Jupiter Wagons Ltd – Leading Manufacturer of Railway Freight Cars

Incorporated in 2006, Jupiter Wagons Ltd (JWL) is one of the most integrated Railway Engineering Company, catering to clientele spread across Indian Railway (IR), private wagon aggregators, commercial vehicles OEMs, Indian defence, and logistics companies. It is a premier manufacturer of railway wagons, passenger coach components, alloy steel casting for rolling stack and track. On a standalone basis, JWL has a capacity to manufacture ~8,000 wagons annually and is backward integrated with a foundry shop to manufacture various components of a typical wagon like couplers, bogies, draft gears, CRF section, etc. It boasts one of the highest capacity complements and holds the distinction of being India’s largest manufacturer of 25-ton wagons. The company has 6 state-of-the-art factories and 2 offices for production and testing and development.

Products and Services

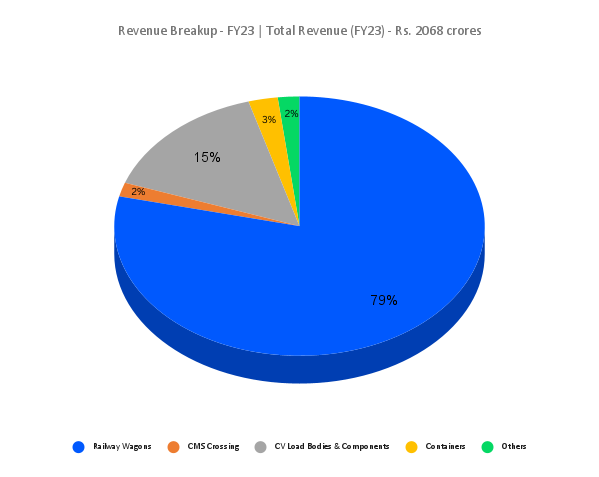

Jupiter Wagons is a comprehensive solutions provider in passenger coaches and freight wagons and accessories. The company’s wide range of products includes brake systems, tippers, trailers for mining, infrastructure, and construction, as well as specialised vehicles such as municipal disposers, refrigerated vans, defence vehicles, reconnaissance vehicles, RAF vehicles, water tankers, oil tankers, containers, commercial electric vehicles and more. It has two main business divisions: Rail mobility (encompassing wagons, track solutions, wagon accessories and passenger coach accessories) and Road & Multimodal mobility (encompassing Commercial Vehicles and Containers).

Subsidiaries: As of FY23, the company has two subsidiary companies and three associate and/or joint venture companies.

Key Rationale

- Expansion plans – The company is planning to increase the capacity of its existing foundry at Kolkata plant parallel to setting up a new foundry at Jabalpur plant, increasing the overall capacity from 2,500 metric tons to 5,000 metric tons in aggregate at two locations with an execution period of 18 to 24 months. This will increase the production from 700 wagons per month to 1000 wagons per month. Additionally, it is adding wheel set manufacturing capabilities to improve backward integration. This will result in improved margins by achieving a reduction in freight costs and improved production efficiencies. It has a capex plan of around Rs.700 crore by the end of next financial year. The company recently raised Rs.400 crore through Qualified Institutional Placement (QIP).

- Recent acquisitions – The company acquired Stone India Limited which is into the business of brake systems and train lighting alternators and a supplier of engineering products to IR. The company is planning to revamp the Stone India facilities with a capex of Rs.30 crore earmarked for facility modernisation with operations commencing by Q4FY24. It is planning to commence the freight brake business in Stone India and later step into manufacturing brakes for locomotives, High-Reach Pantograph and various kind of valves for the locomotive business.

- Robust order book – Jupiter Wagons has a healthy order book backed by unabated demand for wagons from IR and private players. As of Q2FY24, it has an order book of Rs.5952 crore, wherein Rs.5355 crore is being contributed from wagons. Additionally, the company has bagged an order for manufacture and supply of 4 rakes of Double Decker Automobile Carrier Wagons worth around Rs 100 crore and another order from Ministry of Defence to manufacture and supply of 697 Boggie Open Military (BOM) wagons worth Rs.473 crore.

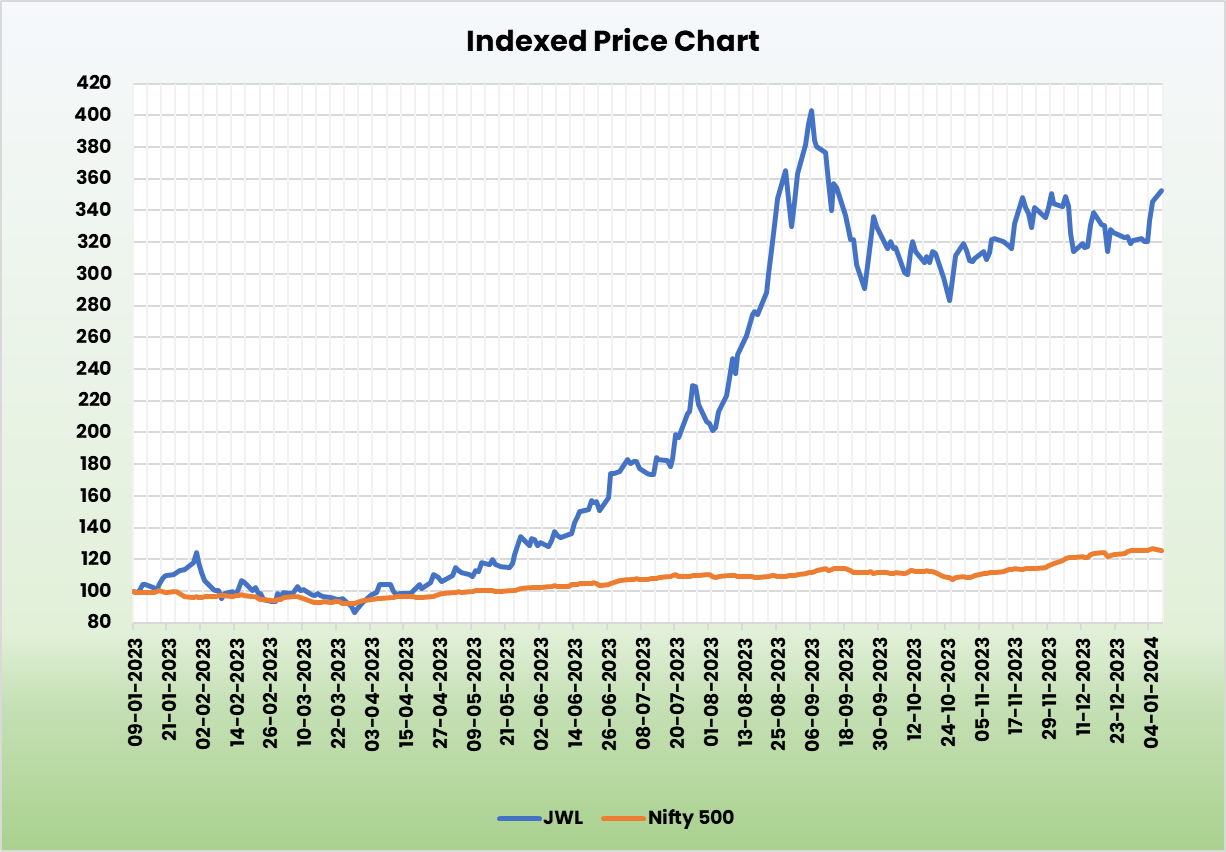

- Q2FY24 – Jupiter Wagons achieved triple digit growth in revenue, EBITDA, and net profit during the quarter. The momentum has been strong, particularly in the wagon business. During the quarter, the company reported a consolidated total revenue of Rs.879 crore versus corresponding Rs.417 crore of Q2FY23, an increase of 111%. EBITDA for the period was Rs.121 crore marking an upside of 142% YoY compared to Rs.50 crore of Q2FY23. As compared to Q2FY23, net profit in Q2FY24 increased by 228% to Rs.82 crore. On account of the enriched product mix and economies of scale, the EBITDA margin improved by 180 basis points from 12% in Q2 FY2023 to 14% in Q2 FY2024.

- Financial Performance -The company has generated standalone revenue and PAT CAGR of 84% and 40% over the period of 5 years (FY18-23). Average 3-year ROE & ROCE is around 13% and 18% for FY20-23 period. The company has strong balance sheet with a robust debt-to-equity ratio of 0.35.

Industry

Indian railways span thousands of kilometres practically covering the entire nation, making it the fourth largest in the world after the US, China, and Russia. The railway network is considered cost-effective and ideal for long-distance travel and movement of bulk commodities. Indian Railways’ revenue reached US$ 5.21 billion in Q3FY23. From April-January 2023, railway freight loading of 1243.46 MT was achieved against last year’s loading of 1159.08 MT which depicted an improvement of 7%. 400 new generation Vande Bharat trains are estimated to be manufactured during the next three years. Railway passenger traffic is projected to reach around 12 Bn per year by 2031 and freight traffic is expected to cross 8,220 Mn tonne by 2031. India is projected to account for 40% of the total global share of rail activity by 2050. With the advent of initiatives such as Vande Bharat, Dedicated Freight Corridors (DFC), Metro Rail and Regional Rapid Transit System (RRTS), coupled with the government’s increased focus on Indian Railways the industry and associated companies are expected to achieve robust growth.

Growth Drivers

Government has allowed 100% FDI in the railway sector. Under the Union Budget 2023-24, capital outlay of Rs. 2.40 lakh crore (US$ 29 billion) has been allocated to the Ministry of Railways, which is the highest ever outlay. The Indian Railway launched the National Rail Plan, Vision 2024, to accelerate implementation of critical projects, such as multitrack congested routes, achieve 100% electrification, upgrade the speed in strategic routes and eliminate all level crossings on the GQ/GD route, by 2024.

Competitors: Titagarh Rail, Texmaco Rail & Engineering Ltd etc.

Peer Analysis

In comparison with its listed competitors, with a robust growth in revenue, JWL is ahead in terms of performance ratios, indicating the company’s financial stability and its efficiency to generate income and returns from the invested capital.

Outlook

Fuelled by high demand for wagons and containers, strategic expansion into international markets, backed by solid order book and promising partnerships, we believe Jupiter Wagons Ltd is in a trajectory of continuing its current growth streak. The boost given by Indian Railways to expand its infrastructure and the “Make in India” initiative gives significant boost to the railway sector and its associated companies. We believe Jupiter Wagons is suitably placed to capitalise on this and tap the market share. The company has set up the stage to enter the commercial electric division under a separate entity formed with GreenPower Motor Company known as Jupiter Electric Mobility aiming to emerge as a leading player in India’s commercial electric vehicle segment.

Valuation

We are positive on the future growth prospects of Jupiter Wagons Ltd given the thrust given by Indian Railways and private sector on rail infrastructure, company’s significant market share coupled with capacity expansion in wagon business and diversification of product portfolio. Hence, we recommend a BUY rating on the stock with target price (TP) of Rs. 406 at 19xFY25EPS.

Risks

- Dependence on Railways – IR being the major customer for wagons, any adverse impact on budget allocation of Railways will impact the order flow. The company has mitigated this risk partly by developing wagons for private operators.

- Execution delay – Delay in timely execution of the orders may impact revenue generation. The company has laid out plans for capacity enhancements. Any delays in this getting executed might affect the business and turnarounds.