently the valuations are attractive and with every further fall they become even cheaper.

We know that from today’s levels our odds of a good return over the next 3-5 years are significantly high.

But if we deploy the entire amount (earmarked from new money or debt portion to make use of this opportunity), what happens if markets fall further. We are then left with the regret of having bought too early.

Then should I wait for a further fall?

If we don’t invest and wait for a further fall, then if the markets suddenly rally, we are left with the regret of not buying at lower levels.

So the idea is to balance out both concerns and instead take a gradual approach and incrementally deploy as markets fall. In this way, if the markets suddenly rally, at least we have some portion deployed, and if markets fall further we still have the cash to deploy.

Overall, from these levels, since the odds of good returns are in our favour, the idea is to manage our ‘regret’ rather than trying to predict a precise outcome.

Where should I invest?

We would recommend sticking to well-diversified multicap funds helmed by experienced fund managers which provide 20-30% exposure to mid/small caps. You can refer to our FundsIndia Select List for suggestions.

What about my existing equity portfolio?

Before the decline happened, our internal model was building an equity return expectation of around 10-12% for the next 5 years (which is a real return of around 5-7% assuming an inflation at 4-5%). This was based on our assumptions of earnings growth of 14-16% CAGR + Valuation de-rating of around -6% CAGR + dividend yield of 1.5%.

Hence we were neutral (read as neither overweight nor underweight) in terms of our positioning. The asset allocation was in line with your risk appetite.

Given the sharp correction in valuations, the model is now indicating returns in excess of 14% over the next 5 years (under the assumption that there is no significant long term impact on the expected earnings growth recovery). We, therefore, believe this is a good time to increase your equity exposure (either from debt portion or new money).

Assuming markets correct further and recover later, should I exit my existing portfolio now and enter later?

Though this approach seems logical, the assumption it makes is market falls are gradual and unidirectional till the cycle turns. Unfortunately, the reality is a lot different.

- There are several false upside rallies during a decline and several false downsides during a recovery – making it extremely confusing and psychologically challenging

- The best and the worst days tend to occur close to each other – exacerbating the above issue

- Recoveries are extremely fast – usually first 1 to 3 months capture most of the recovery gains – the cost of mistiming is substantial

To add to the challenge, in times of crises, the government and central bank usually respond by announcing several stimulus measures and try to talk up the market. Since markets move based on future expectations, some of these announcements might result in a sudden change of sentiment leading to a sharp rally.

Also, since the decline has already happened, there is always the risk that we might end up converting the notional losses into actual losses if we are unable to re-enter at lower levels. For a detailed explanation, you can read our earlier article here.

Summing it up

Our thought process for approaching today’s markets

- In the short run, predicting markets is too difficult – given the various moving parts

- Our intent is to focus on things under our control

- The valuations have become attractive – higher odds of significant returns over the next 3-5 years

- Additional Investments made into equities (from fresh money or debt portion) at current levels can significantly improve overall portfolio returns

- Follow a rule-based, disciplined approach

- Optimism, Courage & Patience – remains the key

- Plan for two scenarios – 1) Immediate Recovery 2) Further fall over a period of time followed by recovery

- Minimizing ‘Regret’ should remain the key – balancing between regret of missing out if markets rally from here (optimistic scenario) vs regret of entering too early if markets correct further (middle path scenario)

- Staggered rule-based approach to deploying additional money

“The stock market is a device for transferring money from the impatient to the patient.”

Warren Buffet