The BJP’s win in the UP elections provided a leg up to the market for couple of reasons: one, it reposed the faith in the policy reforms of the government and brushed aside concerns of demonetisation even if it lasts for some time. Two, while too early, it sets the stage for the 2019 elections and provides comfort, especially to institutional investors, in terms of long-term policies getting implemented at the Central level.

The markets, on Tuesday, gave a firm thumbs-up to the election outcome, pushing the Nifty above the crucial 9000 mark. This is not the first time that markets have touched 9000. Leaving out September 2016 (which just went by and a meaningful comparison is not possible), the last time the Nifty touched 9000 was 2 years ago, in March 2015. It could not retain the level though. But quite a few things have changed since then:

- The banking space was just beginning to wash its dirty linen in terms of opening its bad loan (NPA) story to the market in 2015

- It was the beginning of several earnings downgrades as the post-election rally could not really sustain on the back of poor earnings by companies

- Inflation was much higher than what it is today

- Commodity prices sagged then. While that provided relief for input users, it caused high debt and losses in core sectors. Commodity prices are firmer now and related industries that were in heavy debt and losses are slowly turning around

- And above all, there has since been a steady and meaningful uptick in the domestic institutional activity (DIIs – typically insurance companies and mutual fund companies) in the market since then

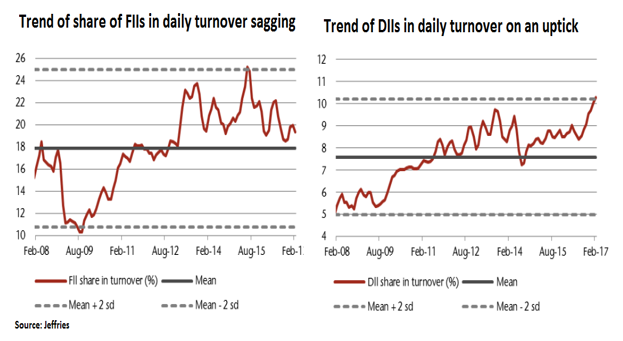

Take the last point mentioned above. While FIIs have remained the largest holders and drivers of stock markets in India, DIIs could slowly take the lead in setting market prices. Evidence to this is appearing in the trading activity of DIIs compared with FIIs. Look at the charts below:

- By mid-2015 DIIs hit new peaks in terms of ownership of stocks albeit still lower than FIIs. But more importantly, DIIs’ proportion of trading activity to their holding is catching up with FIIs (see first chart above)

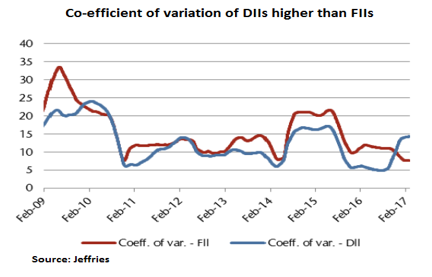

- To confirm this trend, the variability of net flows is also on an uptick. Reported data by research houses suggests that co-efficient of variation of net inflows (which is nothing but the ratio of standard deviation to the mean) of DIIs has surpassed that of FIIs (second chart above)

- This is an important indicator that there is steady uptick in money that DIIs are pumping daily into the market

- And this uptick has been steady because of steady inflows from local institutional investors such as insurance companies and mutual funds.

- In fact, from October 2016 till February 2017, FIIs were net sellers in equities every month other than February. There was a net outflow of Rs 22,000 crore in equities over this period. And yet, the Nifty stood firm, with a positive return of 3.4% over those 5 months. This could not have been possible without domestic support, as DIIs brought net inflows in each of those months with a total of about Rs 41,000 crore over the same period. This goes to show the steady uptick in DII flow.

It is this pumping of money that seems to keep the market going strong despite major news such as Brexit or US elections or Federal Reserve rate hikes. And it is this strength that appears to be keeping the markets afloat despite valuations not being particularly cheap. That does not mean that valuations will be ignored. Just that markets may react less to short-term fears if long-term money finds reason to stay in the markets. And DII money is relatively more long term than FII money.

It is in this context that local news such as UP elections are a big deal in terms of providing comfort to local investors (DIIs).

What to expect?

- As investors, do not give much importance to the current short-term rally. Do not be swayed by the abnormal returns reflected in your portfolios and keep your expectations reasonable based on your time frame

- At the same time, do not fear a bubble as we think a 9000 Nifty, will be different this time compared with March 2015. So, do not wait for any large correction to enter the market

- Expect intermediate corrections, be it in from Fed Rate hike or earnings-driven disappointments, GST-related hiccups or interest rate signals from the RBI. Use such corrections to buy further on dips if the correction is in the range of 3-5% over a month’s time

- Valuations at 23 times trailing Nifty (as of March 10) is not cheap. That means upside from here at least for 2017 will not be much.

- At the same time, the market momentum is being slowly built and being kept afloat by DII inflow surge. This is not short-term money. If this trend continues, expect a long-term uptrend, to be necessarily supported, of course, by corporate earnings growth as well as government reforms gathering momentum; as we take a break from election distractions

The best way to therefore play the market would be to go with the DII flow. That means staying invested and continuing to invest using the SIP/STP route. Stay cautious of high return estimates but do not exit, fearing the market. Keeping away from the market costs more than staying at highs, as long as you are averaging.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis of investment decisions. To know how to read our weekly fund reviews, please click here.