The movie ‘Just My Luck’ starring Lindsay Lohan and Chris Pine has an interesting plot involving luck.

Lindsay plays a character who is always lucky. She works for a great company. She wins every time she plays scratch cards. When she leaves her house, it even stops raining.

Chris, on the other hand, plays a character who is totally out of luck. He works as a janitor. It starts raining when he steps outside. And no matter what he does, something always goes wrong.

What happens when their lives get intertwined makes up the rest of the story!

This movie got me wondering about the role of luck in equity investing –

What would be the portfolio returns of the luckiest and unluckiest equity investors?

Let us find out..

We will take the example of two hypothetical investors Ms Lucky & Mr Unlucky who have been diligently saving a portion of their salary every month for the last 2 decades. As their salaries increased by 5% every year, they also increased their savings by 5%.

They differ, though, in when and how they invest their money in equities.

Both of them believe in timing their entries into equities.

So they keep accumulating their savings in a debt fund every month, and they deploy their entire accumulated amount into equities if they feel the timing is right. They continue with this process for the last 2 decades.

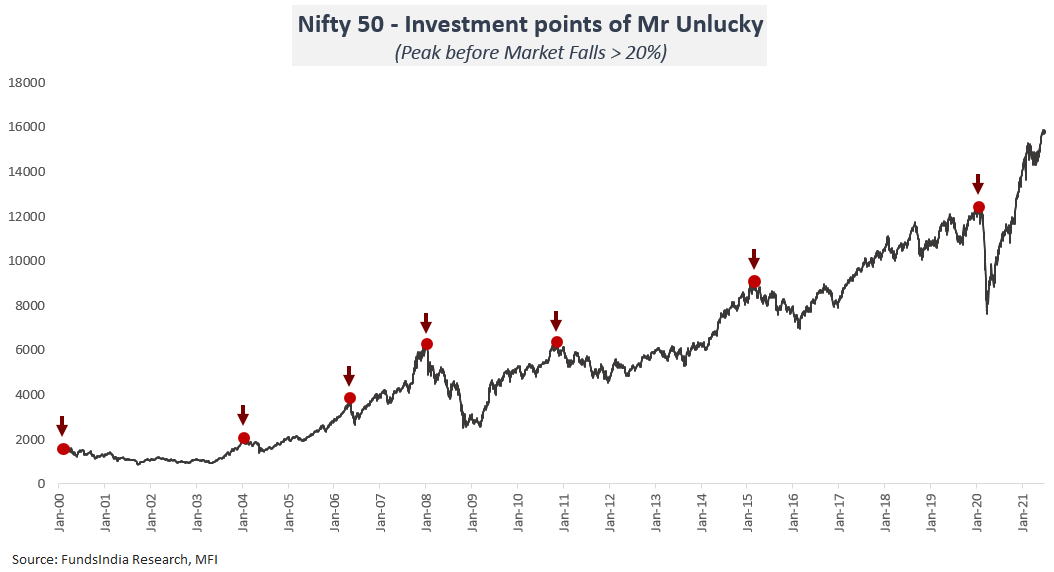

Mr Unlucky – Always invests in equity just before a market fall

Due to his never-ending misfortune and bad timing skills, Mr Unlucky always ends up shifting his accumulated savings from debt into equity just before a market crash (>20% fall).

In the past two decades, he moved his money seven times into equity.

Every single time, the market fell by over 20% immediately after he invested due to different reasons.

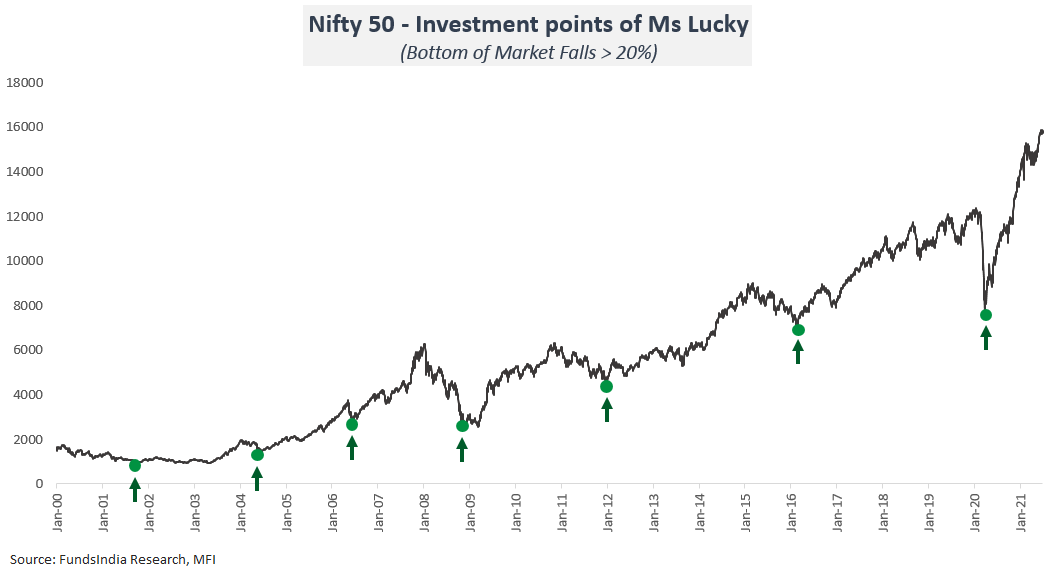

Ms Lucky – Always invests in equity at the bottom of a market fall

Thanks to her incredible luck, she moves the accumulated amount into equity exactly at the bottom of all major falls (>20% declines), every time.

Now here is a quick quiz for you…

What is the annualized return for Mr Unlucky over the past 20 years?

a) 0 to 5%

b) 5 to 10%

c) 10 to 15%

Take a guess?

Intuitively given the unbelievably bad timing skills, it looks like it should be in the 0-5% range.

But hold your breath – Option C is the right answer!

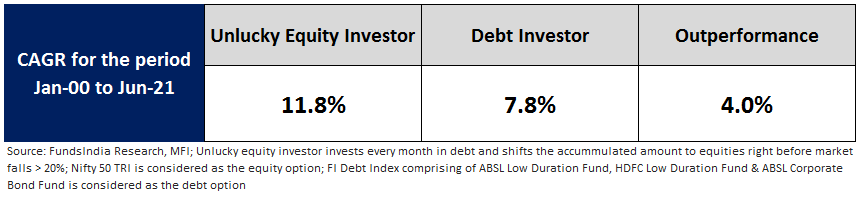

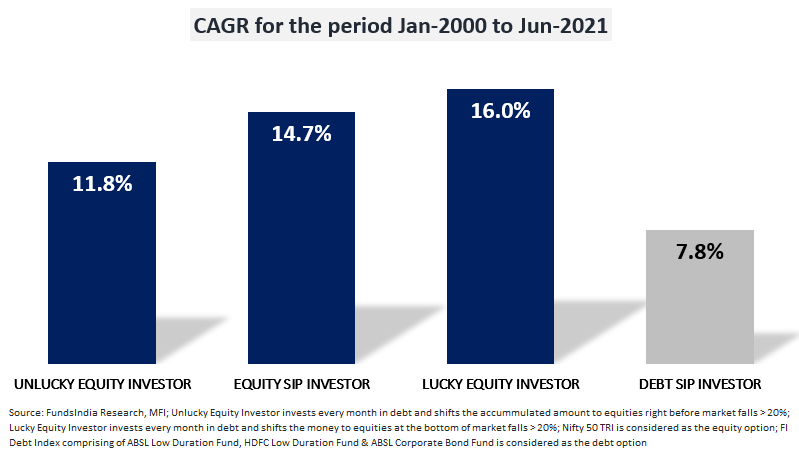

Mr Unlucky made a decent return of 11.8% annually despite his bad timing skills!

Just to put that in perspective, if he had only invested in debt, he would have made an annualized return of just 7.8% in the past two decades – which is significantly lower than the returns of the unlucky equity investor.

Takeaway 1: Even if you were unlucky and only invested right before large market falls, you still made decent returns over the long run – much higher than debt returns

What is the annualized return for Ms Lucky over the past 20 years?

In the case of the lucky investor who timed and invested perfectly at the bottom of all seven declines, the CAGR would have been 16%.

This is fairly intuitive.

But here comes the interesting part…

What if there was another investor – a normal fellow human being like you and me – who has no ability to predict the markets. Let us call him Mr Humble.

Mr Humble instead of regularly investing in debt funds and moving it into equities did a simpler thing – a monthly SIP directly into equities (via Nifty 50 TRI).

What is the annualized return for Mr Humble (the SIP investor) over the past 20 years?

A cool 14.7%!

You read that right. The humble SIP investor’s return was pretty close to the lucky investor who had perfect timing foresight.

Takeaway 2: A Simple SIP comes pretty close to the lucky market timer over the long run

Why are the returns good even when invested at the wrong time?

The answer is really simple – TIME

Though the unlucky investor invested only at the wrong time, he didn’t take his money out after that and withstood all the future declines without panicking out.

This simple but difficult act of patience gave the portfolio a long enough time horizon to let compounding work its magic.

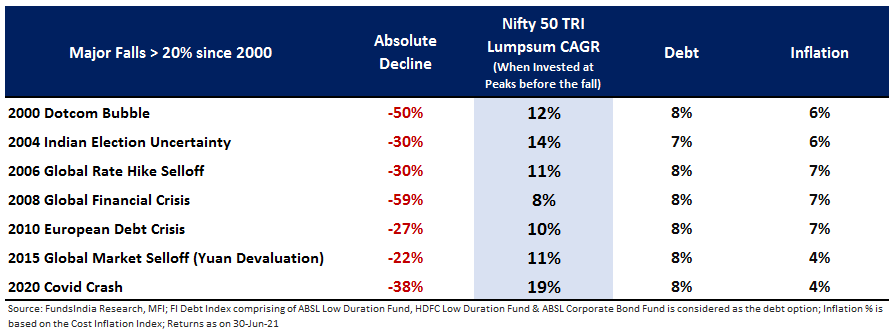

While there is a natural tendency to shrug this off given the simplicity of the solution, here is some hard-hitting evidence.

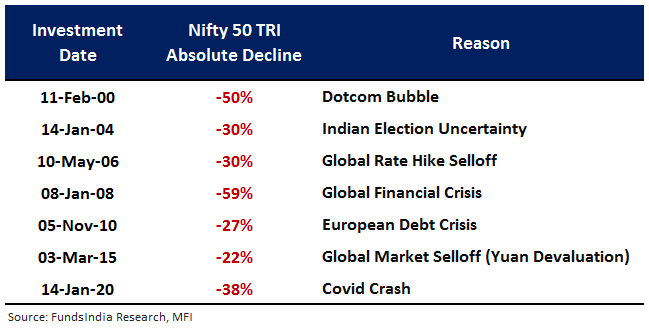

Check out the returns of lumpsum investments in Nifty 50 TRI till date when invested right before the major falls of the past two decades.

As seen above, a long time horizon compensates even for the worst starting points.

Takeaway 3: TIME is a superpower. It works well even for the most unlucky investor!

Summing it up

As seen above with the superpower of time even the most unlucky investor ended up with a reasonable outcome outperforming debt funds and inflation.

A simple SIP removes the need to time the markets and if given enough time provides a return that is almost as good as the hypothetical lucky market timer (who will never exist in reality)!

If you have a long time horizon, a simple SIP in a few good equity funds for the next 10-15 years, and the patience to let it run ignoring all the intermittent noise, is all it takes to ensure a good investment outcome.

Do not let the inherent simplicity of the solution undermine its ability to deliver the magic of compounding.