Thinking Fast and Thinking Slow

3 Simple Questions

Here are three simple questions. Let us see how quickly you can answer these questions.

- You are a participant in a race. You overtake the second person. What position are you in?

- If it takes 5 machines 5 minutes to make 5 bottles, how long would it take 100 machines to make 100 bottles?

- A bat and ball together costs Rs 110. The bat costs Rs 100 more than the ball. How much is the cost of the ball?

Time for the answers..

- The intuitive answer is “I am now the first.” The correct answer is that if you overtake the one who is second, you take his place, and you are now second.

- The intuitive response most people give is 100 minutes. The correct answer is 5 minutes.

- The intuitive response is Rs 110 – Rs 100 = Rs 10. The correct answer is Rs 5.

So how did it go with our three questions?

Got all three correct? Great job!

Odds are, though, that your brain tried to force you to accept the intuitive but wrong (fast) answers first.

Based on what you experienced above, Psychologist and Nobel prize winner Dan Kahneman, in his path breaking book ‘Thinking Fast and Slow’, divides our decision making process into two modes of thinking:

- System 1 Thinking or Intuitive Thinking – which is instantaneous, fast, automatic, effortless and driven by instinct and prior learning

- System 2 Thinking or Rational Thinking – which is slow, more deliberative, logical, and requiring effort and energy

A good way to understand this – all of us speak our native languages using System 1 and tend to struggle to speak a new language using System 2!

Most of the time, System 1 (intuitive thinking), functions as a first filter and responds without having to include System 2, the rational part. This is very useful to automate a lot of our activities, but when we make important decisions, it can be dangerous to rely too heavily on System 1 thinking, instead of logically working through the information that’s available. No doubt, System 1 is critical to survival. It’s what makes you swerve to avoid a car accident.

But as Daniel Kahneman discovered, it can result in poor decision making, because our intuitions frequently mislead us given our inherent biases.

If you are someone who sets your watch timing ten minutes ahead of actual time, in order not to be late, you have unknowingly been using the power of System 1 (fast thinking). Though your System 2 (slow thinking) knows the truth, most often than not we stop with the intuitive and fast System 1 thinking.

Kahneman believes that fast and intuitive thinking (‘System 1 Thinking’) is safe if:

- The problem is simple

- You have seen a problem like this many times before and resolved it successfully

- The cost of being wrong is low and the consequences are acceptable

Kahneman believes that we can think more slowly (‘System 2 Thinking’), when:

- Problem is complex and the solution is not obvious

- You have not seen a problem like this before

- The cost of being wrong is high and the consequences are unacceptable

Now using the approach let us approach a recent event.

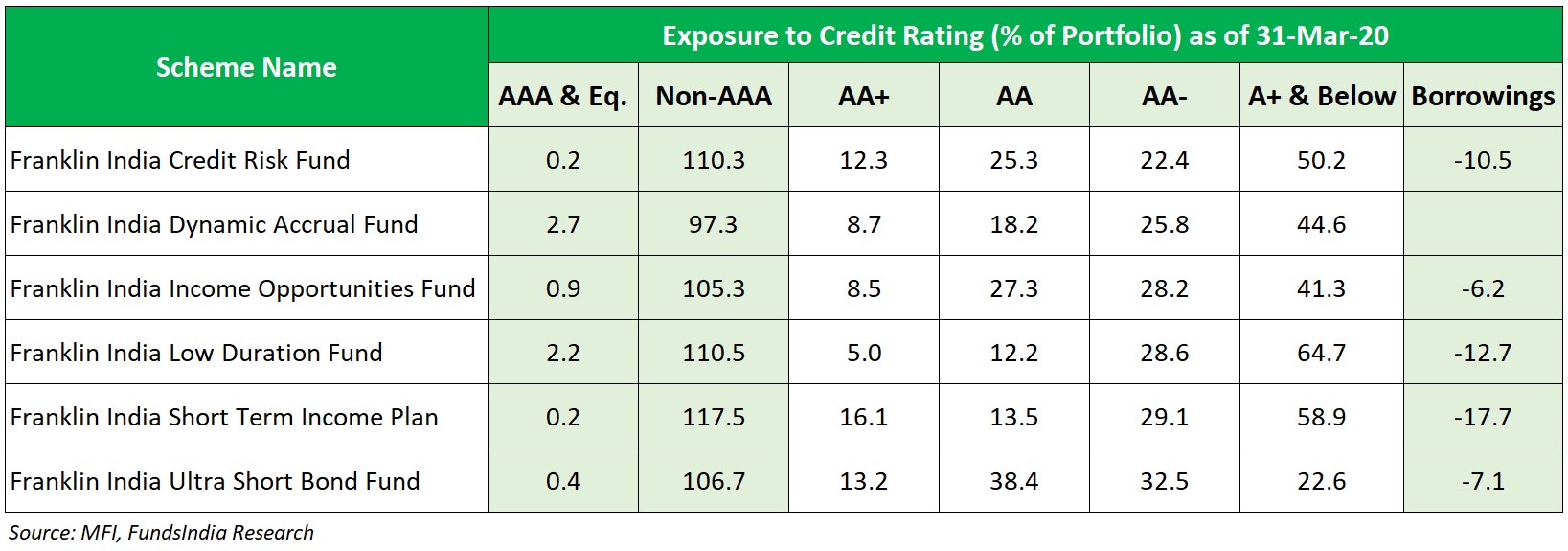

On 23-Apr-2020, Franklin Templeton Mutual Fund wound up its 6 credit risk oriented debt schemes.

Now the key question for us is:

How does this news influence our thinking with regards to our debt mutual funds?

Let us check what both System 1 and System 2 have to tell us..

Thinking Fast – The System 1 Approach

“Oops! Franklin Templeton closed 6 of its debt funds.

So all debt mutual funds must be risky. Let me move out immediately!”

This is a perfectly normal System 1 response. But given that the issue is complex, you have not seen a problem like this before and the cost of being wrong is high, we need to pause and start thinking slowly i.e use our System 2 approach.

Thinking Slow – The System 2 Approach

Why did Franklin Templeton close 6 credit risk oriented debt funds?

All these funds were running credit strategies – i.e a substantial portion of the funds were lent to lower credit rated corporates. But why?

Simple. These lower rated corporates pay higher interest rates to borrow from debt mutual funds versus higher rated corporates, which in turn means higher returns for investors. Sample this – all the 6 funds had YTM (read as aggregate of underlying interest rate paid by borrowers) of around 10-13% vs 5-7% in higher quality funds which predominantly lend to AAA rated corporates.

This was an explicitly stated strategy of the above funds and in technical terms is called as “Managed Credit” or “Credit Risk” strategies.

However these lower rated credit quality papers are usually not very liquid (read as they cannot be sold immediately in the market and will mostly have to be held till maturity). So as long as investors stay with the fund and the underlying papers don’t default on their interest and principal payments, these funds were doing fine.

In recent times, given the weak credit environment, such credit funds were facing significant redemption pressure from investors as most of them were moving to safer higher quality debt funds.

This led to a situation where the above mentioned credit risk oriented Franklin Templeton funds were not able to sell their underlying papers (due to the illiquid market conditions for lower credit papers) to meet redemptions.

If the fund did not close, then it would have been forced to sell its underlying illiquid papers at distress valuations to address the redemptions. This would have in turn led to significant NAV impact for existing investors in the fund.

Hence the fund house, in order to avoid distress selling and value erosion to existing investors has closed all the above funds and decided to return the money back to investors.

So the key reasons for closure of the 6 credit risk oriented debt funds are:

- Lower Credit Quality Exposure which is extremely illiquid

- Continuous and Significant redemptions in recent times

Summing it up,

Illiquid Portfolios + Significant Redemptions = BIG RISK!

Do all debt funds run illiquid portfolios?

As discussed earlier, lower rated papers usually have very low liquidity (read as cannot be sold immediately in the market) in Indian markets. During times of stress, the liquidity for such lower rated papers becomes even more tight as everyone becomes risk averse and wants to lend only to higher rated corporates.

On the contrary, higher rated papers (AAA & Equivalent) have very high liquidity.

In debt mutual funds, there are two categories of funds with respect to underlying credit quality

- Credit Risk oriented Funds (~5-10% of the total Debt Mutual Fund AUM)

- Non Credit Risk Funds or High Quality Funds (>90% of the total Debt Mutual Fund AUM)

Takeaway:

- All debt funds do not run illiquid portfolios. A large part (>90%) of the debt mutual fund is into safe, high quality funds (AAA oriented) and hence have high liquidity.

- Only Credit risk oriented funds which predominantly invest in illiquid lower rated papers have liquidity risk in case of significant and continuous redemptions.

Which debt funds should I be worried about?

All credit risk oriented funds face two risks at this juncture

- Credit risk – which is the possibility of underlying company defaulting and thus leading to NAV decline

- Liquidity Risk or Redemption Risk – which happens if there is continuous redemption from the fund

So if you have any credit risk oriented debt fund, let me reiterate to you before you panic, that it is not any debt mutual fund but specifically if you have CREDIT RISK oriented funds which are funds which predominantly invest in lower rated papers, then you must have a close watch on both the underlying portfolio quality and redemption trend.

This is a segment which remains very risky at this juncture and please get in touch with us if you have any credit risk oriented fund that you may have bought it on your own.

Now the good part is more than 90% of the Debt Mutual Fund Industry runs High Quality Oriented Strategies that have high liquidity.

Are my Funds India recommended debt funds safe?

All our recommended debt funds maintain

- High Credit Quality

- High Liquidity

High Credit Quality:

We have already sent a detailed note last week to you explaining the quality of the funds. But anyway let me give you the gist.

We have a total of 14 recommended funds –

Core Bucket – 10 funds out of which 8 funds have 100% AAA Exposure and 2 funds have >97.5% AAA exposure.

Alpha Bucket – 4 funds which have AAA exposure around 80-90% . The good part is even for our non AAA exposure, majority of the exposure is predominantly in Government backed companies, PSUs and Private Banks and large reputed groups such as HDFC, Tata, Aditya Birla, Hero, Bharti Airtel, Vedanta, TVS (Sundaram) etc.

So in terms of underlying credit quality we continue to stick with proven high quality funds with safe high quality portfolios.

High Liquidity:

The AAA segment is extremely liquid as there is always demand for good quality papers from the mutual funds, insurance industry, corporate treasuries, foreign investors etc.

This liquidity was further accentuated by recent RBI measures.

RBI to address the possible concerns of liquidity, has announced something called TLTRO (Targeted Long Term Repo Operations). While this might sound complicated, it is a simple arrangement where RBI initially went to the banks and said, “Hey I will give you folks Rs 1 lakh crs at the repo rate of 4.4% for 3 years. But you should use this money to lend to corporate bonds etc”. A lot of high rated corporates benefited from this such as RIL, HDFC, PFC, NTPC, National Board of Rural Development, L&T, Mahindra & Mahindra etc.

Post that another TLTRO of Rs 50,000 crs was announced to address the NBFCs. But given the low risk appetite of banks for anything other than high rated corporates, this saw a muted response.

On 27th of April, RBI announced Rs 50,000 cr special liquidity window – from which banks can tap money at the repo rate 4.4% to lend money for mutual fund redemptions or buy mutual fund papers. This money is reserved exclusively for Mutual Funds.

Also as on 04-May-2020, Banks currently have parked a whopping Rs 8.4 lakh crs with the RBI under the reverse repo window at a paltry 3.75% interest rate. This we believe at some point in time will be lent back to the higher rated corporates (given the attractive interest rate differential which the banks can earn) and can lower the yields substantially (providing return kicker based on the extent of modified duration of the fund).

So overall considering both RBI measures and the surplus money parked by banks with the RBI, we find the liquidity situation extremely comfortable for higher rated AAA corporates.

All of our recommended debt funds have high quality AAA oriented portfolios and thereby we are very comfortable on the liquidity front.

Summing it up..

Post the closure of 6 credit oriented debt funds by Franklin Templeton, there have been a lot of concerns surrounding debt mutual funds in general.

While a Systems 1 Thinking (Fast Thinking) would have led us to conclude that all debt funds are bad, going a little deeper using Systems 2 Thinking (Slow Thinking) shows us that only credit risk oriented funds facing high redemptions run similar liquidity risks.

Any debt mutual fund which runs a high quality portfolio (AAA oriented) has sufficient liquidity and hence we don’t need to worry about similar liquidity risks playing out.

All our recommended debt mutual funds maintain high credit quality and high liquidity.

We continue with our positive view on short duration high quality debt mutual funds.

Good explanation. Keep it up.