When we look at some of the mutual fund factsheets or market presentations or listen to a fund manager speak, we often come across the term Overweight/Underweight a sector or a stock holding. Let’s discuss what this means.

An index has a fair representation of all the important sectors in the economy. And all actively managed equity mutual funds would be benchmarked to an appropriate index. Just because a fund is benchmarked to an index does not mean all the sectors of the index have a similar representation in the fund as well. If they did, then they will be more passively managed index funds and not active funds. A fund manager seeks to generate higher returns than the benchmark by taking active calls beyond the benchmark. Hence funds tend to be overweight or underweight sectors and stocks compared with the benchmark. The term overweight/underweight a sector implies that the fund may be holding a higher or lower proportion of a sector when compared with the benchmark.

When would a fund manager be overweight a sector? A fund manager would be overweight a sector when he is bullish about the prospects of a particular sector and is of the opinion that the sector will do well; or when the stocks in the sector are expected to deliver better results compared with other sectors going forward. By how much the fund manager is overweight a sector depends on its future prospects and outlook. The top overweight sector would be that sector where the difference between the weight of the sector in the fund and index is the maximum. When the fund manager is significantly overweight on a sector, it means he is taking a bet that the sector will deliver more than what it presently does.

Similarly, a neutral representation of a sector in the fund indicates that the fund manager expects a status quo on the sector’s performance and simply wants to play safe by holding the sector as much as the index holds. Conversely, a fund manager may have a negative view on certain sectors that are there in the index and may therefore either reduce weight or completely not hold stocks in those sectors. The more a fund manager goes underweight on a sector, the fewer prospects he/she sees in that wither because it is overvalued or its propsects seem diminished.

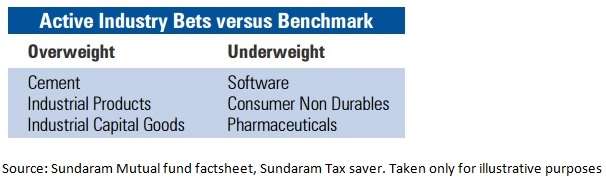

It can be noticed in the above table that the fund manager has overweight positions in cement, industrial products and industrial capital goods indicating that he expects these sectors to do well going forward. Similarly, he appears to be less sanguine about sectors such as IT, consumer non durables and pharma and does not expect these sectors to perform as well.

Why would the fund manager be taking such calls?

This is one of the methods of generating returns more than the index. By being overweight in a sector the fund manager seeks to increase contribution of sector towards the funds’ overall return, when compared with the benchmark. This, of course if the call pans out well. The reverse is also true when the fund manager reduces exposure. When such positions work well, the fund outperforms its benchmark handsomely.

There may also be instances when the fund manager may go wrong with his sector calls. He may be underweight an outperforming sector and overweight a badly performing sector. In such circumstances the funds tends to underperform.

So the underweight and overweight positions of a fund vis-à-vis its benchmark helps to broadly gauge the thought process of the fund manager regarding the performance of the sectors and his expectation regarding the sector.

Informative.

Informative.