SRF Ltd. – Diversified Chemical Player

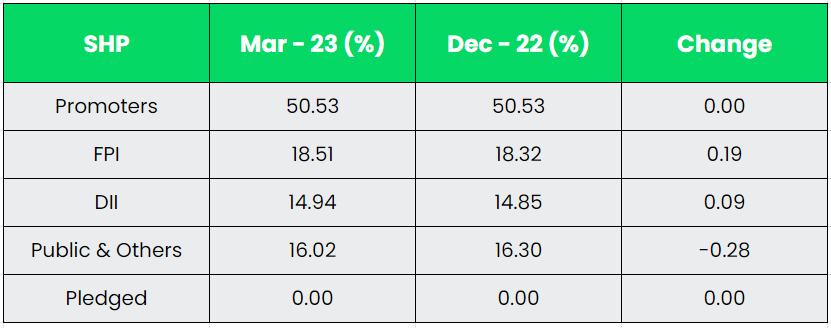

SRF Limited is a chemical-based multi-business entity engaged in the manufacturing of industrial and specialty intermediates. The Company is a market leader in most of its business segments in India and also commands a significant global presence in some of its businesses, with operations in three other countries namely, Thailand, South Africa and Hungary. The Company has commercial interests in more than ninety countries and classifies its main businesses as Chemicals Business (CB), Packaging Films Business (PFB), Technical Textiles Business (TTB), and Other Businesses. The parent company Kama Holdings Ltd. holds 51% stake while the other 49% is held by the DII, FII and public. The company has 10 manufacturing facilities in Tamilnadu, Rajasthan, Gujarat, Uttarkhand, Madhya Pradesh, Hungary, Thailand and South Africa.

Products & Services:

The company offers a diverse range of products majorly in three segments.

- Chemical Business – The Chemicals business includes two segments, namely Specialty Chemicals and Fluorochemicals. It includes products like Active, Non-Active Intermediaries, Ozone friendly refrigerants, Pharma propellants, etc.

- Packaging Films Business – Product mix includes transparent, metalized, coated, and other value-added films finding diverse applications in fast moving consumer goods, food & agro, confectionery, soaps & detergents, solar panels, labelling, overwraps, embossing, etc.

- Technical Textiles Business – Product basket for technical textiles includes tyre cord fabrics, belting fabrics and industrial yarn and is used in varied applications, such as tyres, seatbelts, conveyor-belts and other industrial applications.

Subsidiaries: As on FY23, the company has a total of 8 Subsidiaries and 2 Associate companies.

Key Rationale:

- Established Position – SRF is well diversified within its product mix, manufacturing, infrastructure and end-user industries. The company’s diverse product mix enables it to cater to diverse end-use industries including automobile, pharmaceuticals, air conditioning and refrigeration, food and agro, chemicals, mining, among others. The product and segment diversification provide some safeguard from slowdown in one segment, which is reflected in the company’s historical performance. SRF has been strategically making higher investments in Chemical Business, which has the highest margin among others coupled with high entry barriers.

- Expansion – SRF has guided for ~Rs.2500 crore of capex in FY24 and Rs.15,000 crore over FY24-28. The majority of the capex (Rs.2200-2300 crore for FY24; Rs.12000-13000 crore for FY24-28) is allocated to the chemical business as the company plans to enter fluoropolymers and other refrigerants. SRF plans to commission seven specialty chemical plants and three Fluorochemicals plants in FY24. In the Fluorochemicals business (~36% of chemical segment revenue in FY23), HFC (hydrofluorocarbon) is expected to remain the key product for the next 3-4 years. However, HFO (Hydrofluoroolefins) is likely to play a major role thereafter, thanks to its zero ozone depletion potential and low global warming potential (GWP). SRF’s upcoming R32 plant (HFC variant with lower GWP) with capacity of ~15,000 MTPA (at capex of ~Rs.550 crore) is likely to be commissioned in Aug’23.

- Q4FY23 – The consolidated revenue of the company grew 6% from Rs.3,549 crore to Rs.3,778 crore in Q4FY23 when compared with Q4FY22. The company’s EBITDA decreased 2% YoY from Rs.948 crore to Rs.932 crore in Q4FY23 and the margin decreased by ~210 bps YoY to 25%. The company’s Profit after Tax (PAT) decreased 7% YoY from Rs.606 crore to Rs.562 crore in Q4FY23. Segment wise, Chemicals segemnt reported a 34% YoY growth, followed by Packaging Films Business with a decline of 17%, Technical Textiles business with a decline of 13% and others with a flat growth of 1%. Chemical segment contributes around 88% to the overall EBIT in Q4FY23 followed by Packaging with 4.9%, Technical textile with 5.8% and others with 1.3%.

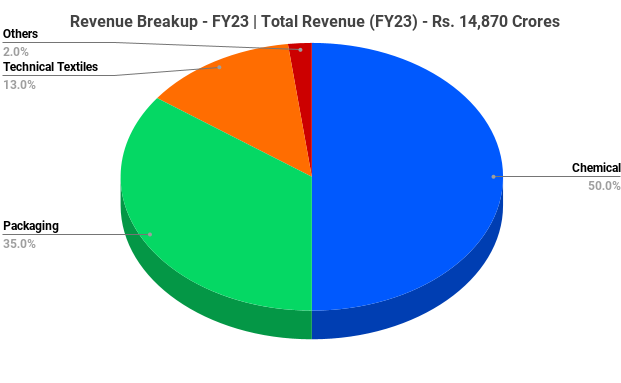

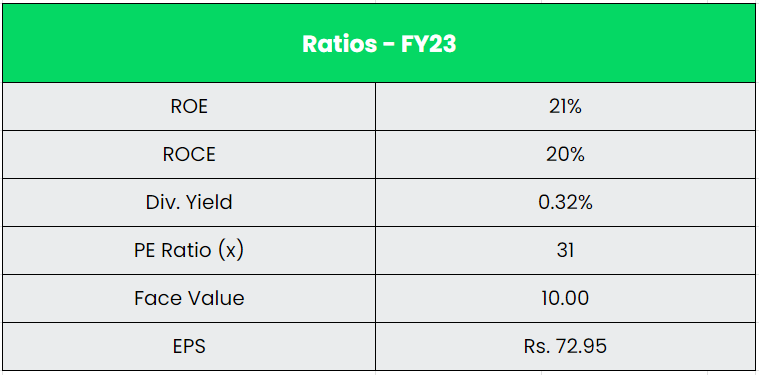

- Financial Performance – The company’s revenue has multiplied nearly 3 times in a span of 5 years, surging from Rs.5589 crore in FY18 to Rs.14,870 crore in FY23, reflecting a remarkable CAGR of 36%. Simultaneously, the EBITDA has surged from Rs.906 crore in FY18 to Rs.3529 crore in FY23, maintaining a robust CAGR of 32% during the same period. Specialty chemical business has been the key growth driver for the company, with a ~49% revenue CAGR over FY18-23. It accounts for ~56% of chemical segment revenue in FY23, up from ~35% in FY18. Cashflow generation is the main positive of the company with the Operating cashflow nearly jumped 5 times from Rs.678 crore in FY18 to Rs.2902 crore in FY23, reflecting a CAGR of 34%.

Industry:

Covering more than 80,000 commercial products, India’s chemical industry is extremely diversified and can be broadly classified into bulk chemicals, specialty chemicals, agrochemicals, petrochemicals, polymers, and fertilisers. The production of Total Major Chemicals and Petrochemicals in 2022-23 (up to September 2022) is 26570 thousand MT. CAGR in the production of Total Chemicals and Petrochemicals during the period 2017-18 to 2021-22 is 4.61%. India ranks 11th in the World Exports of Chemicals (excluding pharmaceutical products) and ranks 6th in the World Imports of Chemicals (excluding pharmaceutical products). The production of Major Chemicals in 2022-23 (up to September 2022) is 6487 thousand MT. The combined exports of Major Chemicals and Major Petrochemicals in the year 2022-23 (up to September 2022) is $ 9 Bn, an increase of 2% from last year’s export value, Imports have increased to $ 13.33 Bn.

Growth Drivers:

- Shift in production and consumption towards Asian and Southeast Asian countries in all sectors leading to increasing demand for Chemicals and Petrochemicals.

- 100% FDI is allowed under the automatic route in the chemicals sector with few exceptions that include hazardous chemicals. Total FDI inflow in the chemicals (other than fertilisers) sector reached US$ 21.3 billion between April 2000 and March 2023.

- India’s large agricultural sector creates demand for fertilizers, pesticides, and other agrochemicals, supporting growth in the chemical industry.

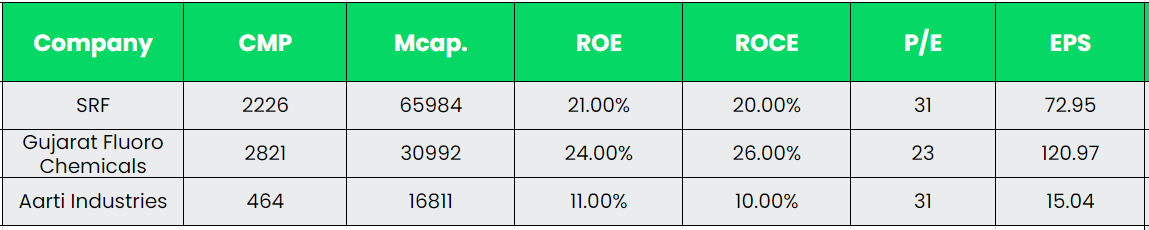

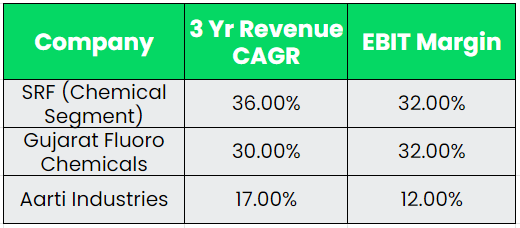

Competitors: Aarti Industries, Gujarat Fluorochemicals, etc.

Peer Analysis:

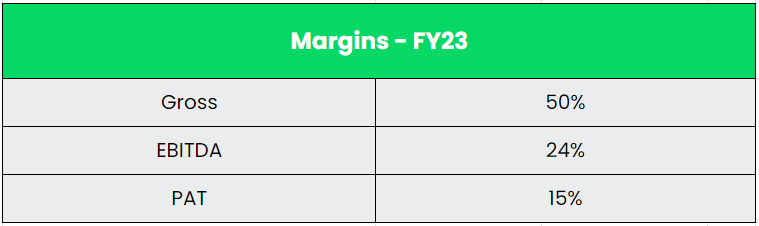

SRF is a diversified player operating in segments other than chemicals and it is tough to compare it with other players. When comparing the chemical segment of the SRF with the peers, it is evident that SRF shines in every aspect of the fundamentals.

Outlook:

SRF anticipates a high growth rate of over 20% in FY24 in the chemical segment. This growth will be fueled by the commercialization of seven new specialty chemical plants, the expansion of their product portfolio, and the fortification of their customer base. The Agrochemical and Pharmaceutical segments remain at the forefront of their focus, and they plan to collaborate with major global innovators to develop, commercialize, and produce complex new age molecules. In the pharmaceutical business, SRF aims to enter the CDMO sector, either through organic growth or strategic acquisitions. The Packaging Films segment has seen significant progress, with debottlenecking at the South Africa plant boosting capacity by approximately 3500 tonnes per month. The upcoming commissioning of the aluminium foil plant in Q2FY24 will further solidify their position as a solution provider in the BOPP (biaxially oriented polypropylene films), BOPET (biaxially oriented polyethylene terephthalate), and aluminium foil markets. Notably, a revival in demand for NTCF and belting fabric is being observed in the Technical Textile segment, while the polyester industrial yarn is expected to thrive with applications in geo-textiles and seatbelts. With these ambitious endeavours across multiple segments, SRF is well-poised for a successful and transformative future.

Valuation:

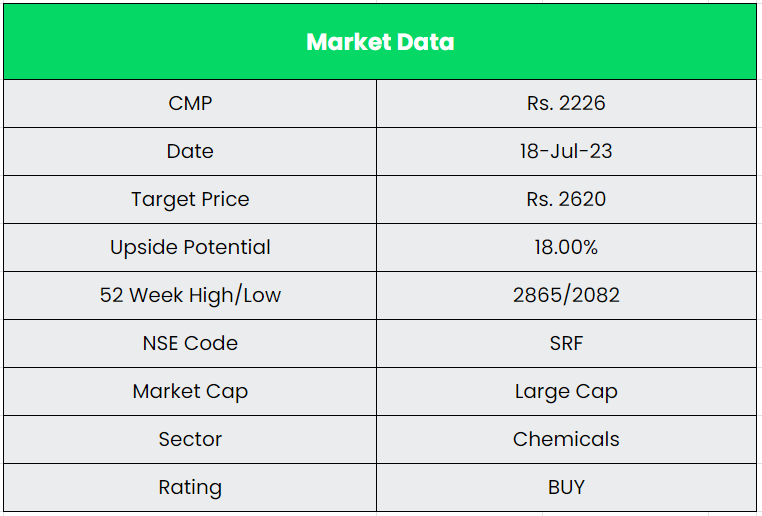

SRF’s strategic positioning across diverse geographies, coupled with its recent capacity expansion plans, places the company in an advantageous position to capitalize on the surging demand in both domestic and international markets. We recommend a BUY rating in the stock with the target price (TP) of Rs.2620, 26x FY25E EPS.

Risks:

- Regulatory Risk – The chemical industry is subject to stringent environmental regulations and safety standards. Non-compliance with these regulations can lead to penalties, legal issues, and reputational damage.

- Raw Material Risk – Fluctuations in the prices of raw materials, such as Crude, minerals, and Flourspar, Methanol, etc. can significantly impact the cost structure and profitability of the company.

- Capex Risk – Stretched payback of specialty chemicals capex due to lower margins or any delay in the execution of the projects will impact the company.