If you are wondering if there is any upside left in the equity market after the 2014 rally and the flash rally this month till date, our answer to it is that we believe that the story may just have begun.

We had put out a quick note last week when RBI made a surprise rate cut of 25 basis points and opined that the rate cut, while obviously expected to boost debt markets, would be a more significant event for the equity markets.

This week, we’d like to elaborate on how this could be a tipping point for a more sustained turnaround in the economy and corporate earnings and what you should be doing to capitalise on this.

Lower current account and fiscal deficit, a more stable rupee and lower inflation were all positive macro economic developments that led to the Indian equity markets outperforming with a 30% return in 2014. That is old wine now.

The rate cut – a directional shift

In 2014, while the improving macro numbers gave reason for the equity markets to cheer, the RBI clearly did not get sufficient comfort to go for a rate cut. The RBI governor had time and again spelt that once the monetary policy stance shifts, further policy actions will be consistent with such a stance. Seen from this angle, the rate cut last week, although just 25 basis points, can finally be seen as an endorsement of an easing interest rate cycle.

Even if we can expect measured cuts over several quarters from now, we think the directional shift is significant for two reasons:

One, sustained periods of lower interest rates are also periods of heightened urban consumption and growth which in turn buttress economic growth.

Two, a sustained rate cut also means lower cost of capital (cost of borrowing for companies), a key for improving the investment momentum by the private sector. As we see today, leaving out external risks, lack of investment in the private sector is the only (significant) missing link to the India growth story and lower cost of capital, together with reforms can put that part of the jigsaw puzzle in place.

So what did the markets not factor in last year? We think the markets remained uncertain about a sustained lower inflation number as the RBI kept a neutral rate stance even as inflation and deficit numbers improved. Also, the markets did not really reward the cyclical sectors as much as we thought it did (in the following section, you will see why we say this).

Hence, we think the upside coming from rate cuts were not fully factored earlier.

What the markets factored

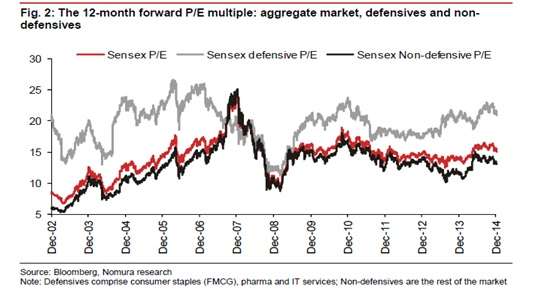

True, markets are not cheap. But neither are they expensive. As against the 5-year average of 15.1 times price earnings multiple, the Sensex (Bloomberg consensus) is trading at 15.3 times its one-year forward earnings. That means, it is not cheap but nor is it expensive. Compared with the 25-30 times it traded at in 2000-01 and 2007-08.

Besides, the below data from Nomura provides some interesting insights on what the markets factored in while rallying last year. Clearly, the defensive sectors (FMCG, pharma, IT) in the Sensex are much more expensive than the non-defensive (cyclical) segments. And the gap between defensive and non-defensive continue to be reasonably wide.

The equity market clearly saw the uncertainty stemming from higher inflation, higher interest rates and lower investment activity in the cyclical space and did not reward these sectors enough, last year, to narrow the gap in valuations between these 2 segments.

With the current rebound in the economy expected to largely benefit cyclical growth stocks, a narrowing of this gap would mean some more re-rating in the cyclical space.

Uptick in activity

The above data suggests that the equity markets remained slightly skeptical about the cyclical space and rightly so since there appeared little evidence of any improvement in corporate earnings growth or investment activity by companies.

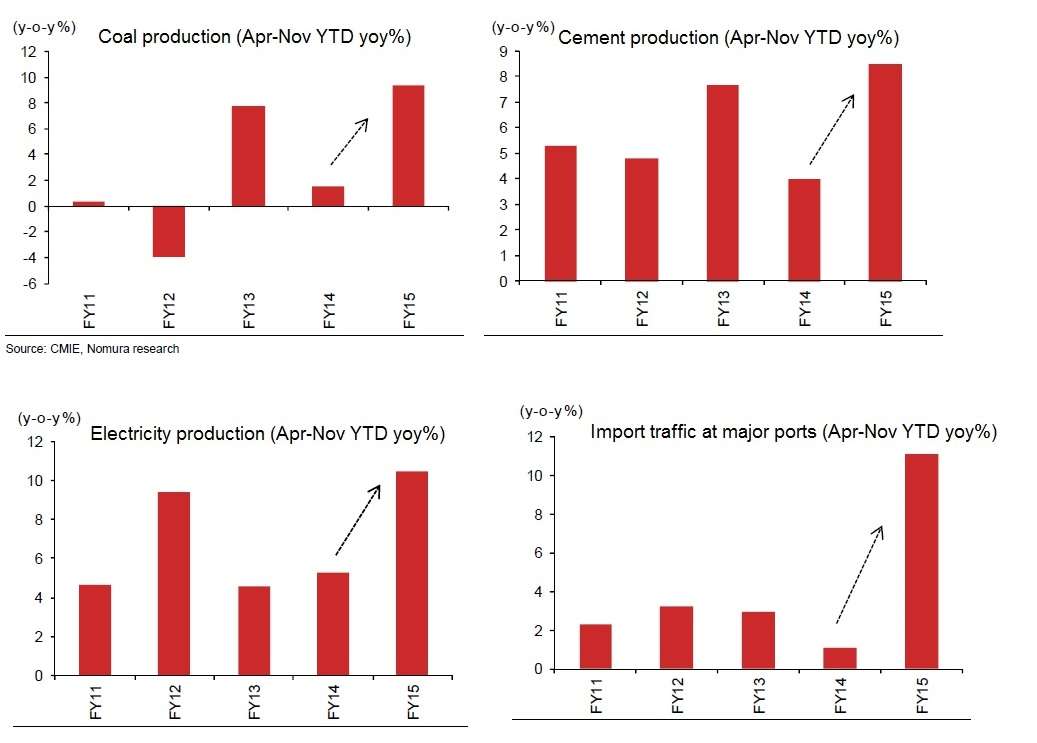

However, there are other less direct data points from the manufacturing indicators of PMI and IIP that suggest that economic activity and therefore corporate activity is indeed on the uptick. We give below some interesting data we sourced to bring out this shift.

Clearly, the increase in production of some of the key inputs used by the manufacturing sector and also an increase in import activity (signifying a possible uptick in demand for inputs by companies) all suggest that the manufacturing space may be seeing a slow rebound. This is also corroborated by an increase in the HSBC Purchasing Manager’s Index (PMI) for India.

While private investment activity could gain pace with some delays, we think an increase in spending by government (with easing deficit) and an already visible capex spending plan by public sector companies can set the ball rolling for the private companies to join the momentum. Rate cuts, could only further buttress such a shift.

The perceived risks

The question of whether FII flows will sustain is important for equity markets such as India as FIIs drive our markets. While this remains an inherent risk at all times, we see 2 mitigating factors at this juncture.

One, the clear differentiation in the premium afforded to some emerging markets will further become apparent this year. Countries that make a conscious effort in stabilising their economy with policy measures can be expected to get a premium for their equities. This trend is visible from mid 2014. India, clearly, appears to be among the top in such a list.

Two, Asian countries such as Malaysia, Indonesia, Thailand and India which have the highest oil subsidy per person (source International Energy Agency data as of 2013), have benefitted the most from a global fall in oil prices.

Countries such as India have been prudent not to transmit the fall to consumers and have instead chosen to ease their deficit situation and improve tax collection (hike in excise duty). This further adds weight to its prudent economic measures.

The other perceived risk of a hike in Fed rates too, seems less threatening for India at this juncture for the following reason: it is the real rate differential of India with the US that typically drives foreign money flows into India.

The short-term real rate differential (3-month treasury rates) at 4.9 percentage points (as against 2 percentage points in May 2013) provides sufficient cushion for any shocks from US rate hikes. The long-term (10-year) rate differential too is at a comfortable 2.5 percentage points (negative in mid 2013). This positive real rate differential is likely to prevent any sudden exodus of capital.

What’s in it for you

To cut the long story short, we believe the equity markets could be ripe ground to start out serious long-term wealth building. While we are not advocating timing the market, we would like to ensure that you do not miss the positive signals that lay the ground for a bull market. Even as we say this, we do not rule out any intermittent corrections. Those are necessary and will keep the equity markets healthy.

For those of you who are in the game for the long term, we would recommend upping your mutual fund SIPs at this juncture, simply to ensure that you invest more now but still in a disciplined manner. For those who can take plenty of intermittent shocks and have a 10-year plus view, lump sums, to our mind, can do no harm.

Even as I say this, please ensure that you have a well-balanced asset allocation and not go all out on equity. Our Select Funds have been chosen keeping the above factors in mind and picked based on portfolios that are well poised to make good the rebound. Choose well, based on your risk appetite or seek our advisor’s help.

Very well researched article. Liked the risk part in the piece, with strong supporting data. Could’ve been better if this added the near-term prognosis for cyclical/defensive based on P/E run-up and due to rate-cut in rate-sensitive sectors. My assessment is PE would moderate over the later part of 2015, while near-term impact will be more on both sectors due to sentiments (well, I am just a novice!!

Bharani, thanks for your comments. Your suggestions are noted. Appreciate it. Vidya

I know these question I am about to ask have no relation to this article. But what are views on UTI Balanced Fund & ICICI Pru Advantaged Balanced fund. I invested in these funds in July 2015. Should I exit now ? Are these good funds ?

Hello Rajiv, Thanks you for writing to us. I request to please route any fund or portfolio specific query through your FundsIndia account (click help tab and choose advisory appointment and mail us your query), if you are a FundsIndia investor. Since this would amount to advice/opinion, we have a process to follow and track, if questions are routed through your account. thanks, Vidya

I have summited a query ,like you have said.

I know these question I am about to ask have no relation to this article. But what are views on UTI Balanced Fund & ICICI Pru Advantaged Balanced fund. I invested in these funds in July 2015. Should I exit now ? Are these good funds ?

Hello Rajiv, Thanks you for writing to us. I request to please route any fund or portfolio specific query through your FundsIndia account (click help tab and choose advisory appointment and mail us your query), if you are a FundsIndia investor. Since this would amount to advice/opinion, we have a process to follow and track, if questions are routed through your account. thanks, Vidya

I have summited a query ,like you have said.

Very well researched article. Liked the risk part in the piece, with strong supporting data. Could’ve been better if this added the near-term prognosis for cyclical/defensive based on P/E run-up and due to rate-cut in rate-sensitive sectors. My assessment is PE would moderate over the later part of 2015, while near-term impact will be more on both sectors due to sentiments (well, I am just a novice!!

Bharani, thanks for your comments. Your suggestions are noted. Appreciate it. Vidya