Ever since the market got its mojo back six months ago, HDFC Top 200 has been overtaking fellow large-cap peers. The 33% it has delivered since March 2016 is better than almost all large-cap funds. In the floundering market before that – from August 2015 to February 2016 when global panic had taken hold, HDFC Top 200 was worse than almost all large-cap funds with a 22% loss.

This see-saw captures the nature of HDFC Top 200. It can spend bear markets worse off than its peers and then outperform peers in recoveries. In the rally from March, sectors that were outside the consumer-focused spectrum are up. HDFC Top 200, which held the majority of its portfolio in such sectors, thus recovered smartly. Investors in the fund can continue to hold, especially having weathered the stark under performance of the past two years.

Risk and returns

To understand why investors can continue to hold the fund, it’s important to know that HDFC Top 200’s strategy demands a higher risk level and patience. Two reasons:

First, the fund takes a two to three-year view on sector and stock prospects with a focus on valuations and so it can hold stocks out of market favour. Moreover, it sticks to its conviction on these sectors or stocks even if short-term sentiments cause price drops. Banking is an example here. In the past three years, it has held to its conviction in banks, especially struggling ones such as State Bank of India, ICICI Bank, and Bank of Baroda.

Given the cheaper valuations in sectors such as energy, power, infrastructure, and engineering, the fund held on to bets such as CESC, Power Grid Corp., ABB, and L&T. The valuation focus also saw the fund pruning FMCG, consumer durables and such where the rally had been sharp. Software, HDFC Top 200’s second-largest sector holding, also did badly in 2015, exacerbating the slump in returns.The 2015 crash in many of these stocks may also have left little room for the fund to shift holdings, given that it stuck to its guns for a good part of this crash.

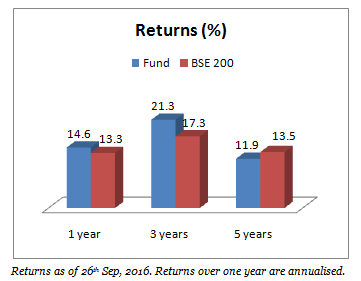

Banking, power, capital goods, oil & gas, infrastructure, commodities have all soared 25-38% since March. This has helped the fund claw back a good part of its losses, pulling its returns just above the category average. The fund’s one-year rolling return in the past five years has it beating its benchmark BSE 200 only 56% of the time. Its 3-year rolling return in the same period, however, has the fund beating the BSE 200 close to 98% of the time.

Secondly, HDFC Top 200 has concentrated stock exposures. The top ten stocks make up almost half the portfolio. Poor performance in the top few can pull down returns even if other stocks happen to do well. Infosys’s bad run in 2015 dragged returns as the stock accounted for around 8% of the portfolio. Other drags include L&T and SBI. These two stocks were in fact factors pulling down performance in 2013 as well.

In both the 2013 sideways market and the 2011 correction, HDFC Top 200 clocked below-average returns. In the subsequent bull-markets, the fund soared well above category average. This crashing and rising makes HDFC Top 200 a very volatile fund; its volatility measured by standard deviation is above the category average. Such volatility in a portfolio will not be suitable for moderate or conservative investors, or those with a relatively shorter horizon.

Low on consistency

The volatility is also the reason that HDFC Top 200 is less consistent than peers. On a 3-year rolling return basis, the fund has not been able to beat its category average almost half the time over the past five years. There are thus other funds available with better consistency and lower volatility. HDFC Top 200’s risk-adjusted returns, measured by the Sharpe ratio, have also taken a blow, holding below the category average.

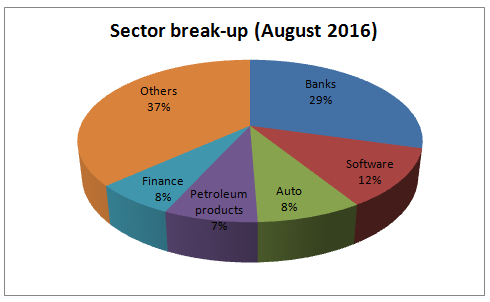

The fund’s current portfolio is still heavy on banking. Exposure to software is down sharply over the past few months. Other top sectors still include the cyclical ones far more than consumer, which is primarily represented only by auto, with some holding in telecom, media, and FMCG. The fund hasn’t been big on pharmaceuticals either in the past five years. Given that a recovery in earnings and the economy is underway, and that consumption sectors have already rallied, HDFC Top 200’s banking and cyclical-heavy portfolio can further benefit as these sectors shine. At this point, it will be better if investors in the fund refrain from any urge to exit.

The fund has an AUM of Rs 13,208 crore. Prashant Jain is the fund’s manager.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis of investment decisions. To know how to read our weekly fund reviews, please click here.

This fund could be a good fit for a satellite portfolio. My risk profile does not prefer a “few yards of extra returns” over consistency in returns.

Regarding Bhavana Acharyas article on HDFC Top 200,I am surprised that she has recommended it when CRISIL says the performance is below par that is relatively weak performance.Is funds india credible?

Hi Rohit,

Crisil and any other rating will show HDFC Top 200 in poor light because they all go by past returns and in the past, the fund has obviously done badly. We’ve said this in the post; that it pales in comparison on consistency and risk-adjusted returns, that it goes through periods of bad performance and revival. HDFC Top 200’s performance from April is a massive turnaround from its past. This revival merited a look. The fund management style is such that it took early calls on some undervalued sectors and then steadfastly stuck to it. The fund’s portfolio is positioned to continue some sort of outperformance going forward. HDFC Top 200 is also widely held by investors and questions about its performance are very frequently raised (it is something we have answered in several comments for several of our other blogposts). These are some of reasons as to why we picked the fund up for review. We’ve not recommended that investors begin investing in this fund today. What we have done is to take stock of the fund’s performance and suggested that investors continue to hold it. For investors who persevered through the bad patch, it would make sense to continue holding it now to make the most of the fund’s revival. The reason why and what kind of fund HDFC Top 200 is, is explained in the post. Hope this clears it up.

Thanks,

Bhavana

Such a nice analysis. Thank you Bhavana. I liked that you covered this with the rolling returns and standard deviation over a period of time. I think I will still hold it and not exit.

This fund could be a good fit for a satellite portfolio. My risk profile does not prefer a “few yards of extra returns” over consistency in returns.

Regarding Bhavana Acharyas article on HDFC Top 200,I am surprised that she has recommended it when CRISIL says the performance is below par that is relatively weak performance.Is funds india credible?

Hi Rohit,

Crisil and any other rating will show HDFC Top 200 in poor light because they all go by past returns and in the past, the fund has obviously done badly. We’ve said this in the post; that it pales in comparison on consistency and risk-adjusted returns, that it goes through periods of bad performance and revival. HDFC Top 200’s performance from April is a massive turnaround from its past. This revival merited a look. The fund management style is such that it took early calls on some undervalued sectors and then steadfastly stuck to it. The fund’s portfolio is positioned to continue some sort of outperformance going forward. HDFC Top 200 is also widely held by investors and questions about its performance are very frequently raised (it is something we have answered in several comments for several of our other blogposts). These are some of reasons as to why we picked the fund up for review. We’ve not recommended that investors begin investing in this fund today. What we have done is to take stock of the fund’s performance and suggested that investors continue to hold it. For investors who persevered through the bad patch, it would make sense to continue holding it now to make the most of the fund’s revival. The reason why and what kind of fund HDFC Top 200 is, is explained in the post. Hope this clears it up.

Thanks,

Bhavana

Such a nice analysis. Thank you Bhavana. I liked that you covered this with the rolling returns and standard deviation over a period of time. I think I will still hold it and not exit.