Wow or Oops!

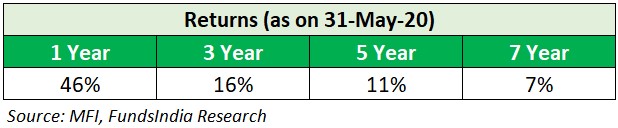

Let us look at the recent Gold ETF returns..

Wow! We need to invest in Gold ETF 🙂

But hang on. Let us rewind 1 year back..

Oops. We need to sell Gold 🙁

Same asset class – but two completely different interpretations!

Note: Returns of Nippon India ETF Gold BeES (largest Gold ETF with AUM above Rs. 3,500 crs) is used for illustration

How do we form our return expectations?

In the long run, the usual narrative is that Gold is expected to be a good inflation hedge (i.e it will beat inflation). But as always let us verify if there is evidence to prove it..

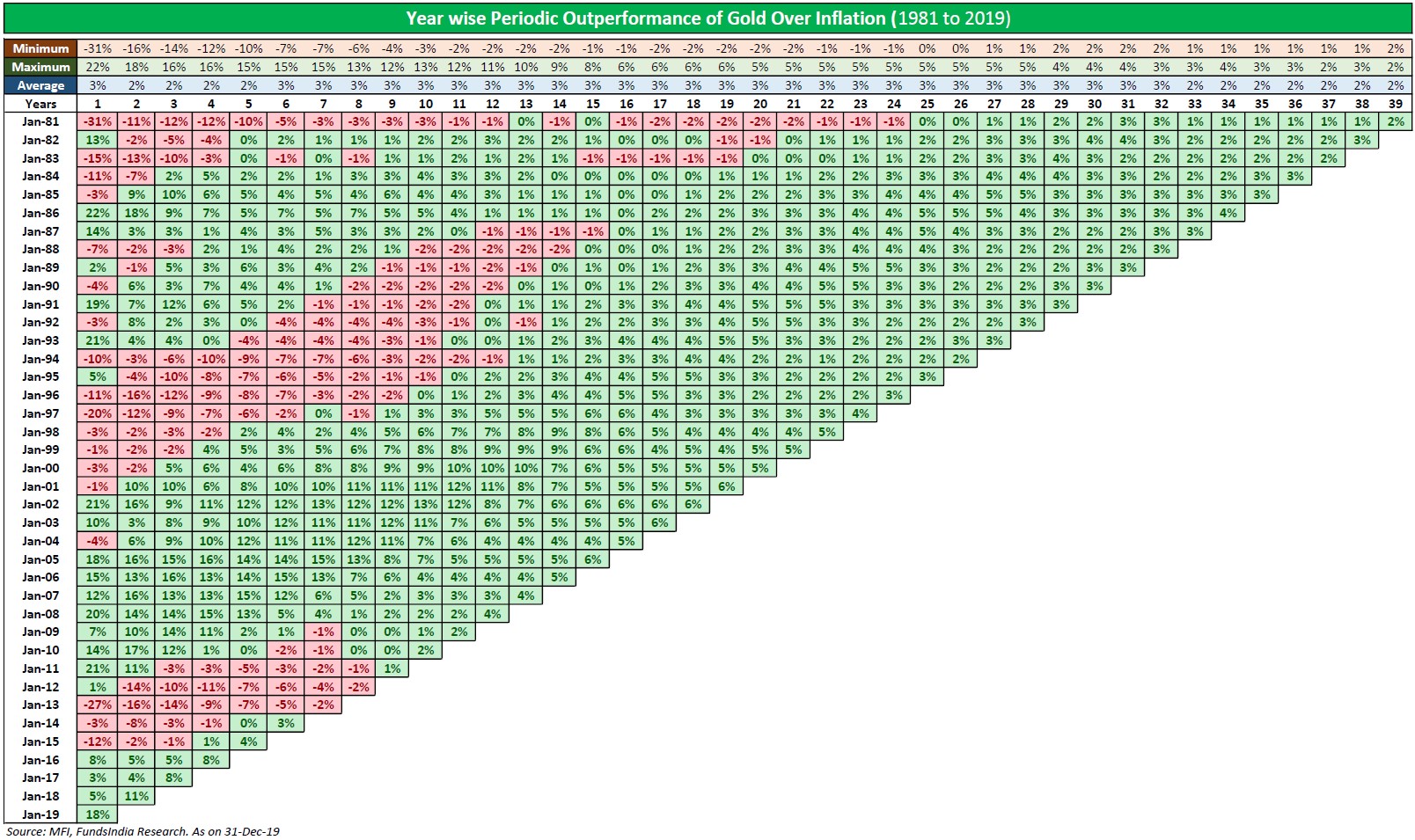

The table shows the outperformance of Gold vs Inflation (we have used the Cost of Inflation Index) for an investor starting at different years – 1981,1982..and so on till 2019. The columns denote the investment time frame from 1 year to 39 years.

As seen from the above table, over long periods of time, Gold has indeed provided higher returns over inflation as indicated by the dominant green shades as you extend the time horizon..

Cool! The assumption of gold as an inflation hedge holds true as seen from the past history of gold prices.

But this leads to the next question –

Why should Gold be an inflation hedge?

Inflation is often understood as the rise in the prices of goods and services over time. However, this is actually the symptom of inflation. Inflation can happen if the money supply in an economy grows faster than the economic output under otherwise normal economic circumstances. It results in more money chasing the relatively same amount of goods and services, thus pushing up prices. Today, currencies can be created in large quantities by central banks and governments at a much faster rate than goods and services are produced and brought to the market. That is why prices rise steadily over time.

Gold is often used to hedge against inflation because, unlike paper money which can be printed excessively, its supply doesn’t change much from year to year. Sample this – the growth in gold supply has changed little over time – increasing by approximately 1.6% per year over the past 20 years (source: goldhub.com).

Thanks to its relatively inelastic supply, gold preserves its purchasing power, thus serving as a hedge against inflation over long periods of time.

Ok. So that leaves us with two conclusions-

- Over the Long Term (10-15 years) Gold has provided returns above inflation

- Long Term Return Expectation = Inflation + 1-2%

But if you notice we sneakily used the word ‘long term’. While the return expectations hold over long periods of time, what about shorter time frames?

We can notice that while gold has done well over the long run, it also has intermittent periods where it didn’t do well.

Here are few examples of such periods.

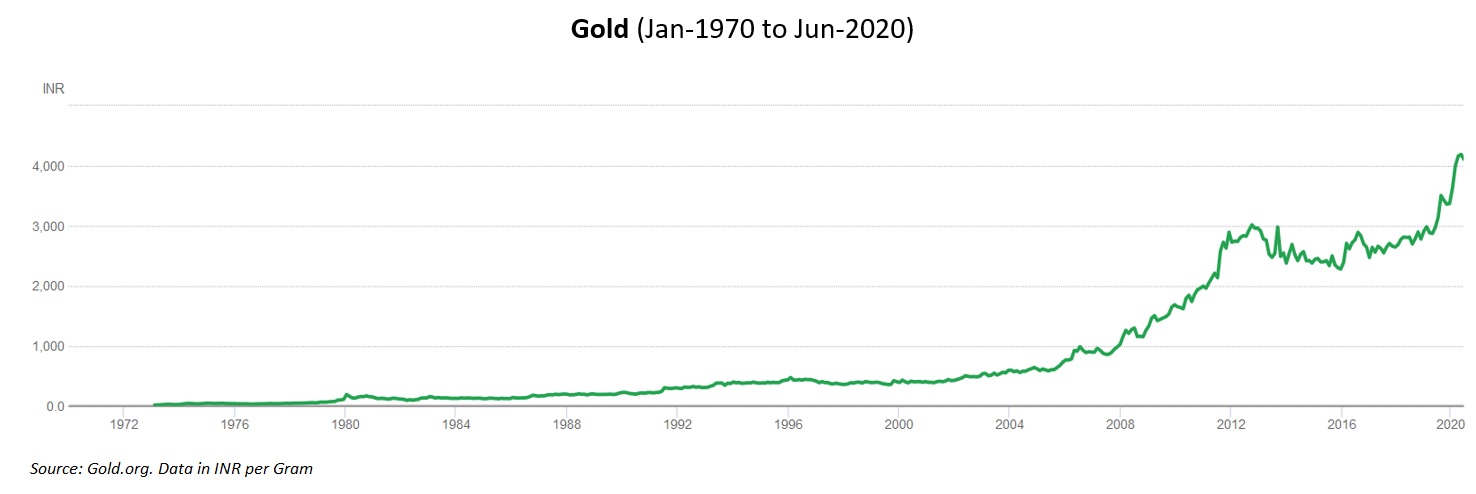

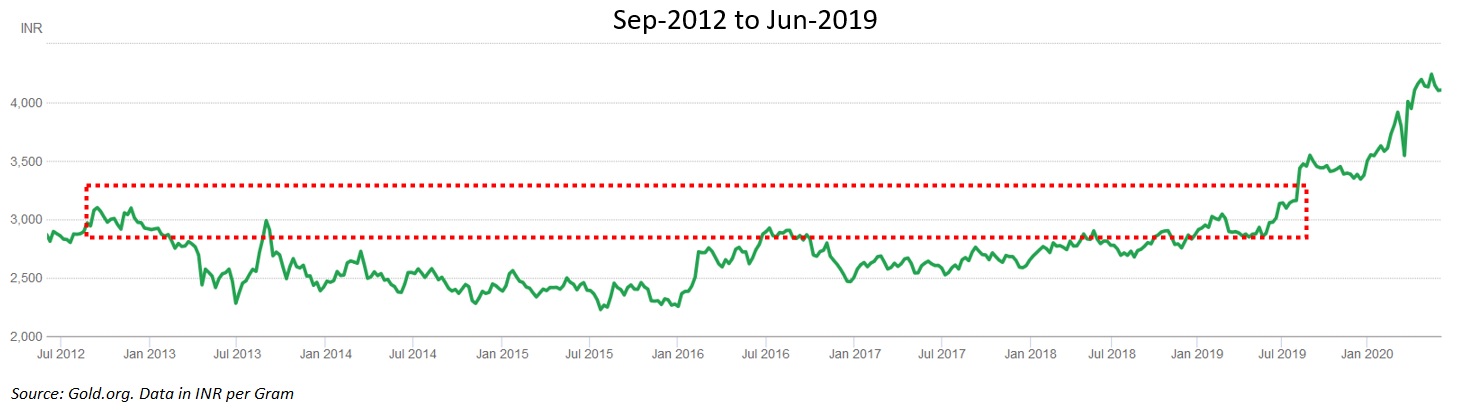

1980-1990: It took gold another 10 years to hit its 1980 peak once again

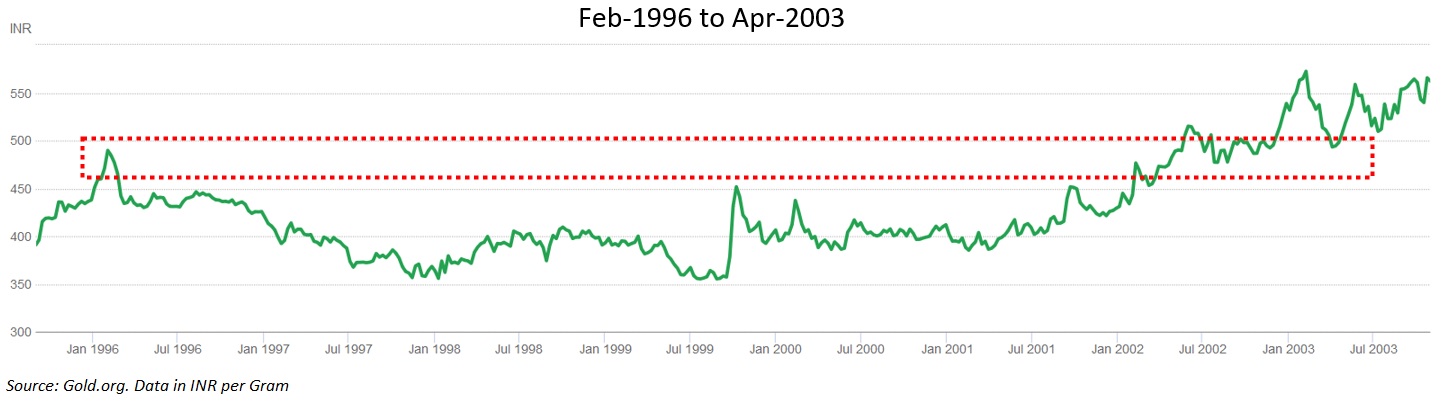

1996-2003: It took gold another 8 years to hit its 1996 peak once again

2012-2019: It took gold another 7 years to hit its 2012 peak once again

As seen above, there have been several instances where Gold returns were dismal over extended periods of time.

So let us modify our conclusions a bit:

1. Over the Long Term (10-15 years) Gold has provided returns above inflation

2. Long Term Return Expectation = Inflation + 1-2% but…

3. Gold also often goes through extended periods of subdued returns

Ok! Now I can hear your next question –

But what leads to these periods of subdued returns or supernormal returns?

Drivers of Gold price

When we in India invest in Gold, there are two major factors which determine our returns.

1. The global price of Gold which is denominated in US Dollar

2. The exchange rate: USD-INR

(there is also customs duty set by the government of India and physical premium/discount which we will ignore for simplicity as the above two are the significant drivers)

Thus, Gold price in India = Gold price in USD * USD-INR

Let us get done with the relatively easier part of the equation: USD-INR movement

Part 1: Long Term INR depreciation trend?

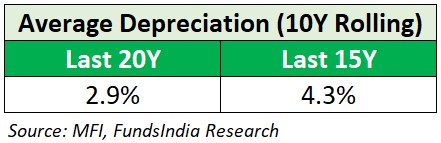

3-4% has been the historical range of INR depreciation vs the USD over long periods of time. This is usually in line with the inflation differential between India and the US.

So we can assume that going forward our long term return expectation can be roughly:

Gold Returns (in INR) = Change in Gold Price (USD) + ~3-4% from INR depreciation vs USD

Part 2: What drives Gold price (in USD)?

First an honest submission. Out of all the asset classes, we find Gold returns to be the most difficult to understand. This is primarily because Gold doesn’t have an underlying cash flow like the other asset classes (Dividends/Profits in Equity, Interest payment in Fixed Deposits and Fixed Income, Rent in Real estate etc). Hence valuing gold becomes extremely difficult.

OK, gold is not a cash-generating asset. Fair enough. But as a metal it must be a commodity, right? Can’t we analyze Gold like how we evaluate other commodities like Silver, Copper etc?

Unlike other pure commodities, gold plays a dual role – both as a commodity and a currency.

When looked at like a commodity – it derives its value from its use as a raw material to meet a fundamental need – which in the case of gold is for jewelry-making or manufacturing certain medical, industrial and technological products. So understanding demand and supply can give us a sense of pricing of gold as a commodity.

When looked at like a currency – it’s a medium of exchange and a store of purchasing power. Gold for several centuries has been perceived to be a store of value especially during crises or when you lose faith in paper currencies and as long as the perception remains, gold also acts as a quasi-currency.

So to evaluate Gold as an asset class for investing, we need to take into account both its role as a commodity (used for jewellery and technology) and currency (store of value)!

2.1. Drivers of Gold Prices as a Commodity:

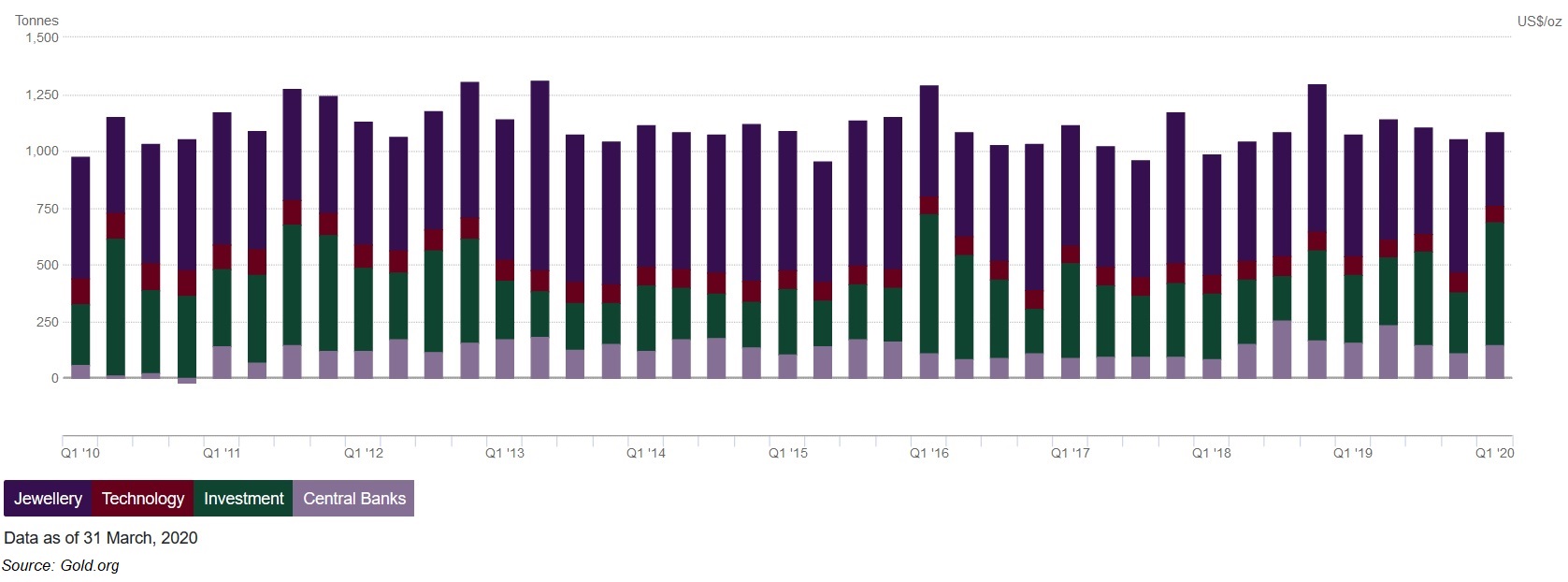

a. Demand – Worldwide Jewellery and Industrial Demand

As with most commodities, an excess of demand for gold (normally for jewelry-making, or manufacturing certain medical, industrial and technological products) drives up the gold price (assuming supply is constant). On the other hand, a weakening of demand often has the opposite effect on its value, sending the price lower (assuming supply is constant).

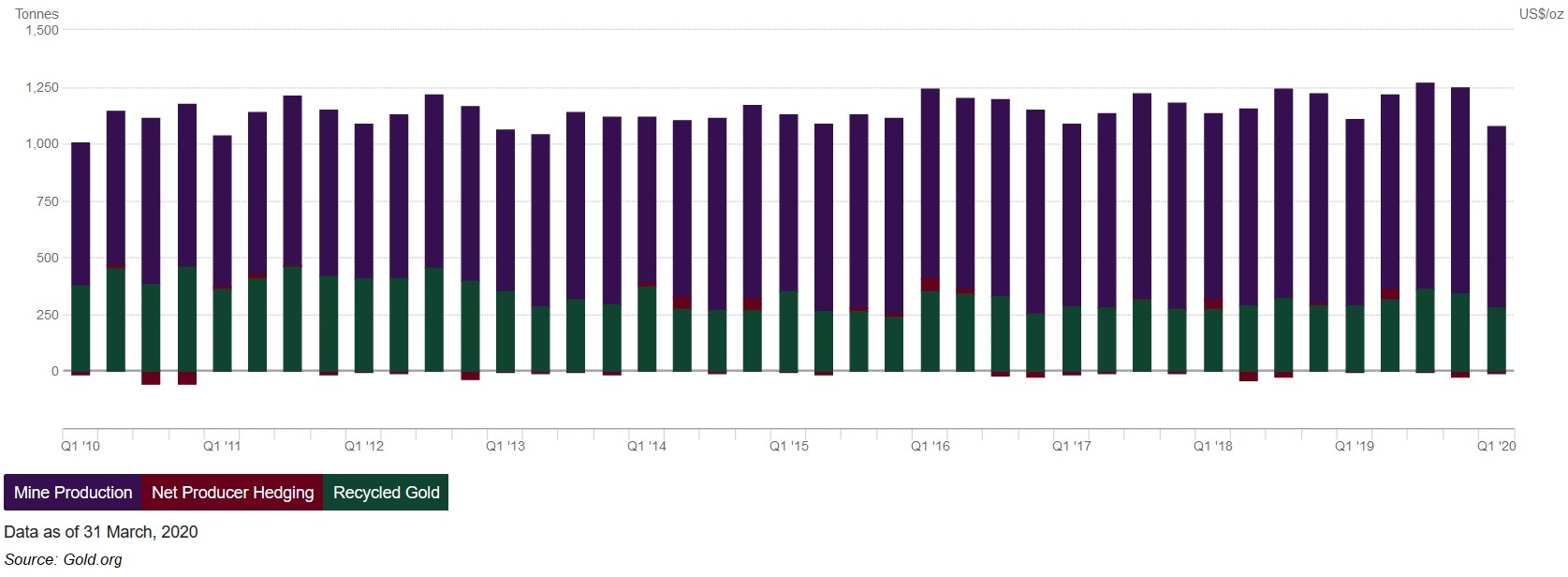

b. Supply

1. The gold supply chain is truly global. Gold is mined on every continent except Antarctica, refined into bars and coins in numerous countries, and distributed far and wide. This geographical dispersion brings stability to the gold market.

2. Gold is almost indestructible. Practically all gold that has ever been mined still exists in some form. So gold is much less prone to production shocks as the price of gold does not depend so much on current production. Any shortages can be relatively quickly fulfilled by recycled gold from the above-ground stocks.

3. Any positive supply shocks (sudden increase in mining output) also affect the gold prices in a limited way, because the annual mining production is only a tiny fraction of the total gold holdings.

However, if Gold Prices reduce significantly to below than production cost (cost for taking gold out of the mines) – supply constraints may lead to higher prices.

2.2. Drivers of gold as a Currency:

a. Risk and Uncertainty

Gold is considered a safe haven asset – an asset which does well in a crisis scenario or financial turmoil. So whenever there is a crisis usually Gold prices go up as investors flock to Gold given its safety haven status.

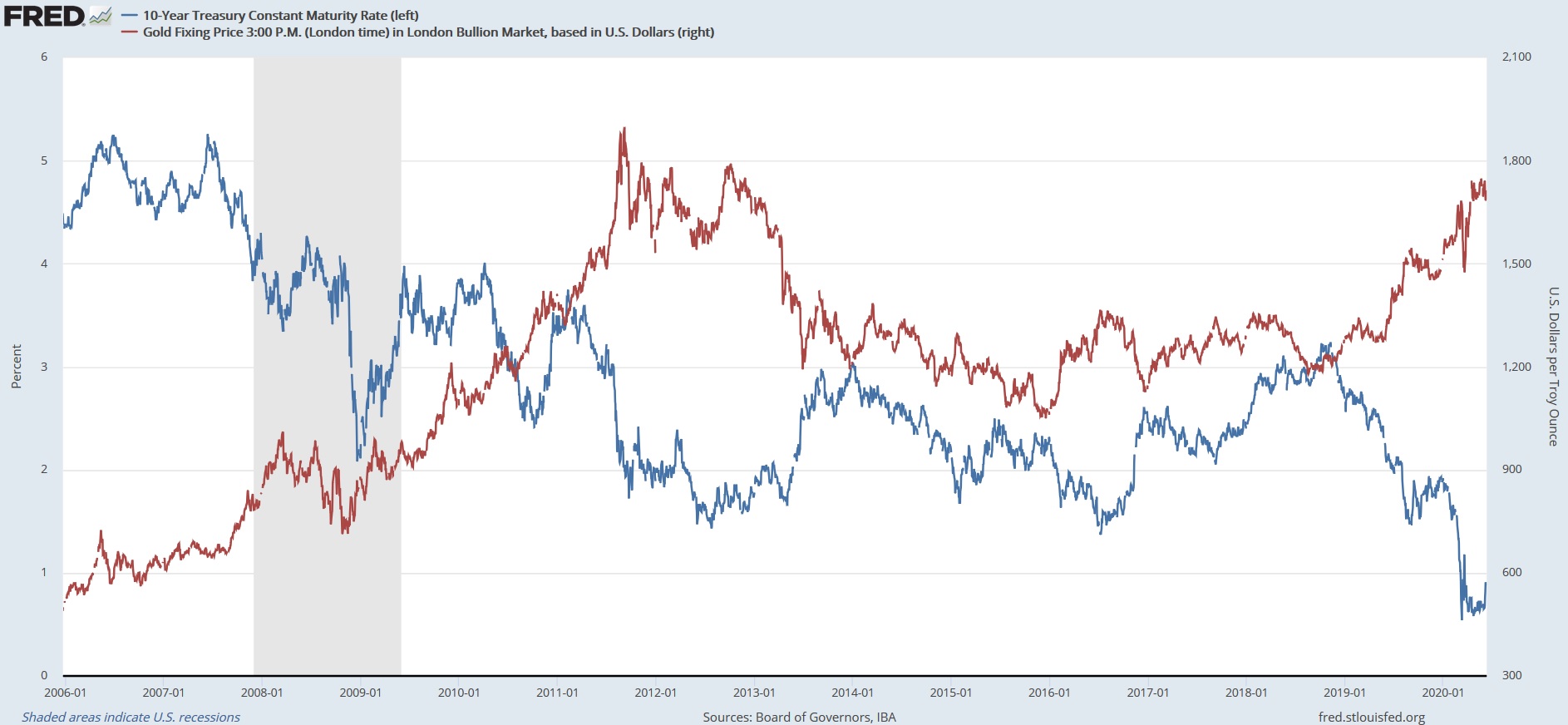

b. US Real Interest Rates

US real yield = US 10Y Treasury yield – US Inflation

Eg: If a bond yields 2%, but the inflation rate is 3%, the real yield on that bond is negative 1%.

Historically it has been seen that, when real yields go down – gold goes up, and when real yields go up – gold goes down. This correlation explains why inflation is gold’s best friend while rate hikes are its worst enemy.

But the million dollar question is why does this happen?

When it comes to safety, global investors have two popular choices – 1) US 10Y Treasury bonds 2)Gold

Now if the real yield of US 10Y Treasury bonds is high then it makes non-interest bearing Gold relatively less attractive and investors would likely want a lower price compared to the long-run estimated real value of Gold. Conversely, when real yields are low, the opportunity cost of owning Gold drops and investors would likely be willing to pay a higher price relative to the asset’s long-run estimated real value.

For those interested here is an interesting paper published by a reputed global investment firm PIMCO which explores more on this topic.

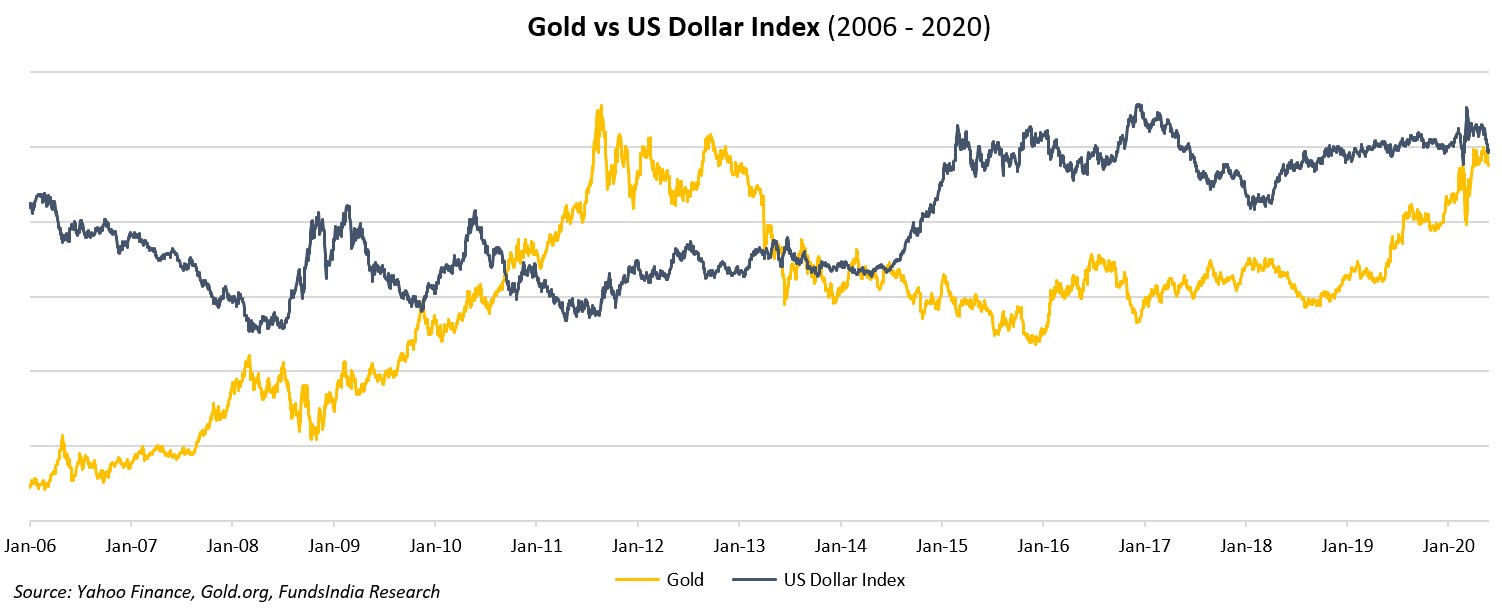

c. Value of the USD Currency

US dollar typically trades inversely with gold. When the value of the dollar increases relative to other currencies around the world, the price of gold tends to fall in U.S. dollar terms. It is because gold becomes more expensive in other currencies. As the price of gold moves higher, there tend to be fewer buyers, in other words, demand recedes. Conversely, as the value of the U.S. dollar moves lower, gold tends to appreciate as it becomes cheaper in other currencies

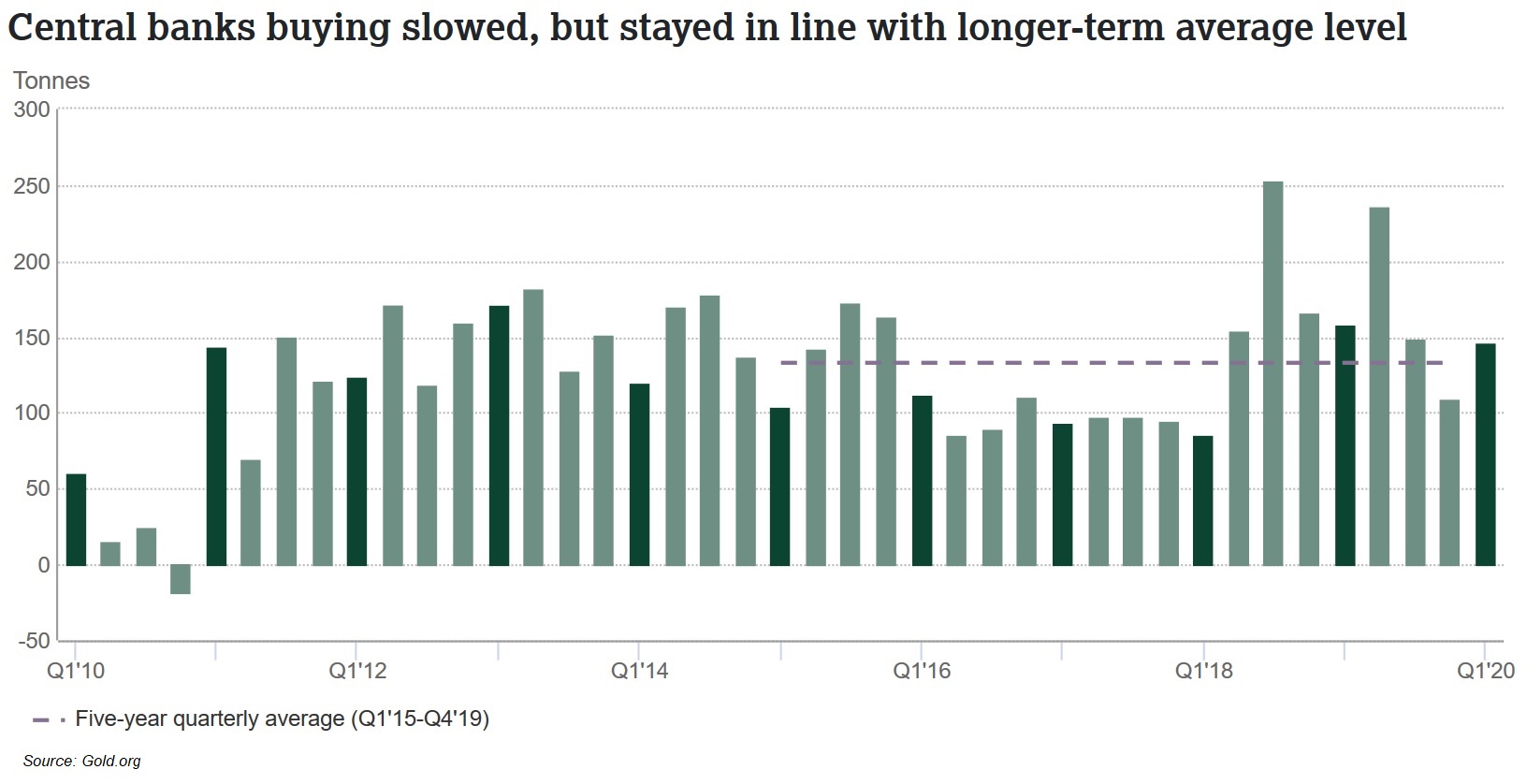

d. Central Banks Buying Gold for their Reserves

Many of the world’s gold reserves are controlled by central banks within developed nations, in locations such as Europe and North America. As a result, these banks wield immense pricing power in global gold markets. If the banks suddenly increased or reduced their gold exposure at once, even slightly, this would have a magnified effect on the gold price. Central banks therefore rely on a joint (though unofficial) commitment to refrain from unilaterally engaging in large-scale gold sales that could destabilize global markets.

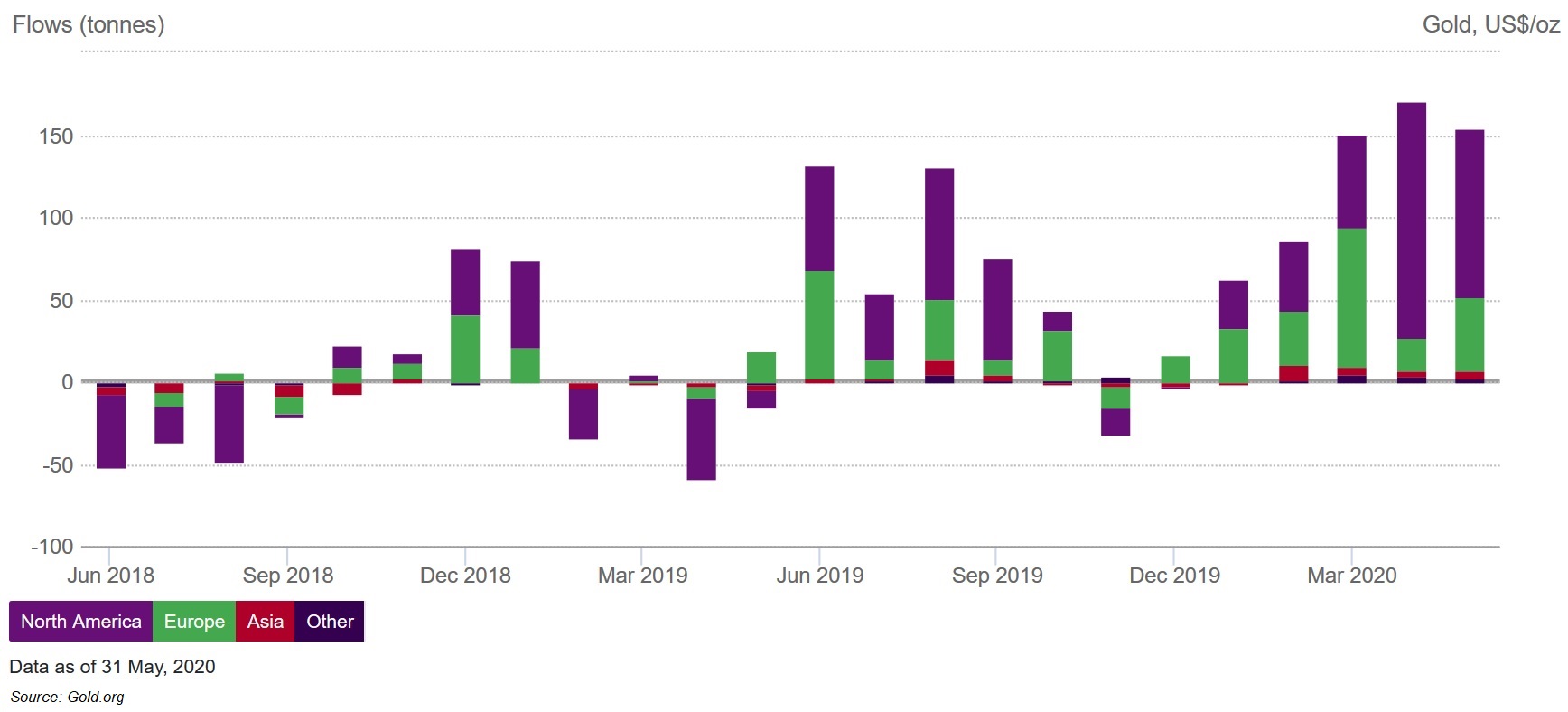

e. Global Gold ETFs

With the launch of gold ETFs in 2004, gold has increasingly become a liquid financial asset. But over much of history, the price of gold was either fixed or gold was a relatively illiquid physical asset held by a small minority of investors. Today the marginal price of gold is largely set by financial demand.

While exchange traded funds are generally intended to mirror the gold price rather than influence it, many large ETFs hold a significant amount of physical gold. Therefore, the inflows and outflows from such ETFs can affect the metal’s price, by altering the physical supply and demand in the market.

Predicting Gold Price

Now for someone trying to predict Gold prices over the short term, you need to get all the above right. Phew. Good luck with that!

How to think of Gold allocation within a portfolio?

Gold can enhance your portfolio in three key ways:

- Portfolio Diversification: Act as an effective portfolio diversifier and helps reduce overall portfolio losses in times of crisis

- Inflation and Currency Hedge: It can serve as a hedge against inflation and rupee depreciation

- Reasonable Returns: Gold historically has generated long-term inflation + 1-2% returns

The way we think about Gold, it is an asset that you buy and pray it doesn’t do well because that would mean the remaining portion of your portfolio allocation in other asset classes will most likely not do well.

This is more like wearing a helmet when you drive a bike. While you wear a helmet, you really pray you don’t want the helmet to come into action – as only in an accident will the helmet serve its true purpose.

Similarly if Gold returns are very high, then usually it means that – we are in the middle of some crisis scenario like the current Covid-19 crisis. This will also mean many of your other assets such as your equity allocation, own business/sector etc will not be doing well.

So,

Portfolio Recommendation

For investors who don’t have existing exposure to gold via existing jewels or coins (most of us have it in some form or the other given our cultural context), we would recommend limiting gold exposure to 5%-15% of overall portfolio.

While the recent past shows strong return momentum in Gold, you need to remember that there were several instances in the past where Gold had extended periods (7-10 years) of weak returns.

The short term returns will be driven by: Demand for Gold (Jewelry and Industrial) + US Real Yields + USD-INR movement + Central Bank & ETF Demand + Crisis Events. This is something we don’t have the expertise to predict.

Summing it up, if you want to invest in gold, then you can consider a small portion (5-15% of overall portfolio) to act as a diversifier to ‘crisis scenarios’ and long term (10-15 year) return expectations can be anchored to Inflation + 1-2%.

Gold has always given a sub optimal return. Even globally, the value of gold arise when there is a crisis in the world. So it is a thing of crisis.

In India, it rises with the depreciation of INR which is roughly 3 to 4% p.a.