HCL Technologies Limited, incorporated in 1991 and headquartered in Noida, Uttar Pradesh, is a global technology company delivering industry-leading capabilities centered around artificial intelligence, digital, engineering, cloud and software. The company operates through three reportable segments: IT and Business Services, Engineering and R&D Services, and HCLSoftware, providing a comprehensive range of technology services and products to various critical sectors. As of December 31, 2025, HCLTech employed 226,000+ professionals across 60+ countries. The company’s integrated model includes in-house R&D, collaboration studios, experience zones, and specialized labs for innovation.

Products and Services

The company’s business can be categorised across the below business segments:

- Engineering and R&D Services – Provides end-to-end engineering services, including product and digital engineering, covering the full product lifecycle across industries.

- IT and Business Services (ITBS) – Delivers integrated digital transformation solutions across applications, infrastructure, cloud, AI and digital process operations for global enterprises.

- HCLSoftware – IP-led portfolio spanning Total Experience, Business Applications and Industry solutions, Data & Analytics, Intelligent Operations, Security & Compliance, Specialized Software and Sovereign Collaboration.

- AI and GenAI – Supports enterprise AI adoption through platforms such as AI Force, AI Foundry, AI Labs and AI Engineering, enabling scalable, real-world AI deployments.

Subsidiaries – As of FY25, the company has 124 subsidiaries and 3 associate companies.

Investment Rationale

- Strong Deal Wins Provide Revenue Visibility and Downside Protection – HCLTech’s deal momentum remains a key earnings visibility driver, with net new bookings of $3.0bn in Q3FY26, marking 17% QoQ and 43% YoY growth, and the highest ACV booking in the last four years. Notably, 63% of bookings were driven by Applications and ER&D, where demand resilience is stronger versus discretionary digital spends. The company secured a $473mn, 5-year mega deal with a global apparel retailer, with revenue contribution expected to begin from Q4FY26, improving medium-term growth visibility. Client mining also strengthened, with one new $100mn client, three $50mn, and 15 $20mn clients added, reflecting both wallet share gains and vendor consolidation wins (notably in US insurance). This breadth and size of deal wins materially reduce near-term earnings risk amid a volatile macro environment.

- Partnerships and Acquisitions Strengthen AI and Software Monetisation – HCLTech’s partnerships and acquisitions are increasingly focused on monetisable AI and IP-led growth, rather than experimental investments. The launch of OEM-aligned AI Factory offerings with Dell, HPE, Cisco, NVIDIA, AWS, Azure and GCP, alongside a Physical AI Lab with NVIDIA, positions HCLTech as a scaled system integrator for enterprise AI deployments. Advanced AI revenues grew 19.9% YoY, led by Agentic Physical AI and AI Factory programs, indicating early commercial traction. On the software side, acquisitions of Jaspersoft and Wobby enhance Actian’s data management stack, enabling an end-to-end governed analytics and GenAI platform – supporting higher-margin, recurring revenues. Additionally, the acquisition of HPE’s Telco Solutions business expands HCLTech’s telecom engineering IP, already translating into a stronger pipeline. These moves collectively improve margin durability and long-term valuation support.

- Q3FY26 – During the quarter, the company reported consolidated revenue of Rs.33,872 crore, up 13.3% YoY compared to Rs.29,890 crore in Q3FY25. EBIT stood at Rs.6,285 crore (18.6% margin), up 8.0% YoY from Rs.5,821 crore, and net profit was recorded at Rs.4,795 crore (14.2% margin), posting a growth of 4.5% YoY from Rs.4,591 crore. The quarter witnessed exceptionally strong deal bookings, with Advanced AI revenue growing 19.9% QoQ, and the company crossing US$15 billion in annualized revenues.

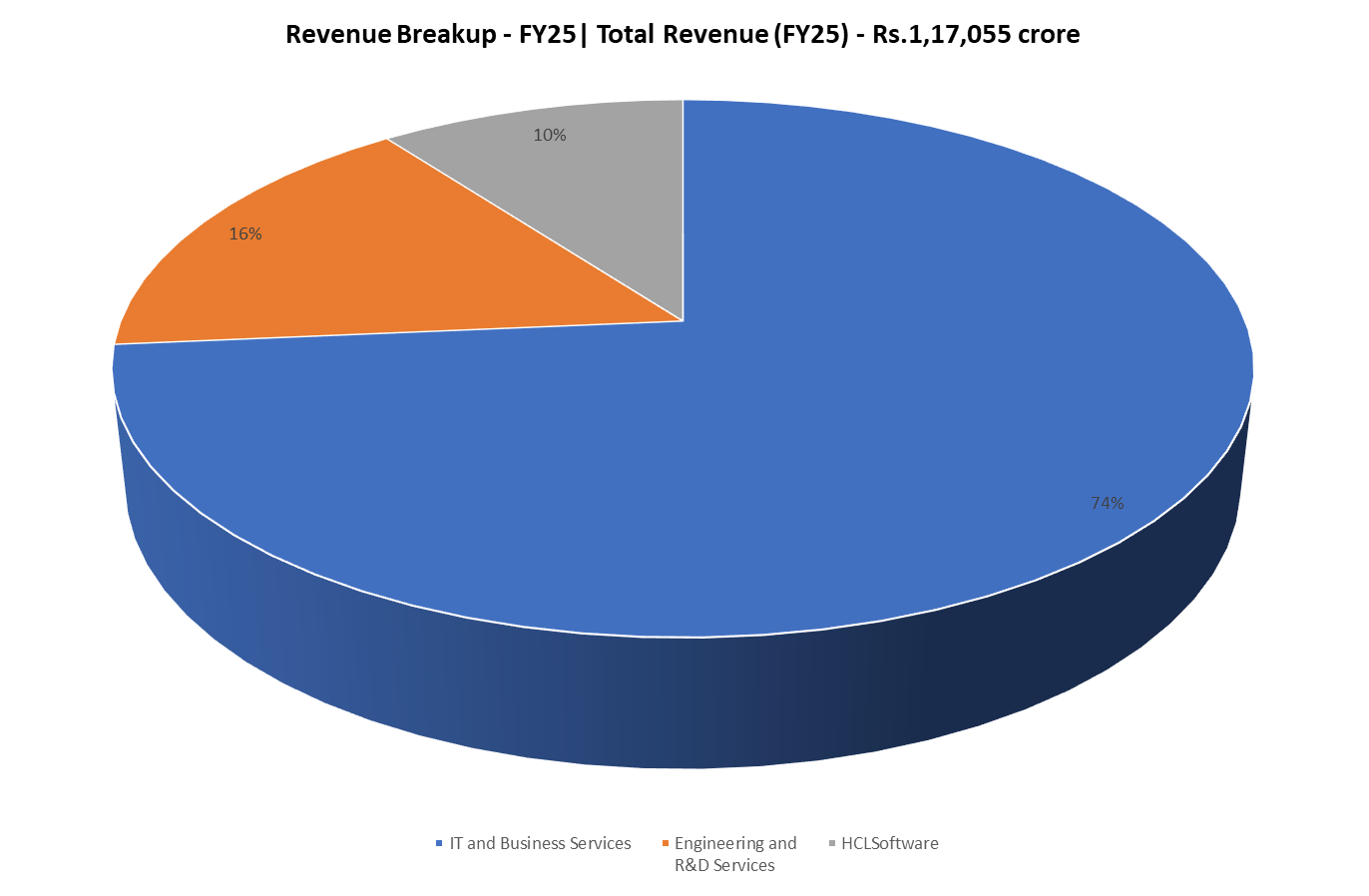

- FY25 – During FY25, the company reported consolidated revenue of Rs.1,17,055 crore, representing a 6.5% YoY increase compared to Rs.1,09,913 crore in FY24. EBIT stood at Rs.21,420 crore, up 7.0% YoY, and net profit was recorded at Rs.17,390 crore, posting a growth of 10.8% YoY.

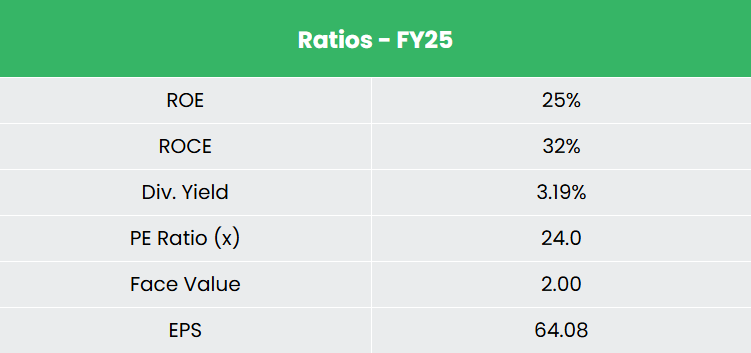

- Financial Performance – The 3-year revenue and net profit CAGR stands at 11% and 9% respectively between FY23-25. The company maintains a healthy capital structure, with a debt-to-equity ratio of 0.10x and the 3-year average ROE and ROCE are around 24% and 30% for FY23-25 period.

Industry

The Indian IT-BPM sector has emerged as a critical pillar of the economy, with revenue estimated at Rs.24,29,838 crore (US$283 billion) in FY25, growing at a CAGR of ~9% from Rs.10,13,148 crore (US$118 billion) in FY15. Export revenue reached Rs.19,23,264 crore (US$224 billion) in FY25, registering 12.5% growth from US$199 billion in FY24, with IT services accounting for 66% of total exports, followed by Business Process Management at 26% and Engineering R&D and software products at 8%. The industry attracted cumulative FDI inflows of Rs.7,84,971 crores (US$110.70 billion) between April 2000-March 2025, ranking second in sectoral FDI and contributing 15.19% of total cumulative FDI equity inflows. India’s IT spending is projected to rise 11.1% YoY to US$161.5 billion in 2025, with the sector on track to double revenue to Rs.43,10,000 crores (US$500 billion) by 2030, driven by AI adoption, cloud transformation, and expansion of Global Capability Centers expected to generate 22-25% of net new white-collar tech jobs.

Growth Drivers

- AI and emerging technology proliferation – India’s AI market is expected to contribute US$957 billion to GDP by 2035, supported by the IndiaAI Mission’s Rs.10,300 crores allocation.

- Cloud adoption and data center expansion – India’s public cloud services market is projected to grow from US$6.2 billion in 2022 to US$17.8 billion by 2027 at 23.4% CAGR, with data center capacity expected to triple from 870 MW in 2023 to 2,500 MW by 2027.

- Expanding Global Capability Centers and geographic diversification – GCCs are expected to generate 1.2 million of the 4.7 million new tech jobs projected by 2027, with non-metro cities driving over 50% IT hiring growth in H1 2025, offering 30% cost savings.

Peer Analysis

Competitors – Wipro Ltd, LTIMindtree Ltd, etc.

Compared to its peers, the company demonstrates superior profitability, strong overall financial performance, and disciplined capital allocation. The company boasts industry leading earnings quality, with the 3-year average CFO/PAT ratio 1.3x, and a large cash position of Rs.34,306 crore as on Q3FY26.

Outlook

HCLTech enters the coming quarters with a strong financial cushion, supported by $2.5bn in operating cash flows and $2.35bn in free cash flows over the last 12 months, translating into healthy OCF and FCF conversion of 127% and 120%, respectively. A robust balance sheet provides flexibility to invest while protecting downside. Management has raised FY services revenue growth guidance to 4.75 – 5.25% CC (constant currency) and company-level growth to 4 – 4.5% CC, reflecting confidence in deal momentum and execution. EBIT margins are expected to remain within the 17 – 18% band, despite near-term pressure from restructuring costs, with Q4 margins likely to see a temporary dip. Key monitorables include timely ramp-up of large deals, AI monetisation visibility and margin normalisation post restructuring, particularly in a volatile demand environment.

Valuations

We remain positive towards the company’s long-term growth outlook given the improvement in scale. We recommend a BUY rating in the stock with the target price (TP) of Rs.2,015, 26x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

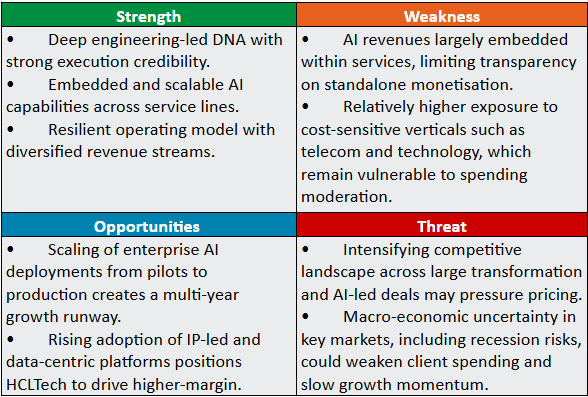

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.