At the current juncture, fixed income investors need to be prepared for relatively lower returns both from Bank Fixed Deposits and Debt funds compared to the returns they enjoyed in the last few years. You can read the detailed rationale behind our view here.

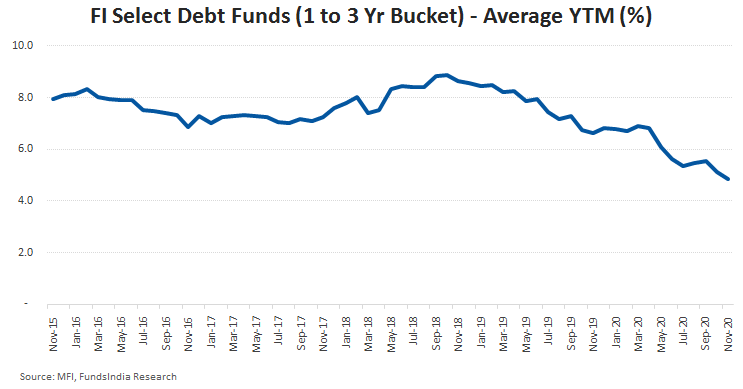

To put that in context, as seen above, the average yield to maturity (which roughly translates to the aggregate of interest rates paid by underlying companies of the debt fund) of our select debt funds from being above 8% a few years back has reduced to around 5% levels today.

Given the low yields in both Bank FDs and Debt funds, there is an inherent temptation to shift to slightly riskier ‘Debt-Oriented-Hybrid’ options (with some equity exposure) for improving returns.

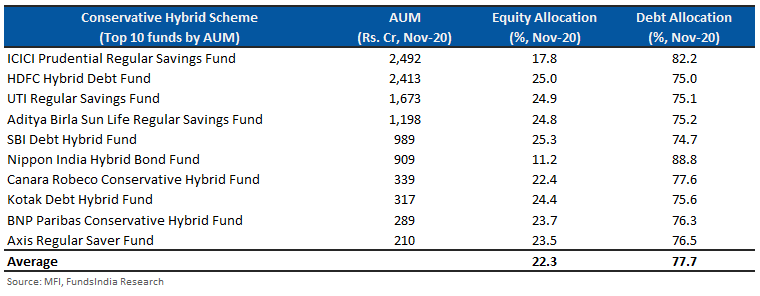

Under this context of wanting to improve fixed income returns, one particular ‘Debt-Oriented-Hybrid’ category that is starting to get attention is the Conservative Hybrid category of funds. These funds invest around 75% to 90% of their portfolio in debt instruments and the remaining in equities (i.e. 10% to 25% in equities).

The simple attempt is to improve returns via some exposure to equity.

Sounds like a reasonable choice, right?

But we have a slightly different view and would suggest you to be cautious while approaching this category.

Why do we find conservative hybrid funds to be not so conservative?

Stating the obvious, the equity portion of the conservative hybrid funds carries market risk and naturally, the overall returns may be more volatile than a plain vanilla debt fund.

This is perfectly fine with us as any investor who chooses this category for improving returns knows upfront about the 10-25% equity exposure and the volatility that it brings along with it.

Our real concern actually comes from four different sources:

- Credit Quality of the debt portion

- Higher Duration leading to interest rate risk in the debt portion

- High Expense Ratios

- Debt Taxation for the Equity portion

Concern 1: Most Conservative Hybrid Funds take some degree of credit risk to improve returns

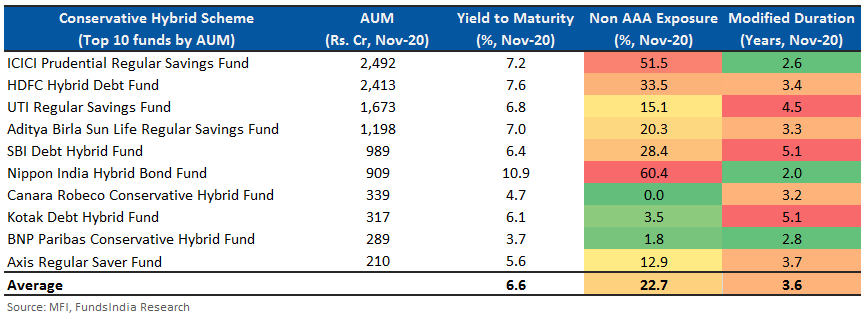

When we analyzed the debt portion (which amounts to more than three-fourth of the portfolio) of conservative hybrid funds, we found that most of the funds were taking credit risk to improve returns.

But hang on… what is credit risk?

There are certain debt funds which lend your money to lower rated corporates in return for higher yields (read as the interest rate paid by corporates for borrowing money from the fund i.e. indirectly from you).

As long as the underlying corporates fully service and repay their debts on time, these funds enjoy higher returns compared to higher credit quality debt funds (who lend predominantly to AAA rated corporates, financial institutions and government).

We have been avoiding such credit risk oriented funds, given the uncertain economic backdrop and the risk of redemption pressure (investors selling out of the fund).

As lower rated papers cannot be sold easily given the illiquid market for these securities, whenever there is a surge in redemptions from these funds, the fund manager is forced to sell other higher quality papers (which can be sold easily) in the portfolio. This usually leads to unintended higher concentration of lower quality papers in the fund significantly increasing the default and liquidity risks. The closure of 6 credit risk oriented funds of Franklin Templeton a few months back is a reminder of how liquidity risk can play out in the worst case scenario.

In our view, this makes credit risk oriented strategies extremely risky at this juncture.

Oops.. So what?

Conservative hybrid funds unfortunately invest a significant portion of their portfolio in the assets issued by lower rated borrowers in search for higher returns. Thus, this category tends to have higher credit risk and along with it the liquidity risk that follows.

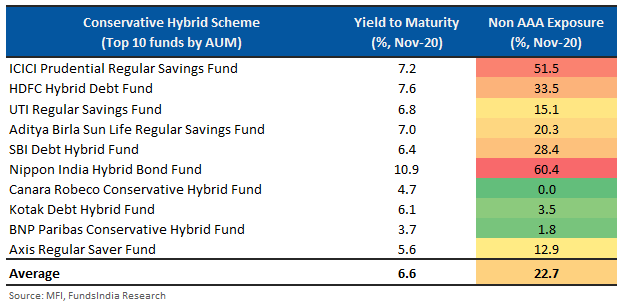

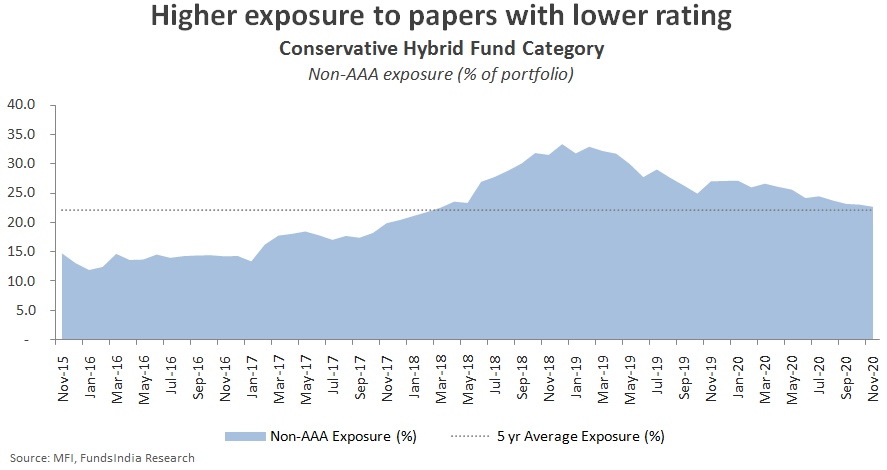

The conservative hybrid fund category (top 10 funds by AUM) holds an average exposure of around 23% in instruments with credit rating lower than AAA.

Over the past 5 years, the category has had consistently high exposure to non-AAA instruments at an average of 22% of the portfolio.

While this is not to say that all non-AAA exposures are risky and may default, this is a risk that you must be aware of. Most importantly liquidity risk (read as sudden redemptions) is our biggest concern when it comes to funds taking exposure to lower rated papers.

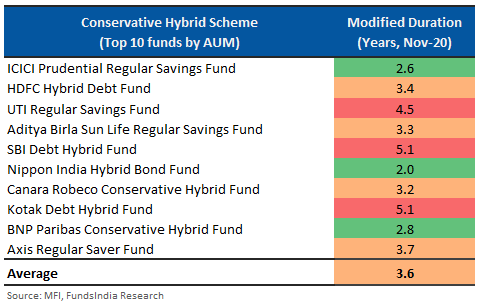

Concern 2: Several Conservative Hybrid Funds take higher duration in portfolios implying higher degree of downside if interest rates move up

In addition to credit risk, some of the conservative hybrid funds also tend to take interest rate risk. This risk arises due to the change in interest rates – increase in interest rates leads to price decline for the debt portion.

But hang on… What is Interest Rate Risk?

Let us explain this with a simple example.

Assume you have opened a Fixed Deposit for Rs 1 lakh at 6%, this will give you Rs 1,06,000 after 1 year. What if suddenly the bank increases its interest rate from 6% to 7% the next day?

This means, you got unlucky as you could have invested a lower amount – Rs 99,065 (vs the original Rs 1 lakh) to get the same 1,06,000 after a year.

What if instead, the bank reduces its interest rate from 6% to 5%?

In this case you got lucky as otherwise you should have invested more i.e. Rs 1,00,952 (vs the original 1 lakh) to get the same 1,06,000 after a year!

In the real world, FDs are not tradable. But hypothetically if you assume you could trade your FDs everyday, this implies the price of your FD will change if interest rates move up or down.

As seen above, if they move up, then your FD (already locked at lower interest rates) becomes less valuable and hence the trading price of your FD would come down to adjust for the new higher interest rates. Similarly, if interest rates move down, then your FD (already locked at higher interest rates) becomes more valuable and hence the trading price of your FD would go up to adjust for the lower interest rates.

This is exactly what happens in a debt fund which invests in bonds which are traded every day and the price of the underlying bonds fluctuates everyday based on change in bond yields.

If interest rates move up then your debt fund NAVs have a negative return impact and vice versa. However the extent of the same interest rate movement in your debt fund NAVs will depend on a parameter called modified duration.

Modified duration is measured in years and tells us what would be the expected increase or decrease in fund NAV for a 1% change in interest rates.

Change in fund NAV = (-1) * change in interest rates * modified duration

Assuming that a fund’s modified duration is 4 years and the yields rise by 0.5% then the fund’s NAV should drop by 2% (calculated with the above formula: (-1) * 0.5% * 4.

So higher the modified duration for a fund, higher the interest rate sensitivity.

Oops.. So what?

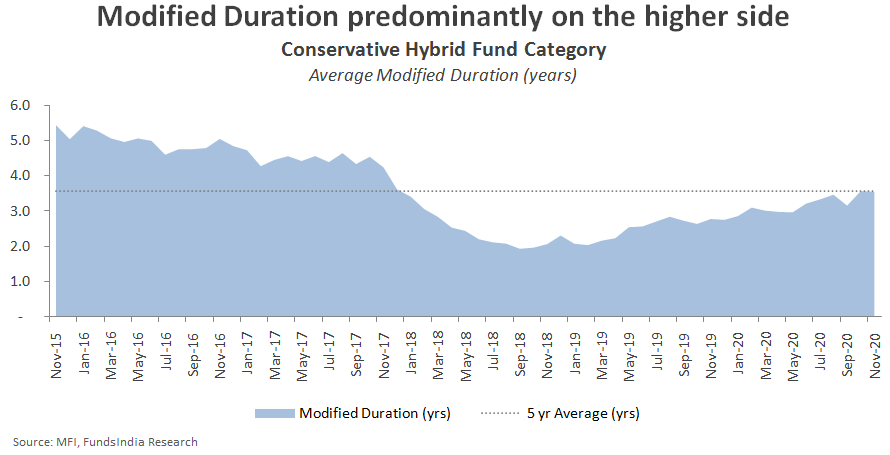

Modified Duration is on the higher side (> 3 years) for most funds in the conservative hybrid category with the average hovering around 3.6 years.

Even in the past 5 years, most of the funds in the category have run modified duration more than 3 years.

So overall when it comes to the debt portion most funds in this category have both

- Credit Risk via non-AAA exposure

- Interest Rate Risk via higher modified duration

While we have broadly warned you of the prevalent risks in the category, it is always better to evaluate on a case by case basis as there may be few exceptions.

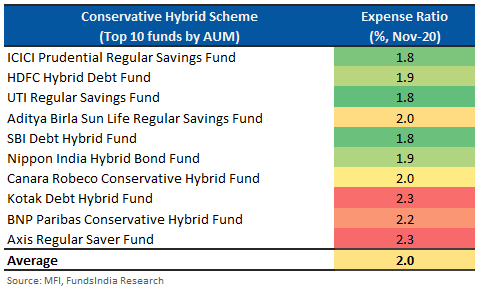

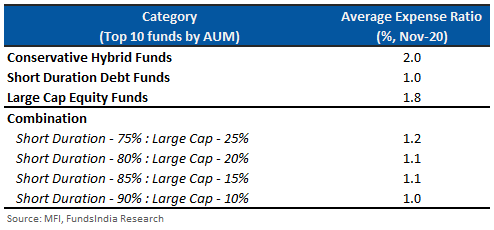

Concern 3: Expense Ratio is on the higher side…

Our other major concern is on the expense.

Conservative hybrid funds usually have high expense ratio for their regular plan – average expense ratio is ~2%.

To put this in perspective, the average expense ratio of the large cap equity fund category is 1.8% and the short duration debt fund category is around 1%. So if you decide to invest 25% into a large cap fund and 75% into a short duration debt fund, your expense ratio will work out to be around 1.2%.

Conservative hybrid funds thus work out to be a whopping 60-70% more expensive than a simple combination of 75% in a short duration debt fund and 25% in a large cap equity fund.

Concern 4: Equity portion (10-25% of portfolio) also gets ‘debt fund’ taxation

Conservative hybrid funds are taxed similar to debt funds. If you exit from a conservative hybrid fund within 3 years of investment, the gains realized will be treated as short term capital gains and they will get taxed per your income tax slab. This could imply higher taxation impact on the equity component, which would have otherwise enjoyed equity taxation if taken exposure directly.

So, are there any alternate options?

Option 1: Equity Savings Funds

The equity savings fund category is also pretty similar to Conservative Hybrid category and has around 20-40% exposure to equities, with remaining in debt and arbitrage. In addition, equity savings funds come with the equity taxation advantage.

This is a category where most funds run high credit quality portfolios (predominantly AAA & Equivalent) and have low modified duration thereby low interest rate risk.

The only hitch is the expense ratio. While most of the funds in this category have the same problem of higher expense ratios as the conservative hybrid category, a few options thankfully are available at relatively lower expense ratios.

Option 2: Building a Conservative Hybrid portfolio manually

Instead of going for any particular category, you can manually construct the ‘conservative hybrid’ allocation by investing, let’s say, 75% of your money in a high credit quality shorter duration debt fund and the remaining 25% in a proven large cap equity fund.

Summing it up

- We find conservative hybrid fund category not so conservative, as most of the funds

– Take credit risk to improve returns

– Run high modified duration (> 3 years) which can impact returns if interest rates move up

– High Expense Ratio of ~2%

– Taxation disadvantage for equity component

- This is also reflected in our lower rating for funds from the conservative hybrid category

- Alternate options:

– Equity Savings Fund (but look out for the expenses)

– Manually construct a 75% Debt + 25% Equity Portfolio

Wake-up call for most of us choosing funds based solely on advertised gains!