- A debt fund that will invest in corporate bonds

- Will invest over 80% in instruments with credit rating of AA+ and above

- High yield portfolio with moderate risk

- Has reduced its credit risk

Who

- Investors looking for FD-plus returns

- Willing to take moderate risk and hold for 3 years or more

These are times when debt mutual funds appear to be operating on the extremes – taking credit risks for higher returns or playing it very safe and compromising on returns. A fund that reduces credit risk at such times, without compromising too much on returns, therefore stands out.

We are talking of Franklin India Corporate Debt (earlier called Franklin India Income Builder), one of the few accrual funds with a 20-plus year track record. Post SEBI’s classification norms, this former credit-risk fund now dons a new avatar as a corporate bond fund, with significantly reduced credit risk compared with the last 5-6 years.

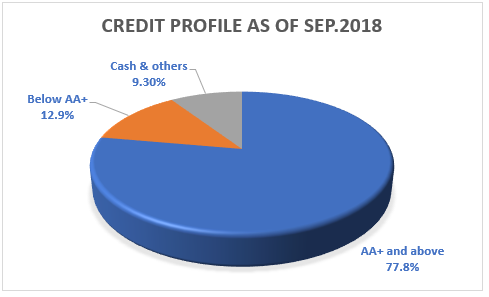

With a holding of less than 13% in instruments below AA+ (SEBI defines instruments below AA+ as having higher credit risk), the fund has an impressive 9.5% yield to maturity (YTM) on its current portfolio. This together with a relatively low expense ratio in the category (0.89%), makes this fund among the better picks in the corporate bond fund category.

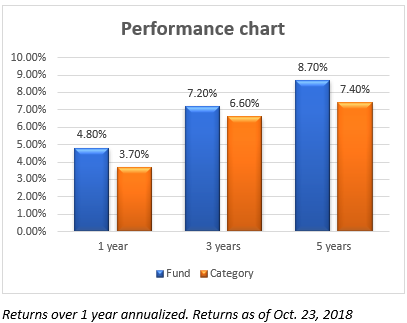

The fund delivered 8.7% annually in the past 5 years but that came with higher risks then. We have added this fund to our select list in the September-ended quarterly review.

The fund and suitability

Corporate bond funds are required to hold 80% or more in instruments with a credit rating of AA+ or more. That basically means that they must keep their risk profile low-to-moderate. They seek to earn returns through accrual (interest income) and any possible capital appreciation opportunities.

Franklin India Corporate Debt now adheres to this requirement and has about 55% in instruments with AAA/AAA(SO) rating, 23% in AA+/AA+(SO) and another 9% in cash. The fund’s reduced risk together with a long track record of generating steady accrual, makes it a good choice in the corporate bond category.

Having said that, funds such as HDFC Corporate Bond, although adhering to the same credit profile appear to come with marginally lower risks Franklin India Corporate Debt is suitable for marginally high-risk investors who want superior returns in the long term. While the fund has no exit load, this should not give any indication to investors to hold it for a short time frame. A minimum of 3 years is required to earn optimally and tax efficiently in this fund, considering its average maturity of 2.7 years.

Portfolio

From over 70% exposure to instruments below AA+ a year ago, Franklin India Corporate Debt has brought it down to 12.9% in September 2018. While it has been steadily reducing credit risk, the cut was more rapid after it classified itself as a corporate bond fund.

Its YTM, on the other hand, climbed from 8.7% to 9.5% in the past 1 year. The rising interest rate scenario has helped the fund catch the higher coupon rates even while reducing credit risks. The fund’s timing in terms of rejigging its portfolio has therefore worked in its favour.

The fund’s present YTM is higher than the corporate bond category average of 8.9%. It is also higher than stable funds such as HDFC Corporate Bond (8.9%). This pushed us into looking deeper into its portfolio to see where the higher yield was coming from. Instruments such as Sikkal Ports (Reliance Industries’ group), Piramal Capital & Housing Finance, all AAA rated were some of the high yielding papers. Barring this, the fund had exposure to stable companies such as REC, PFC and HDFC Bank, to name a few.

To us, the higher portfolio yield may come from mispriced opportunities but still suggest a notch higher risk despite high rating. It therefore calls for some risk-taking ability although not as much as credit risk funds.

Performance

Franklin India Corporate Debt has a good record of consistency, barring poor patches in 2016-17. This happened when one of the instruments it held across several schemes got downgraded and hit its NAVs. But the fund was then higher on credit risk, unlike now.

When returns are rolled on a 3-year basis, over the last 5 years, the fund has beaten its peer-average (including medium duration funds many of which had higher credit holding like the FT fund) 92% of the times. But this record is bettered by HDFC Corporate Bond fund. This was primarily because of the hit that Franklin India Corporate Debt took in 2016-17.

Franklin India Corporate Debt traditionally had a lower standard deviation and higher Sharpe (both being metrics for volatility and risk-adjusted return respectively) compared with the HDFC fund. However, it did not have high exposure to AAA earlier. With AAA-holdings now going up, higher volatility can be expected from here as this means holding more liquid/traded papers whose price gyrations will be higher.

The fund is managed by Santosh Kamath and has an AUM of Rs 811 crore.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis for investment decisions. To know how to read our weekly fund reviews, please click here.