In a word, yes. A debt fund can deliver losses. You would have noticed it last week, when you saw your one-day return in the red. Why does this happen? Debt funds can deliver losses in the three instances:

1. When funds hold instruments whose prices fluctuate daily (as they are linked to markets), they can generate a loss on days when debt markets fall. The debt markets may fall or rise based on interest rate movements (or expectations of interest rate change). This is the most common reason for a fund to generate losses.

2. In some cases, where the credit rating of an instrument that the fund holds is downgraded and the instrument is listed, they will see a drop in their prices. When such instrument is unlisted and the instrument’s price needs to be reset to reflect the higher risk, a fund’s NAV will see a fall. This is a less common event.

3. In few cases, when an instrument that the fund holds has defaulted, the fund must reset the instrument’s price to market price or its current worth today. This will also result in NAV fall. This event occurs rarely.

Except in the case of the third event above, this fall in market prices and NAV does not mean that the fund is losing money. It’s a paper loss (since it is just marked to market) and not a real loss, unless the fund sells the instrument at that time. Regular receipt of interest on the underlying instrument or an improvement in price will once again bring the NAV to the profit zone.

The fact is there are funds that do not fluctuate heavily daily and there are funds that fluctuate in the short term but even out in the medium to long term. Thus, you need to match your requirement with the type of fund. Equally important, you need to hold the fund for the required timeframe if you are to get the best of it.

How do debt funds make returns? One way is by holding the debt papers and earning the interest due on it, called accrual strategy in finance-speak. Income, short-term, ultra-short-term, and liquid funds follow this for a good part. The second way is to bet on interest rates and bond price movements and so make gains, called a duration strategy. Gilt funds and dynamic bond funds play on duration; dynamic bond funds change their strategy depending on the interest rates.

Why do fund NAVs fall or rise? Bonds trade on exchanges, just like stocks. If interest rates are on the rise, existing bonds become less attractive as newer bonds carry higher rates. Thus, their prices thus fall until they are in line with new yields. The reverse happens when interest rates are falling. Funds have to show the market value of their holdings. Barring liquid funds, all funds have at least some part of their portfolio that is traded and so reflect market value.

For much of last year, bond prices rallied handsomely as rates fell. This allowed gilt funds and dynamic bond funds to post double-digit returns that caught your eye and investments. The recent monetary policy gave cues for direction of interest rates and ruled out possibilities of near-term rate cuts. This caused bond prices to fall due to a potential upward movement of rates and the possibility of the rate cycle getting closer to the finish. As bond prices fell, so too did fund NAVs.

Why did some funds fall more than other funds? The volatility in NAVs of funds will broadly depend on two factors: one, whether the underlying instruments have longer maturity or shorter maturity and two, whether the instruments are traded in the market or not. Longer the maturity and more traded the instruments – the more the fund’s NAV fluctuates based on market movements.

Government bonds are the most traded and liquid and have longer maturity. Gilt yields assimilate changes far quicker and far more sensitively (given their longer maturity) than any other bond. A fund that holds a significant proportion here will see more activity in its NAV. This is why the falls in long-term gilt funds and dynamic bond funds were steeper than other categories on the day of the monetary policy. Outside pure gilt funds, dynamic bond funds are the most volatile debt category. AAA-rated corporate bonds are also highly traded and these also reflect changes in rates, though not as much as gilts as their maturities are shorter. Income accrual funds are slightly more volatile than credit opportunity funds as the former holds more listed securities. Credit opportunity funds, although not volatile, have a different kind of risk, arising from their own credit profile.

A short-term fund would see smaller deviations in NAV than a long-term fund. Thus liquid and ultrashort term funds remained unaffected on monetary policy day, short-term and credit opportunity funds saw slight dips, and income accrual funds fell a little more.

What happens when a fund makes losses? A loss in a debt fund is not like a loss in an equity fund. A debt fund loss reflects only the market value of the debt papers. These debt papers are not going to deliver losses for the fund itself, unless it exits the bond at a loss. The fund still earns the interest due on them, and at the time of maturity receives the principal back. The loss, thus, is extinguished. This is where the holding period is of importance because you need to give the fund time to allow its interest accrual to play out.

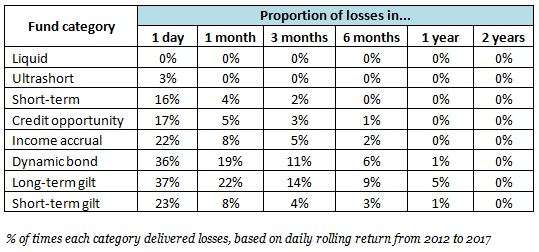

Why is timeframe important? The table shows the proportion of times different fund categories have delivered losses across timeframes. The returns for each timeframe has been rolled daily for five years, a period that has seen at least one rising and one falling rate cycle.

Notice how the proportion of losses diminishes according to period for each category. If you enter a dynamic bond fund with a 3-month timeframe, you could well lose money. Respecting timeframe is important if you are to get the best out of your investment. The fund needs to hold the papers for the required timeframe to earn the yield and in consequence, so do you. Dynamic bond funds need the time to allow the rate cycle to play out fully, book the gains and protect return. Note that gilt funds are purely a play on the rate cycle and require timed entry and exit.

Notice how the proportion of losses diminishes according to period for each category. If you enter a dynamic bond fund with a 3-month timeframe, you could well lose money. Respecting timeframe is important if you are to get the best out of your investment. The fund needs to hold the papers for the required timeframe to earn the yield and in consequence, so do you. Dynamic bond funds need the time to allow the rate cycle to play out fully, book the gains and protect return. Note that gilt funds are purely a play on the rate cycle and require timed entry and exit.

Thus, when investing in debt funds, ensure that the fund suits your timeframe. Once you invest, remember to stick to that timeframe.