What is NPS?

National Pension Scheme (NPS) is a old-age retirement savings scheme introduced by the government of India. It allows citizens of the country to save and invest for retirement in a tax-efficient and growth-oriented manner.

Two primary features that distinguish NPS from other government savings schemes are:

1. It allows participation in the equity markets (up to 50% of the portfolio)

2. It is fully tax exempt - tax exempt at source, accrual and withdrawal phases.

Under NPS two types of accounts can be opened and operated

- Tier I Account: This is a non withdrawable account to which the Subscriber shall contribute his/her savings for building a retirement corpus.

- Tier II Account: This is a voluntary savings facility which provides liquidity to subscribers i.e subscribers will be free to withdraw their savings from

this account whenever they wish. Tier I is a re-requisite for opening tier II account. A subscriber need not pay any additional AMCs for tier II account

- Minimum amount per contribution - Rs 500

- Minimum contribution per year - Rs 6,000

- Minimum number of contributions - 1 per year

Who can subscribe to an account?

Any citizen of India between the ages of 18 and 60 are allowed to open an NPS account.

What are the investment criteria?

For Tier-I accounts:

You are required to make your first contribution at the time of applying for registration at any POP - SP. You are required to make contributions subject to the following conditions:

Over and above the mandated limit of a minimum of one contribution, you may decide on the frequency of the contributions across the year as per your convenience.

For Tier- II account

Penalty of Rs. 100/- to be levied on the subscriber for not maintaining the minimum account balance and/or not making the minimum number of contributions.

Where can the money be invested?

The NPS offers you two approaches to invest in your account:

- Active choice - Individual Funds (E, C and G Asset classes)

- Auto choice - Lifecycle Fund

Active choice - Individual Funds

You will have the option to actively decide as to how your NPS pension wealth is to be invested in the following three options:

E - "High return, High risk" - investments in predominantly equity market instruments

C - "Medium return, Medium risk" - investments in predominantly fixed income bearing instruments

G - "Low return, Low risk" - investments in purely fixed income instruments.

You can choose to invest your entire pension wealth in C or G asset classes and upto a maximum of 50% in equity (Asset class E). You can also distribute your pension wealth across E, C and G asset classes, subject to such conditions as may be prescribed by PFRDA. In case you decide to actively exercise your choice about investment options, you shall be required to mandatorily indicate your choice of Pension Fund from among the six Pension Funds appointed by PFRDA.

Auto choice - Lifecycle Fund

NPS offers an easy option for those participants who do not have the required knowledge to manage their NPS investments. In case you are unable/unwilling to exercise any choice, your funds will be invested in accordance with the Auto Choice option.

In this option, the investments will be made in a life-cycle fund. Here, the fraction of funds invested across three asset classes will be determined by a pre-defined portfolio. At the lowest age of entry (18 years), the auto choice will entail investment of 50% of pension wealth in "E" Class, 30% in "C" Class and 20% in "G" Class. These ratios of investment will remain fixed for all contributions until the participant reaches the age of 36. From age 36 onwards, the weight in "E" and "C" asset class will decrease annually and the weight in "G" class will increase annually till it reaches 10% in "E", 10% in "C" and 80% in "G" class at age 55.

Like the active choice subscriber must choose one PFM under auto choice.

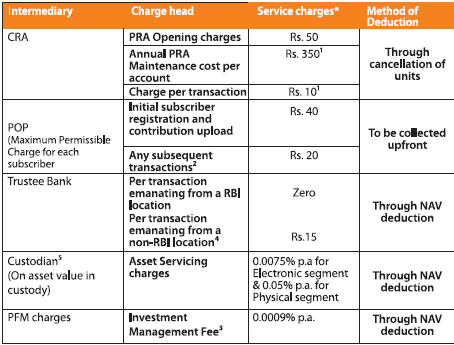

What are the charges for investing in NPS?

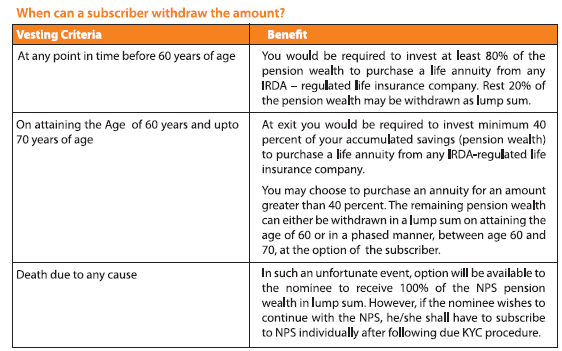

When can money be withdrawn?

For more information on NPS please click here