The stock markets hit record highs on global political cues and post a special report by Federal Reserve on the positive impact of GST on India’s GDP. But elsewhere, the banking regulator, the RBI, has been quietly tightening the screws on banks. And this, we believe is a more important event for the markets.

Last week saw a couple of important notifications from the RBI that may have a near to medium-term impact on the markets. The crux of those notifications are as follows:

- The RBI advised banks to make higher provisions (than the current 0.4% regulatory minimum) to assets that have not gone bad but are in stressed sectors. Banks must have a board-approved policy for such provisioning.

- The RBI indicated that telecom could be one such stressed sector at present and asked banks to review their loan books to this sector by June 30, 2017 and make higher provisions where needed.

- In another notification, the RBI said that where the additional provisioning requirements identified by them for each bank is higher than 15% of what the bank publishes, then the divergence must be disclosed in the annual report.

Why the above norms

There are a few reasons why RBI is doing what it is doing. For one, over the last few years, banks have been on and off disclosing the skeletons in their closet – that is loans that have gone bad and could not be recovered. This story has not seen the end of day, thus preventing banks from getting into full-fledged lending mode again. The RBI, by asking banks to assess stressed sectors (even if they are servicing their debt), is simply asking banks to take the cautious route and manage loan books and profitability in a less volatile manner. Two, where it is felt that banks are not fair in their disclosure, the RBI is forcing them to disclose an independent view (the RBI’s audit of their loan book) on how much provisioning is really needed and what was provided. Both are steps towards ensuring banks clean up their books as and when warranted, do not take in sudden shocks and provide a true and fair view of their financial position.

What this will do

From a big picture perspective, this will distinguish the better managed banks from those that run risks to earn profits. From a bank’s perspective, higher provisions that banks hadn’t done for normal assets may now have to be done. This means that in the medium-term, banks may take a hit in the margin. However, in the long term, the banking space may be professionally run and see less shocks even when various sectors go through cycles. It may also have a more normalised growth as opposed to the volatile growth they witness now.

What’s the scene today

While it is very early to comment on which banks will be forced to provide more in sectors such as telecom and other stressed sectors, there are some research reports on the quantum of exposure to these sectors. Data below is sourced from the respective research reports mentioned:

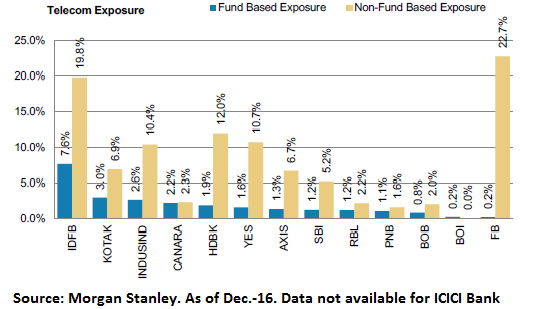

Exposure of banks to the telecom sector is at Rs 82,000 crore or 1.2% of their loans. This is not too high if you consider the below-mentioned stressed sectors. Their exposure can be split into fund-based and non-fund based exposure (shown above). Fund-based exposure are loans and other direct forms of credit given to a company while non-fund based exposure is typically in the form of letter of credit, bank guarantees and so on. Both can be a source of risk to banks, if the telecom company is unable to service its obligations on time.

While there could be some provisioning made by banks in the telecom space (given RBI’s current emphasis on this), we believe it is the other stressed sectors that will start coming into the quarterly radar of the boards of each bank, as required by RBI.

What’s with mutual funds

The telecom sector, together with the equipment space accounts for less than 1.2% of equity mutual funds’ exposure. Hence, it is not a large exposure and stocks in the space have seen some turbulence already, post Jio entry. However, debt funds do hold many AAA rated instruments in this space. For now, there does not seem any concern, although we will be keeping a close watch on instruments held by the debt category.

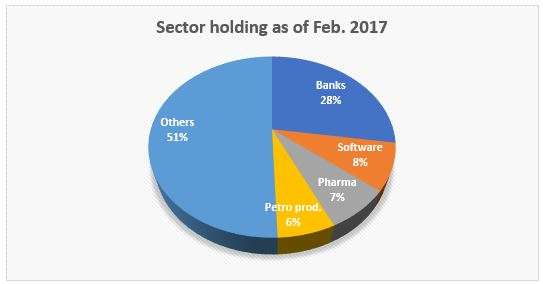

The bigger story and the bigger opportunity lies with exposure of equity mutual funds to banks. With banking and financial services accounting for about a third of the bellwether index Nifty 50, mutual funds are not far behind with their exposure of 28.3% (as of March 2017) in this segment. That means as and when banking stocks see turbulence from provisioning norms, the market too (and consequentially mutual funds) will see a jerk. We think such events will be opportunities for you to buy and average better.

The long-term story

Remember, the RBI norms do not in any way mean the end of banks. They simply mean banks must go through a clean-up phase and a more stringent ‘vigilance’ mode. Even as this clean up happens, there is more positive news in the economy in the form of GST and its benefits, as well as other reforms.

Let’s take the GST: a recent Federal reserve paper states thus – ‘The first (assumption) gives an aggregate weighted GST of 16 percent with a positive impact on real GDP of 4.2 percent, whereas our second allocation gives an aggregate weighted GST rate of 20 percent with a lesser positive impact on a GDP of 3.1 percent.

Now, the above number is not small in any sense of the term, as it amounts to Rs 6.5 lakh crore (stated to be higher than the government’s borrowing) and is underpinned by manufacturing output. A local-estimate (by NCAER) had placed this number at 1-2% of the GDP.

Now, take a step back and look at the not-so-cheap valuations especially in certain sectors – auto and auto components, cement, certain industrials and consumer durables – to name a few and more recently energy, logistics and transport. The market’s willingness to pay high multiples (valuations) in a sustained manner can only point to one thing – that it hopes reforms will pay off, even if it takes time. And remember, these multiples may be justified even if the return on equity of many of the companies (that have fallen since 2008), move up a bit. Interestingly, many of these sectors are a play on commodities as well as consumer spending. To this extent, they can offer double benefits, when there are tailwinds on both these fronts.

What to do

We believe that the headwinds in the market in the form of bank earnings should be viewed as opportunities to average. Fund managers will take a call on which banking stock to hold and which ones to prune. As investors, we think your job will be to capitalise on the turbulence. Systematic transfer plans or better still, value averaging plans (or value averaging transfer plans) will be the way to go for the next 6-9 months at least to make the best of such turbulences.

If you wish to know how to go about setting up these or which funds to invest in, talk to our advisors to understand which of the funds you currently hold will be better suited to invest in further now. If you are a moderate-risk investor, avoid taking direct exposure to banking sector funds afresh. Any averaging already being done may be continued with a long-term time frame.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis of investment decisions. To know how to read our weekly fund reviews, please click here.

Very nice article. Crisp, timely (FY 17 result season has just started ) and thought provoking.

Very nice article. Crisp, timely (FY 17 result season has just started ) and thought provoking.

Thank you so much, For the information, that’s really gonna help me alot

Thank you so much, For the information, that’s really gonna help me alot