In the last few weeks, you would have suddenly noticed that some of your debt mutual funds have given slight negative returns. The extent of negative returns would be different based on the category of funds you are invested in.

Nevertheless, there is a good chance that you are beginning to worry as to what is happening.

Now before you jump the gun and take some hasty decisions, let me try and help you make sense of what is happening. Once you understand the reasons, you can make an informed decision.

Back to Basics – What Goes Behind Debt Fund Returns?

Let me start with the basics:

When you invest in any debt mutual fund, in essence, you are actually ‘lending’ your money just like a bank, moneylender, etc. Now because you have a day job, and have no intention to analyze whom to lend and how to retrieve the money back (if in case the borrower plays smart), you want someone who can do it on your behalf.

This is where debt funds enter the picture. They collect money from several investors (read as indirect lenders) like you and lend it on your behalf. They do all the required analysis, due diligence etc and lend to a mix of

- Corporate companies (jargon used: Corporate Papers, Corporate Bonds etc)

- Government (jargon used: Gilt, Treasury Bills etc )

- Financial Institutions (jargon used: Certificate of Deposits)

Say you lend your money to your friend. What is the first question you ask?

Obvious right – What is the interest rate that you will pay me?

This simple question’s answer in the debt fund world is called the YTM (Yield to Maturity). Before you freak out, it is simply the aggregate interest rate of all the borrowers to whom the debt fund has lent your money.

Now typically this should be the approximate return expectation from your fund.

But wait!

Debt Mutual funds don’t do this intermediation for free and charge us a small cost called expense ratio for going through the hassles of evaluating borrowers, lending, and collecting money from them.

So we need to adjust for this expense ratio.

Your return for the next 1 year will be approximately equal to YTM adjusted for this expense ratio. Let us call this Net YTM.

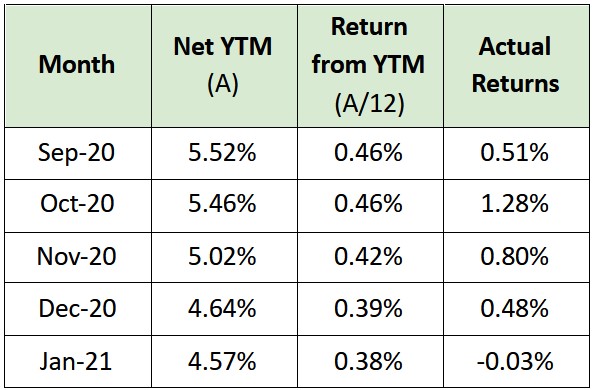

Say let us take an example of HDFC Short Term Fund.

YTM = 5.48%

Expense Ratio = 0.78%

Net YTM = YTM – Expense Ratio = 5.48% – 0.78% = 4.7%

Cool! So we should be expecting around 4.7% from HDFC Short Term Fund over the next 1 year.

Let us simplify this further using 5th standard mathematics.

If our return expectation is Net YTM over the next 12 months – the return expectation over 1 month should be roughly Net YTM / 12.

Let us check if this held true in the last few months.

Oops! There seems to be a significant difference in certain months. How do we explain this?

This is where we need to understand the second component of debt fund returns – Returns due to change in interest rates.

Before you switch off, let me simplify this for you.

Assume you have opened a Fixed Deposit for Rs 1 lakh at 6%, this will give you Rs 1,06,000 after 1 year.

What if suddenly the bank increases its interest rate from 6% to 7% the next day?

This means you got unlucky as could have invested a lower amount Rs 99,065 (vs the original Rs 1 lakh) to get the same 1,06,000 after a year.

What if instead, the bank reduces its interest rate from 6% to 5%?

In this case, you got lucky as otherwise, you should have invested more i.e Rs 1,00,952 (vs the original 1 lakh) to get the same 1,06,000 after a year!

In the real world, FDs are not tradable. But hypothetically if you assume you could trade your FDs every day, this implies the price of your FD will change if interest rates move up or down.

As seen above, if interest rates move up, then your FD (already locked at lower interest rates) becomes less valuable and hence the trading price of your FD would come down to adjust for the new higher interest rates. Similarly, if interest rates move down, then your FD (already locked at higher interest rates) becomes more valuable and hence the trading price of your FD would go up to adjust for the lower interest rates.

This is exactly what happens in a debt fund that invests in bonds that are traded every day and the price of the underlying bonds fluctuates every day based on the change in bond yields.

If interest rates move up then your debt fund returns will go down and vice versa. The degree of impact of the same interest rate movement on your debt fund returns will depend on a parameter called modified duration.

Modified duration is measured in years and tells us what would be the expected increase or decrease in fund NAV for a 1% change in interest rates.

Change in fund NAV = (-1) X change in interest rates X modified duration

Assuming that a fund’s modified duration is 2 years and the yields rise by 0.5% then the fund’s NAV should drop by 1% (calculated with the above formula: (-1) x 0.5% x 2).

Higher the modified duration for a fund, the higher the interest rate sensitivity.

So this implies that there are two components to your returns

- 1st Component: Net YTM

- 2nd component: (-1) x Modified Duration x Change in Interest Rates

Approximate Debt Fund Returns = Net YTM + (-1) x Modified Duration x Change in Interest Rates

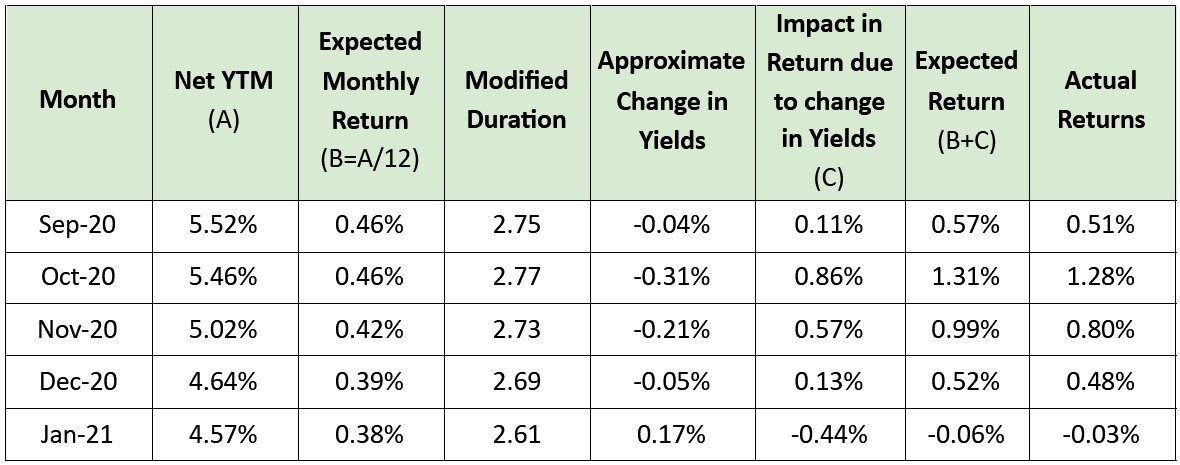

Now let us go back to our original example

In Jan-21,

HDFC Short Term Fund had a starting Net YTM of 4.57

Interest rates increased during the month by roughly 17 bps

Modified Duration was roughly around 2.61 years

1st Component: Net YTM/12 = 4.57/12 = 0.38%

2nd component: (-1) x Modified Duration x Change in Interest Rates = -1 x 0.17% * 2.61 = -0.44%

Return Expectation for Jan-21 = Net YTM/12 + (-1) x Modified Duration x Change in Interest Rates = 0.38% – 0.44% = -0.06%

Actual Return = -0.03%

Ah! There you go. If not for the yields going up, you would have received around 0.38% returns. The yields going up led to a decline of ~0.44%. Adding both these components we ended up with flat returns for Jan-21.

Let us check the previous table now,

Now you understand what goes behind the returns from a practical point of view.

Two Key Drivers of Debt Fund Returns

Now, we know that

- Debt fund returns should be anchored to Net YTMs and not past returns

- If interest rates go up, the returns will be lower and vice versa

- The extent of impact due to interest rate changes depends on the modified duration of the fund – the higher the modified duration higher the impact on NAVs

If interest rates go down, we will end up with higher returns and everyone is happy.

But if interest rates go up, returns come down sharply in the near term especially for funds with higher modified duration. This is the context that we must be aware of.

Interest rates as seen from history move through cycles i.e they have periods where they go up followed by a period where they come down and this keeps repeating. While the duration and magnitude of these cycles are difficult to predict, we need to have an approximate view of where we are in the interest rate cycle to make sure that our debt fund portfolios are appropriately positioned.

- When interest rates are expected to come down, it makes sense to go for funds with slightly higher modified duration

- When interest rates are expected to go up, it makes sense to go for funds with a low modified duration.

So here comes the million-dollar question

Right now, where are we in the interest rate cycle?

In our view, the ‘declining yields’ phase is behind us and we must prepare for a rising yield environment going forward.

What this means for us is that funds with higher modified duration (which also had great returns in the past when yields were falling) may exhibit higher volatility (read as negative returns) in the short run. The returns from these funds may be back-ended and will require longer investment time frames.

Here is our detailed rationale:

FundsIndia Debt Market View

- We are in a ‘rising yield’ environment and we expect yields to gradually inch up over the next year albeit in a gradual & not-so-sudden manner

- The rate cut cycle is behind us (read as the period of excess returns from debt funds) and you will have to prepare for relatively higher volatility in your debt fund portfolios over the next 1 year

- The extent of volatility will be dependent on the modified duration profile of your funds. Higher the modified duration, the higher the volatility to be expected

- Debt mutual fund portfolios must be positioned for the rising yields environment

Why do we think you must prepare for a ‘rising yield’ environment over the coming quarters?

- Higher-Than-Expected Government Borrowing

- Announced in the recent budget – led by higher Fiscal Deficit – 9.5% of GDP in FY21 and 6.8% of GDP in FY22

- Gross Market Borrowing for FY22 at Rs 12 lakh crs – To put this in perspective, FY21 gross market borrowing estimate of the centre government before the pandemic was ~Rs 7.8 lakh crs

- Rs 80,000 cr additional borrowing for FY 21

- Given the extended fiscal glide path government’s market borrowing is likely to remain elevated for longer period

- Higher expected borrowing from State Governments

- Pause in Rate Cuts

- Gradual Normalization of Liquidity measures undertaken by RBI during the Covid Crisis

- Possible Inflation Pressures due to Economic Recovery and Commodity Price increase (especially crude)

- Bond Yields near decadal lows

- Global Yields inching up in recent times

Why do we expect the rise in yields to be gradual and non-disruptive?

- In the monetary policy statement on Feb 05, the RBI reiterated its commitment to support the bond market and promised an ‘orderly completion of the government’s market borrowing program in a non-disruptive manner’

- A sudden sharp increase in interest rates will

- increase the cost for the government’s large upcoming borrowing program

- impact the economic recovery

- RBI will want to avoid this scenario and will attempt to keep the yields in a narrow range

- We expect RBI to continue using OMOs and other tools (at least in this calendar year) to ensure that yields do not suddenly move up sharply

- Our view is that yields are expected to gradually inch up but in a gradual and non-disruptive manner

How do you position your debt portfolios for a rising yield environment?

Going forward, we prefer funds with lower modified duration (1 year or less) as these funds are well suited for a rising yield environment. They exhibit much lower volatility when yields increase and quickly reset to the higher yields thus improving future return potential.

With the broad objective of striking a reasonable balance between near-term volatility and long-term portfolio returns, here is our debt fund portfolio construction approach.