Bharti Airtel Ltd – The Safe Network

Bharti Airtel Ltd., established in 1995 and headquartered in New Delhi, is a leading global provider of telecommunications and digital communication services. With a customer base exceeding 600 million across 17+ countries in India and Africa, the company also maintains a presence in Bangladesh and Sri Lanka through its associate entities. Airtel ranks among the top three mobile network operators worldwide, with its infrastructure reaching over two billion people. Domestically, it stands as India’s largest integrated communications solutions provider, while in Africa, it holds the position of the second-largest mobile operator.

Products and Services

Bharti Airtel’s offerings are structured across five key business segments:

- Mobile Services: Includes prepaid, postpaid, roaming, high-speed data, and value-added services for individual and enterprise users.

- Home Services: Provides fixed-line voice and high-speed broadband connectivity to residential customers.

- Digital TV Services: Offers DTH services under the Airtel Xstream brand, delivering standard and HD channels along with digital content.

- Airtel Business: A leading ICT provider offering enterprise solutions such as fixed-line voice (PRIs), data connectivity (MPLS, VoIP, SIP), and conferencing tools.

- Passive Infrastructure: Through Indus Towers Ltd., Airtel offers telecom tower infrastructure services, supporting network deployment and maintenance across India.

Subsidiaries: As of FY25, the company has 145 subsidiaries, 5 joint ventures and 7 associate companies.

Investment Rationale

- Strategic alliances – The company is driving digital leadership through strategic partnerships and differentiated offerings. Its exclusive tie-ups with Apple TV, Apple Music, and Google One enhance value for postpaid and Wi-Fi customers, offering premium content and 100GB cloud storage at no additional cost. The launch of an industry-first all-in-one OTT pack for prepaid users, with access to 25+ platforms, further strengthens customer stickiness. Airtel is also investing in frontier technologies, evident in its agreement with SpaceX to bring Starlink’s high-speed satellite internet to India, improving rural and remote connectivity. The company is expanding its global infrastructure with the landing of SEA-ME-WE 6 and 2 Africa Pearls subsea cables. Its AI-led partnership with Perplexity is seeing rapid uptake, crossing 5 million users within days. Furthermore, Airtel Business is pioneering precision-tech in India through an exclusive deal with Swift Navigation, launching the Airtel-Skylark Precise Positioning Service – a cloud-based, AI/ML-powered platform with 100x GNSS accuracy. These initiatives reflect Airtel’s clear focus on convergence, innovation, and high-margin digital services, positioning it well for long-term value creation.

- Strong operational performance – Bharti Airtel delivered a strong operational performance during the quarter, with its mobile segment leading the industry in revenue growth and broadband maintaining solid momentum, driven by continued FWA expansion. The recently launched IPTV business is gaining encouraging traction, reflecting Airtel’s ability to scale new digital offerings. Airtel expanded its infrastructure footprint by deploying 1,830 new network sites and laying over 8,300 km of fiber, in line with its planned rollout. The company added 1.2 million mobile users and 3.9 million smartphone data customers, while postpaid net adds stood at 0.7 million, making up 57% of total additions despite postpaid comprising just 7% of the base. ARPU remained stable at Rs.250, supported by smartphone upgrades, postpaid conversions, and data monetization. 5G adoption reached 152 million users, while the broadband business recorded its highest-ever quarterly net adds of 939,000. Digital verticals, including Cloud, Cybersecurity, IoT, and CPaaS, continue to see strategic investment. Africa operations also remained resilient, with 6.7% sequential constant currency revenue growth, aided by favourable FX impact and delivering 6.2% reported revenue growth.

- Q1FY26 – During the quarter, the company generated revenue of Rs.49,463 crore, an increase of 28% compared to the Rs.38,506 crore of Q1FY25. Operating profit increased from Rs.19,708 crore of Q1FY25 to Rs.27,839 crore of Q1FY26, a growth of 41%. The company reported net profit of Rs.7,422 crore, an increase by 57% YoY from Rs.4,718 crore of Q1FY25. Operating free cash flow was at ~Rs.12,000 crore.

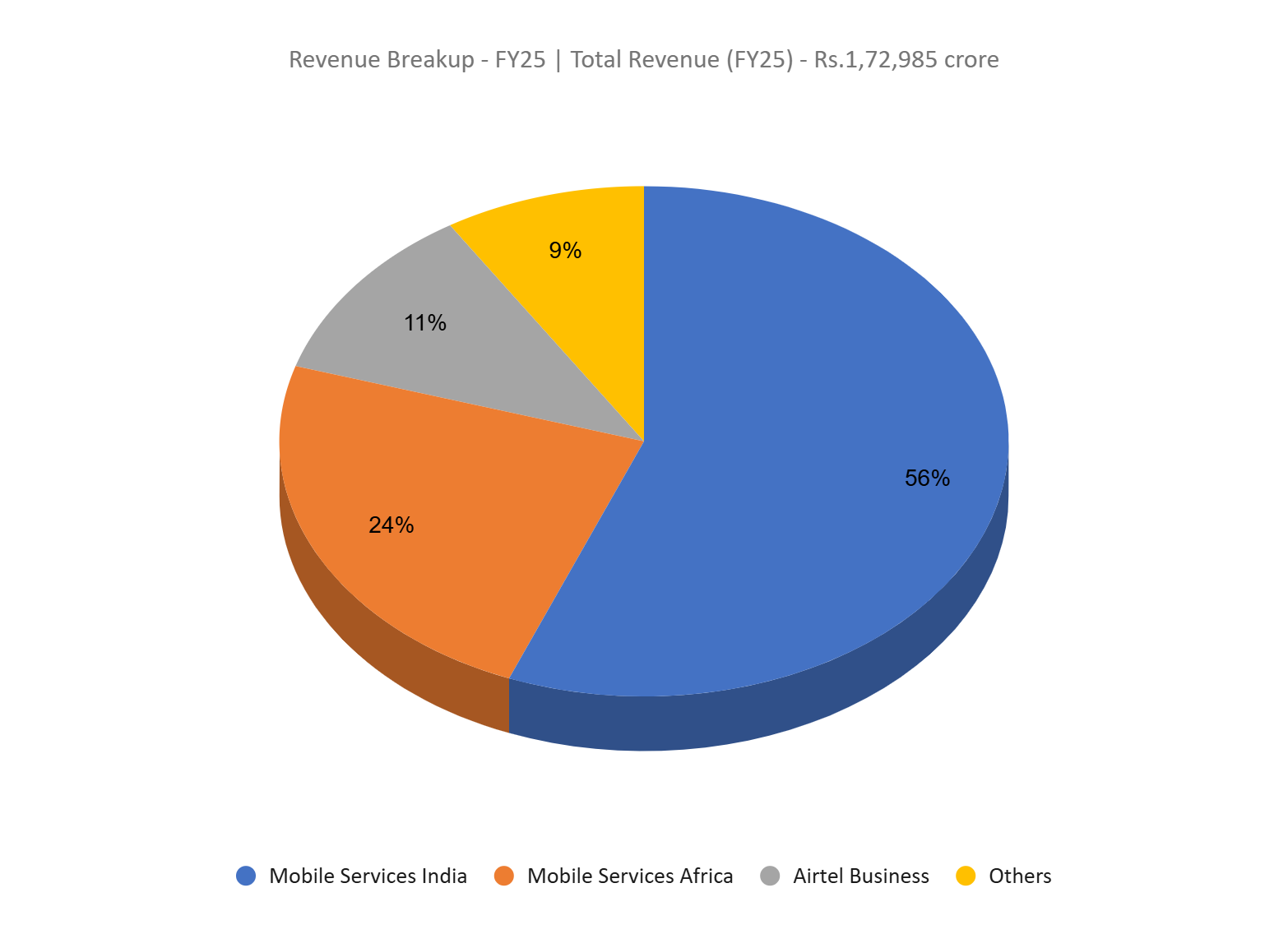

- FY25 – During the FY, the company’s generated revenue of Rs.1,72,985 crore, an increase of 15% YoY. Operating profit was at Rs.1,04,999 crore, up by 18% YoY. The company reported net profit (before exceptional items) of Rs.26,457 crore, an increase of 72% YoY.

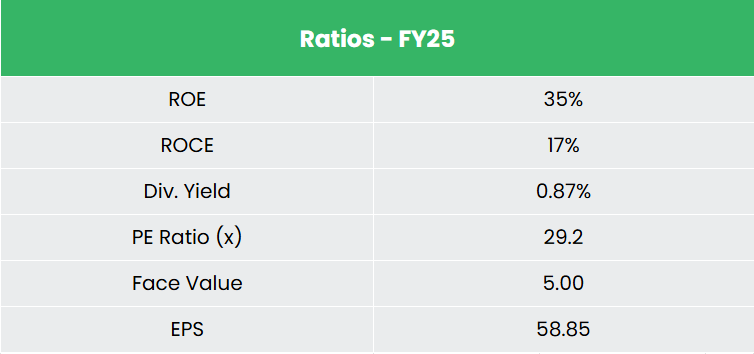

- Financial Performance – The company has generated revenue and net profit CAGR of 14% and 83% over the period of 3 years (FY23-25). Average 3-year ROE & ROCE is around 17% and 13% for FY21-24 period. The company has a debt-to-equity ratio of 1.88.

Industry

India is one of the world’s largest data consumers and the second-largest telecommunications market, with over 1.2 billion subscribers and a tele-density of 85.04% as of March 2025. The sector has witnessed strong growth, supported by liberal government policies, rising digital adoption, and affordable service access. India’s 5G subscriber base is projected to grow 2.65x to 770 million by 2028, reflecting robust demand. The digital economy is expected to contribute 20% to national income by FY30, driven by IT, telecom, and electronics manufacturing. With early investments in 6G and a proactive regulatory framework, India is poised to solidify its position as a global digital leader.

Growth Drivers

- Allocation of Rs. 81,005.24 crore (US$ 9.27 billion) towards the Department of Telecommunications and IT in the Union Budget FY26.

- Government initiatives such as 100% FDI allowed under the automatic route to the telecom services, PLI for Telecom and Networking equipment, reduced license fees, and spectrum liberalization, etc.

- Substantial technological advancements, including the fastest rollout of 5G networks.

Peer Analysis

Competitors: Vodafone Idea Ltd, Tata Communications Ltd, etc.

Compared to its competitors, the company is achieving consistent growth in capital employed, supported by steady revenue expansion.

Outlook

The company remains focused on strategic fibre deployment and accelerated rollouts to support future growth, while capital expenditure is expected to moderate in FY26. The company is exploring deleveraging opportunities and has initiated the exit of low-margin B2B segments, aligning with its strategy of portfolio premiumization. The broader focus is on building a diverse and resilient portfolio across segments. In the broadband business, Airtel sees significant potential in the home segment, with plans to deepen its market presence and scale fibre rollouts. It aims to increase its quarterly home pass run rate from 1.6 million to 2.5 million, with a target of reaching 3x growth in revenue and EBITDA over the next 2 – 3 years.

Valuations

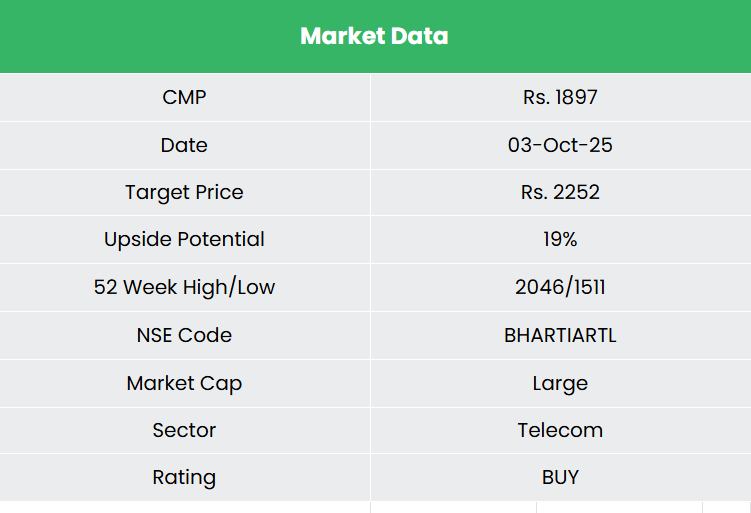

We believe Bharti Airtel is a compelling investment opportunity given its strong market leadership, diversified digital portfolio, and strategic investments driving sustainable growth and long-term value creation. We recommend a BUY rating in the stock with the target price (TP) of Rs.2,252, 34x FY27E EPS. We also encourage maintaining a stop-loss at 20% from the entry price to manage potential downside risk effectively.

SWOT Analysis

Disclaimer: Investments in the securities market are subject to market risks, read all related documents carefully before investing. Securities quoted here are exemplary, not recommendatory. Please consult your financial advisor before investing. Please note that we do not guarantee any assured returns for the securities quoted here.

Research disclaimer: Investment in the securities market is subject to market risks. Read all the related documents carefully before investing. Registration granted by SEBI, and certification from NISM in no way guarantee the performance of the intermediary or provide any assurance of returns to investors.

For more details, please read the disclaimer.