Berger Paints India Ltd. – Paint Your Imagination

Berger Paints India Ltd (BPIL), incorporated in 1923, is one of the leading manufacturers and sellers of paints and varnishes in India with an established brand. It is present in both the decorative paint and the industrial segment, namely, general, automotive, protective and powder coatings. BPIL has 24 manufacturing plants located in India (including plants of subsidiaries in India), Nepal, Poland, Bangladesh and Russia. It also has ~180 stock stations. Its decorative segment includes brands, such as Weathercoat, Luxol, Silk and Easy Clean. The Berger Group (comprising BPIL, its subsidiaries and associates and its other group companies) also has an international presence in eight countries, including Russia, Nepal, Bangladesh, and in certain countries of Europe.

Products & Services:

Berger Paints offers a diverse range of products in both decorative and industrial paint segments.

- Decorative Paints – Interior Wall Coatings, Exterior Wall Coatings, Wood Coatings, Metal Coatings, Enamels and Distempers under the brands WeatherCoat, Silk, Luxol, Solitaire, etc.

- Industrial Paints – Protective Coatings, Powder Coatings, Marine and Container Coatings, Road Marking Paints, Waterproofing under the brands UltraCoat, QualiCoat, Duraberg, Epilux, Home Shield, etc.

Subsidiaries: As on FY23, the company has a total of 8 Subsidiaries, 6 Step down subsidiaries and 2 Joint Venture companies.

Key Rationale:

- Established Position – Berger Paints has established a formidable position in the Indian paint industry, solidifying its reputation as the second-largest paint company in the country. Its success extends beyond national boundaries, with a presence in all paint segments and a prominent standing among the top 15 paint companies worldwide. In Asia, Berger Paints proudly ranks among the top four paint companies, while globally, it claims a spot among the top seven architectural (decorative) coating companies. The company has been consistently improving its market share. In FY23, its market share stood at approximately 19.3%, compared to 19% in FY22 and 18.6% in FY21. Berger Paints is the market leader in the protective coatings business in India.

- Product Innovation – Berger Paints has recently launched a range of exciting offerings. During Q4FY23, the company introduced a cutting-edge product called “antidust cool,” revolutionizing the paint industry with its unique features. Additionally, the expansion of the wood coating range has welcomed three new products: Imperia Trend, Imperia Breathe Easy, and Imperia Dura Coat. Capitalizing on its success, Berger Paints has experienced robust growth in the premium luxury category, spearheaded by its highly acclaimed brands, Easy Clean and Anti Dust. These brands not only lead their respective categories but also continue to make remarkable progress. However, under luxury category (the most premium segment), the interior luxury product called silk glamour, has not performed as expected.

- Q4FY23 – Berger Paints achieved a decent financial performance in Q4FY23. The company reported an 11.7% YoY increase in revenue, reaching Rs.2444 crore, bolstered by a strong 11% growth in overall volume. The decorative paints segment experienced even higher volume growth, with an impressive 14.5% rise attributed to dealer expansion and the successful launch of new products. While gross margin improved by 93 bps YoY due to lower raw material prices, higher operating expenses counteracted the benefit, leading to a decline in EBITDA margin by 170 bps YoY to 14.1%. Unfortunately, the company faced a setback as the joint venture company, Berger Becker Coatings Pvt Ltd, encountered a fire in its Goa factory, resulting in a share of loss amounting to Rs.22 crore. So, the PAT declined 15.6% YoY to Rs.186 crore.

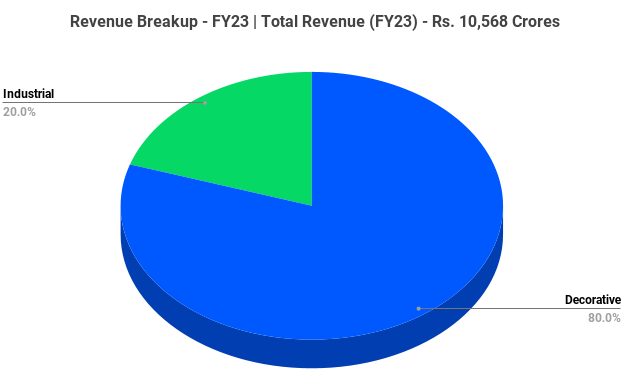

- Financial Performance – The company’s revenue has multiplied nearly 22 times in a span of 22 years, surging from Rs.490 crore in FY01 to an impressive Rs.10,568 crore in FY23, reflecting a remarkable CAGR of 15%. Simultaneously, the EBITDA has demonstrated consistent growth, maintaining a robust CAGR of 17% during the same period. FY23 marked a significant milestone for the company, surpassing the Rs.10,000 crore revenue mark for the first time in its history. Additionally, the protective coatings segment celebrated a remarkable accomplishment by exceeding Rs.1,000 crore in revenue during FY23. Also, Berger Paints successfully commissioned a state-of-the-art, fully automated manufacturing facility in Sandila, Hardoi, Uttar Pradesh. With a substantial investment of Rs.1,037 crore during FY 2022-23, this facility commenced commercial production on February 6, 2023, bolstering Berger Paints’ manufacturing capabilities.

Industry:

The Indian paint industry is set to cross Rs.1 lakh crore in sales by 2027/28 from the current Rs.75,000 crore clocking a compounded annual growth rate of 9-10%. The paint industry in India is expected to add 2.5 million kilolitres of capacity over the next three years, which is about 20 percent of the existing capacity. The total capex outlay for the industry stands at Rs.20,000 crore, 50 percent of which will come in from the Grasim Industries, which is investing Rs.10,000 crore. Asian Paints is also looking to mark its presence with a capex outlay of Rs.8,000 crore. Other companies are also investing Rs.2,000 crore for expanding their respective capacities. The decorative paints segment is the largest category within the Indian paints industry. It includes interior and exterior wall paints, enamels, distempers, emulsions, and wood coatings. This segment is driven by factors such as increased urbanization, rising disposable incomes, and growing demand for aesthetic home decor. As much as 75% of the sector’s revenue comes from the decorative segment and the rest from the industrial segment. Within decorative, repainting accounts for 70% of revenue.

Growth Drivers:

- The Indian government has been emphasizing infrastructure development with initiatives such as Smart Cities Mission, Pradhan Mantri Awas Yojana (PMAY), and Atal Mission for Rejuvenation and Urban Transformation (AMRUT). These initiatives involve the construction of roads, bridges, public buildings, and affordable housing, which generate substantial demand for paints and coatings.

- As the Indian middle class continues to expand, disposable incomes are increasing. With higher incomes, consumers are spending more on home decor, including painting and renovation, thus driving the demand for decorative paints.

- India is experiencing rapid urbanization, with a significant rise in urban population and the expansion of cities. Urbanization leads to increased construction activities, renovation projects, and demand for paints in residential and commercial sectors, driving the growth of the paints industry.

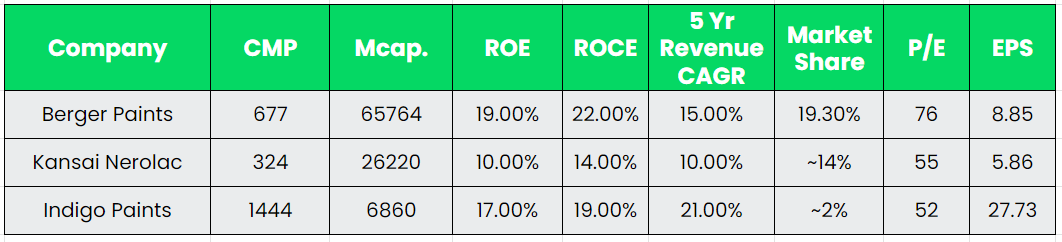

Competitors: Kansai Nerolac, Indigo Paints, etc.

Peer Analysis:

Berger Paints is a prominent player in the paint manufacturing industry and holds the position of the second-largest paint manufacturer in India, following Asian Paints. In terms of financial performance, Berger Paints has demonstrated impressive results that outshine its close competitors. Moreover, Berger Paints has strategically focused on expanding its production capacity and dealer network, which bodes well for its future growth prospects.

Outlook:

Following the commissioning of the Sandila plant, Berger Paints has experienced a significant increase in overall capacity, which has risen by 35% to 95,000 MT. The company has set a target to achieve 70-75% utilization at this plant within the next two years. While some capacity additions are planned for FY24, there are no further greenfield projects anticipated during that period. However, the company has announced plans to establish a new plant in Panagarh, West Bengal by March 2025. This plant will focus on producing industrial paints and construction chemicals. With these expansion plans in place, Berger Paints’ management is confident in doubling its revenue over the next five years, targeting a 15% compound annual growth rate (CAGR). Currently, the company has 40,000 touchpoints, and it intends to add an additional 8,000 retail touchpoints in FY24. The management believes that this expansion will drive an additional 4%-5% volume growth. Berger Paints’ management is committed to maintaining a gross margin range of 38-40%, supported by benign raw material prices. Additionally, they anticipate an improvement in EBITDA margin from Q1FY24 onward and have set a guidance of 16-17% EBITDA margin in the near term, aided by cost savings in areas such as freight costs.

Valuation:

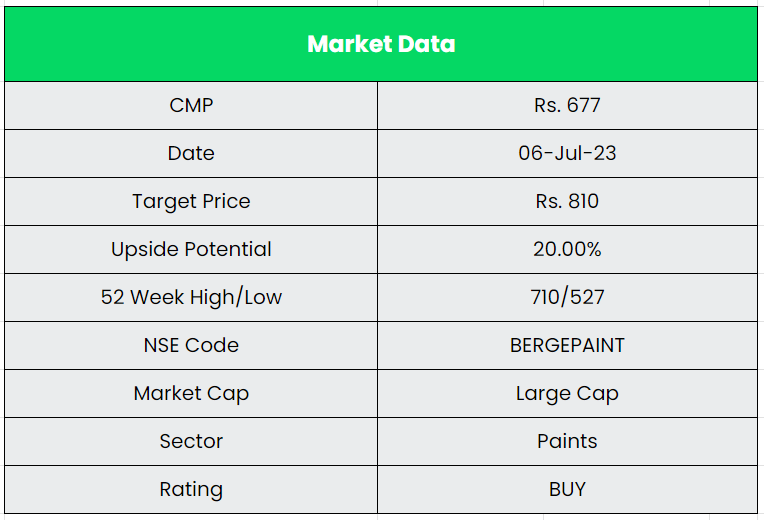

Considering Berger Paints’ strong position in both the decorative and industrial paint segments, as well as its capacity expansion and new product launches, it could be considered as an attractive play in the Paint Industry. We recommend a BUY rating in the stock with the target price (TP) of Rs.810, 60x FY25E EPS.

Risks:

- Competitive Risk – The Indian paint industry is characterised by presence of few large players in the organised segment who control significant market share, while there are some smaller regional players in the unorganised segment as well. Entry of Grasim, Pidilite, etc. will create a tough competition among the existing organised players.

- Raw Material Risk – The prices of raw materials (account for 55-65% of total sales) such as titanium dioxide, crude oil derivatives, pigments and resins are affected by volatility in crude oil prices which can affect margins.

- Forex Risk – BPIL imports around 35% of its raw material requirement, such as Titanium Dioxide from countries like China, Germany, Australia, etc. This exposes the company to foreign currency fluctuation risk in addition to commodity price fluctuation risk.