Come festive season and the attention for gold goes up. This time, the attention may be more as equity markets seem to be disappointing investors and gold prices seem to be climbing. As Diwali nears, a lot of you may be considering accumulating gold during this auspicious time.

But like you weigh the pros and cons of any other investments, you should with gold as well. Gold as an asset class has different demand drivers from equity or debt. Here, we tell you how to look at gold investments and debunk some common myths.

Gold prices are also volatile

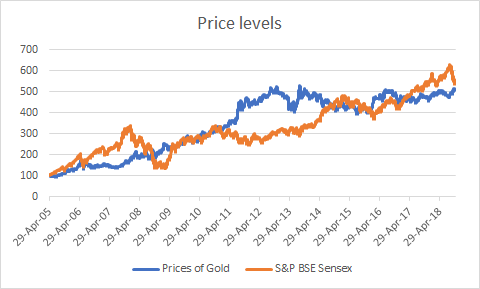

Investors who fear the equity market’s ups and downs are not perturbed by the movement in gold prices. This is mostly because most of us don’t look at gold prices every day like we check the Sensex or Nifty 50. We look at long periods. Gold price today is around Rs.31,735, nearly three times it was ten years ago, painting a rosy picture.

But if we look at the annualized return, like we do with equity investments, the same number is reduced to a simple 10%. That is, on an average, gold has delivered about 10% each year over the past ten years. The Sensex, during this same period, has given an annual growth of 13.6%, despite the correction in the recent months. Global gold prices have, in fact, moved in a narrow band or dipped often for most of the period between 1980-2000.

You may claim that if you could get 10% from gold, why would you invest in risky equity markets? The graph shows the movement of gold prices and equity market levels from 2005. We can see that both the asset classes are volatile. Gold prices are just as likely to depreciate in value as equity does.

The difference between equity (or even debt markets) and gold is that gold prices move only on sentiment. Gold prices chiefly move based on the conditions of the global equity and debt markets, strength of the dollar and overall risk levels. There is no intrinsic value addition that gold on its own as a commodity does. This is unlike equity, since a company would derive value from its business, earnings and revenue growth. It’s also unlike other commodities, which have widespread industrial uses and have their own demand and supply factors. When the global and domestic factors are not positive, investors move to safe haven assets like gold. Domestic gold prices are derived from global gold prices, exchange rates, and duties.

If we see the graph, gold prices saw a steep rise from 2008-2011. The rally started during the 2008 financial crisis and prices continued to run on the back of geopolitical tensions, countries adding to their gold reserves, and reflationary pressure in the US. Much of the gains in gold over the past decade happened during this period. But if you look at the last 5 years (Oct 2013- Oct 2018), gold gave only 0.7% annual returns. Gold prices go through phases in tandem with global markets and external factors unlike equity which does through business cycles.

Gold as an investment

So, going overboard on buying gold thinking of it as an investment will only bring down your overall returns. For the long term, there is no other asset class which can deliver as much returns as equity.

A 10-year SIP in gold would have delivered an IRR of just 5.6%. In comparison, a similar SIP in large-cap funds such as Aditya Birla Sun Life Frontline Equity, SBI Bluechip or ICICI Prudential Bluechip generated an IRR of 13-14%. Those such as Mirae Asset India Equity or Canara Robeco Emerging Equities would have generated a 17-21% IRR. In fact, even the worst multi-cap fund return beat gold.

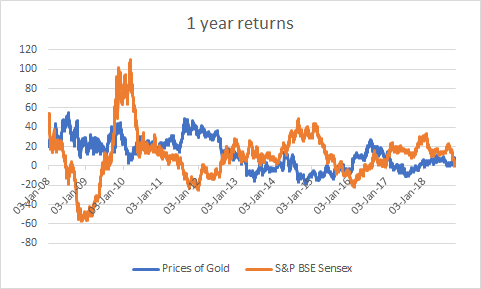

If gold has any purpose at all, it is only to hedge against equity volatility. The graph below shows 1 year returns during different periods from 2008. We can clearly see an opposite trend in gold and equity markets. Equity benefits from economic growth while gold benefits from a distress. The two asset classes are negatively correlated, giving you a hedging opportunity.

Not to forget, for long-term portfolios, debt is also a cushion against equity volatility and is better returning. Debt and gold investments have the same taxation.

After all this, if you still want to invest in gold, keep this in mind:

- Do not invest in gold jewellery and coins. Physical gold will not capture the actual gold price movement due to wastage. Quality is also suspect. You also have practical issues like liquidity and other irrecoverable charges.

- Financial gold such as ETFs, gold mutual funds and sovereign gold bonds are the only way to effectively reap the benefit of gold price movement. They are also more liquid and do not have storage or quality risks that physical gold does. Limit such exposure to about 10% of your portfolio.

- You should be able to differentiate between gold for consumption purposes and for investment purposes. Be mindful when you are accumulating gold jewellery in the name of investing.

So use this auspicious time to make smarter investment choices by limiting your gold rush. While you are exploiting Diwali sales elsewhere, don’t forget the equity markets are also at a low!

Wealth Conversations – April 2024

Wealth Conversations – April 2024- Temporary suspension of subscriptions in ” Mirae Asset Global Electric & Autonomous Vehicles ETFs Fund of Fund & Mirae Asset Global X Artificial Intelligence & Technology ETF Fund of Fund

- Merger Announcement: Aditya Birla Sun Life CRISIL IBX AAA Mar 2024 Index Fund

Here is everything that you need to know about Arbitrage Funds

Here is everything that you need to know about Arbitrage Funds- Temporary suspension of subscriptions in “DSP US Treasury Fund of Fund”