The Budget 2018 proposal does not seek to leave more money in your hands. But by not pleasing you much, it has sought to keep its fiscal situation from deteriorating further. While we will discuss the benefits of a non-populist budget on the market and the economy in a separate article, here’s what the budget proposes for your finances.

Major tax changes

Imposition of long-term capital gains tax on equity and equity funds

For those new to equity markets and not used to equity taxation, the Budget may present a bit of a shock. From the next financial year, long-term capital gains on stocks and equity-oriented funds will be taxed. There are three aspects to this:

- Long-term is defined as a holding period of more than 12 months. This remains the same as before.

- Gains up to Rs 100,000 in a financial year will be exempt. The gains earned beyond this limit will be taxed at a flat and uniform rate of 10%. There will be no indexation benefits on gains. The table below explains this in simple terms with examples, for a holding period of 12 months and over.

- To prevent any retrospective taxation, and to cushion the impact, the tax proposal exempts all gains made up to January 31, 2018. Only the gains you make from this date onward will be taxed. How does this work? For that, understanding how the investment cost is calculated is necessary. In usual cases, the investment cost is simply the NAV or stock price on the date on which you were allotted mutual fund units or bought the stock. The gain will be the difference between the NAV of the sale date and the NAV of the purchase date. This rule changes for equity-oriented funds and stocks bought before 1st Feb 2018. The investment cost will be the higher of the following values:

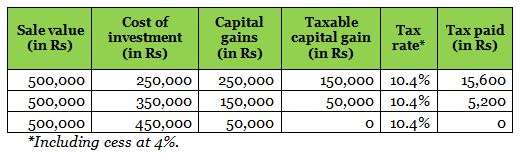

Let’s see this with an example. Say you bought a fund on 1st December 2016 at an NAV of Rs 100, and its NAV of 31st January 2018 was Rs 120. You sold it on 1st May 2018. Referring to the table above, the investment cost works out as below under different instances of sale value.

For any investment made from now, the above rule won’t apply and your gain is simply the sale less the cost.

Imposition of dividend distribution tax on equity-oriented funds

Dividends from equity-oriented funds were tax-exempt up to now. From the next financial year onwards, dividends will be taxed at 10% to bring it in line with the capital gains taxation rules. The dividend will be deducted by the AMC and given to you net of tax, as is the case with debt-oriented funds today. The NAV will reduce by the dividend amount and the tax.

How do these changes impact you?

Equity remains the asset class that can deliver superior return over the long term. In the past 15 years, equity funds across large-cap, diversified, and mid-and-small cap on average delivered 22.6% annualised returns. This compares favourably with fixed deposits, whose interest rates have never gone beyond 9.25% since 2003-04 in any timeframe, going by RBI data. Similarly, for those who think the tax-free status of PPF is better for tax-saving purpose, do not lose sight of the fact that PPF interest has been dwindling steadily and is at 8% currently. Compared with this, the long-term return on ELSS (tax-saving funds) remains superior even post the 10% tax on redemption.

Taxation on equity is still more favourable than other asset classes. Fixed deposit interest is taxed at slab rates. Yes, the 5% tax bracket has a lower rate, but as seen above, the differential between equity and fixed deposit returns is large enough that the lower tax rate does not result in higher FD returns. Besides, for those in the low-income tax bracket, it is very unlikely that their gains from equity will exceed Rs 1 lakh. In such a scenario, you will still pay nil tax on your equity funds and be taxed for interest income in other options. It is worth noting that pre 2004-05, equity long term capital gains were taxed at 20% with indexation or 10% without indexation. It is possible that over a period of time, equity will once again move to that structure. Be that as it may, the superior returns generated in equities in a tax-efficient way, makes it the best asset class to generate wealth. For those prone to a knee-jerk reaction of cashing out of equities fearing taxes, the question you need to ask yourself is where else you will generate superior returns in a tax-efficient manner.

Tax advantage of arbitrage funds fade. Arbitrage funds were used for short-term holding periods to escape taxes as holding beyond one year became tax-free. Their dividends were also being promoted as a tax-free income option. This allure of this option is drastically reduced. For those in the 5% tax bracket, arbitrage funds no longer holds good from tax perspective. For those in the 20% and 30% tax brackets, tax outgo may be only marginally more favourable with arbitrage funds. Note that arbitrage funds aim to deliver liquid-fund like returns and depend on available opportunities. Currently, 1-year returns of arbitrage funds are lower than liquid fund returns.

Dividend options no longer favourable. We have always taken a stand that depending on mutual fund dividends for regular income is unwise and that dividends are unpredictable. We’ve maintained that dividends from mutual funds are nothing but your own gains given back to you. With dividend from equity-oriented funds – and this includes balanced funds – now taxed, dividend and dividend reinvestment options are not viable. Though capital gains will be taxed, it happens only at the time of redemption. In the dividend option, taxes are cut every time a dividend is declared. This is true of dividend payout and dividend reinvestment. Besides, in the reinvestment option, it reduces compounding. If you have dividend reinvestment options in equity and balanced funds, it is best to switch out of them and into the growth option before 31st March 2018, if you are especially a long-term investor. You may suffer an exit load and/or short-term capital gains tax, but it would still be prudent from a longer-term tax perspective.

Keep portfolio churn to the minimum. Every redemption suffers a tax. If you keep redeeming funds each time you think it’s not doing well or it’s doing too well and you want to book profits, you will be paying tax henceforth, whether long-term and short term. Hence urge to switch funds constantly based on performance should be reduced.

Plan your redemptions. If you wish to plan your redemptions tax effectively, in future, you can consider staggering redemptions over two or three fiscals, instead of in one shot to gain a larger tax-exempt income. For example, selling (your long-term holding) in March and April of a calendar year would entail an exemption of Rs 200,000 (Rs 1 lakh each) since redemptions would fall in two fiscal years. Had you redeemed only in March, your exemption would be limited to Rs 100,000. This also holds to the logic of gradually moving out of equity as your goal approaches. Please note that we are NOT recommending this to avoid taxes now by churning your portfolio. This planning is for redeeming your money when you reach your goal.

Other key personal tax changes

- Education cess paid on taxes at 3% will be revised to 4%, and renamed health and education cess. Tax rates would then work out to 5.20%, 20.80%, and 31.20% in each slab under the new cess.

- For salaried employees, a flat Rs 40,000 will be available as standard deduction. That is, your income will be reduced by Rs 40,000 and then all applicable exemptions will come into play. Your taxable income will be calculated after all these. However, transport allowance of Rs 19,200 and medical reimbursement exemption of Rs 15,000 will be done away with. The standard deduction benefits all salaried employees, and more so for those who do not claim exemptions under transport and/or medical reimbursement.

- For senior citizens, up to Rs 50,000 per year on interest income from savings bank account and fixed deposits put together, will be exempt from taxes. Fixed deposits here include those from banks and post office accounts. TDS will also apply on income in excess of Rs 50,000. Earlier, TDS applied on FD income above Rs 10,000. FD income was also taxed in entirety; it was only savings account interest that was exempt up to Rs 10,000. With this move, instruments such as the Senior Citizens Savings Scheme become more attractive. Careful allocation between this option and debt funds can maximise tax benefits.

- For senior citizens with health insurance policies, the deduction claimable on premium paid will be increased to Rs 50,000 from the Rs 30,000 it was earlier. Similarly, expenditure on treatment of critical illnesses can be claimed up to Rs 100,000.