Women are better investors than men. Period. Study after study has vouched the accuracy of this statement, and survey after survey does well to drive home the point. But here’s what’s surprising: In spite of being able to manage money and investments well, women shy away from embracing their potential.

Only 20.6 per cent of investors at FundsIndia constitute women – a shocking number in today’s day and age. N. Sathyamoorthy, Analyst – Mutual Fund Research, FundsIndia.com, believes that patriarchy still exists in the world of investments. “In India, most money-related decisions are made by men. Even if women earn an income, or manage the savings of the household, they tend to choose traditional options like banks savings accounts and fixed deposits. To overcome this divide, firstly, women need to educate themselves on the better investing options available in the market. Secondly, they need to take charge of their money and make a start at investing.”

Here are a few simple ways to get started with the healthy habit of investing:

1. First save, then spend – Here’s the simplest way to build wealth: When calculating your monthly expenditure, first, keep money aside for saving, and then keep money aside for expenses. The golden formula is this: Income – Savings = Expenditure. Most households tend to follow the formula – Income – Expenditure = Savings. When you start following this archaic formula, very soon, Income becomes equal to Expenditure, leaving no room for Savings.

2. Stop “investing” in gold – Gold, as an investment in the long run, will match inflation, but not beat it, making it an impractical choice of investing your money. Vidya Bala, Head – Mutual Fund Research, explains, “Instead of buying gold jewellery, start investing your money in gold funds and gold Exchange Traded Funds (ETFs). They are more cost effective because there are no wastage charges, no making charges, and no security issues. Usually, Indian families start buying jewellery for their daughters from a young age to gift it to them at the time of their wedding. However, there may be a change in fashion then and you may have to sell the jewellery to buy new designs. This would burn a hole in your pocket. Instead, if you invest in gold funds and gold ETFs, you can simply sell them at market value when you need to buy jewellery.”

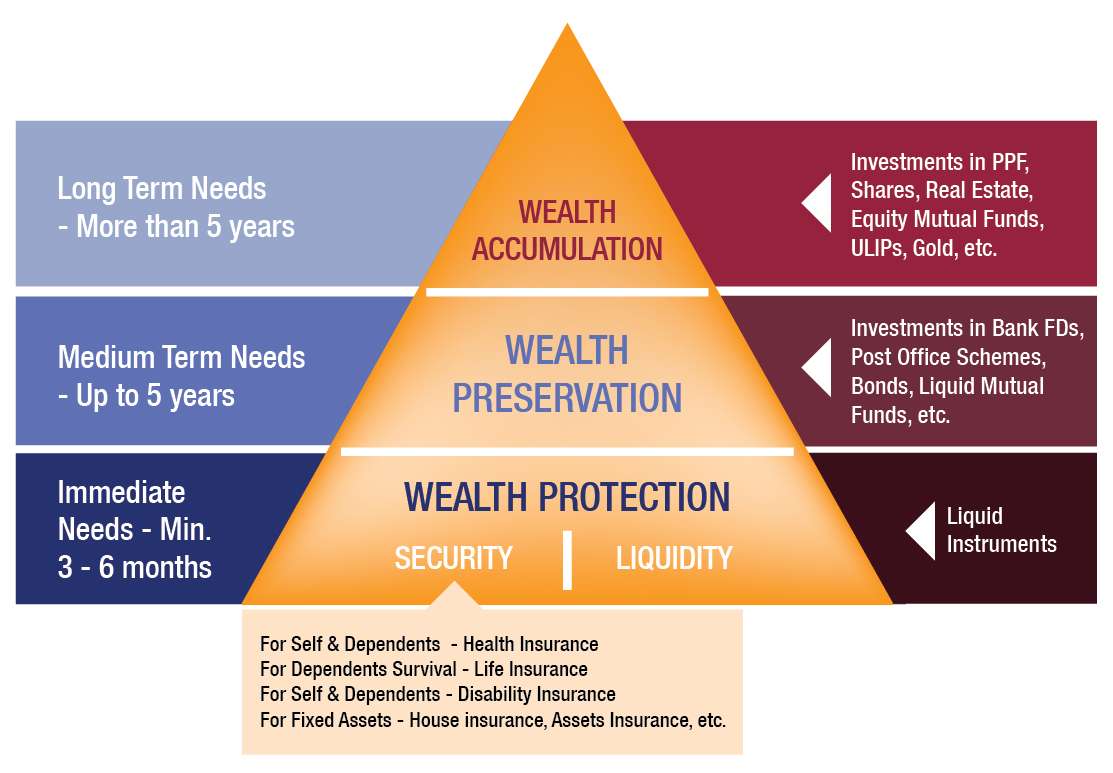

- Single or double? – Do you earn an income? Does your family depend on your income? It is essential to ask yourself these questions to make sure you put your money to the best possible use in the best investment instruments. If your family depends on a part of your income / your full income, and if you have less assets to back you up, you must invest your money in less risky instruments like debt mutual funds. Also, do make sure you maintain an emergency fund at all times, an ideal number for which is about six months of your salary. If you belong to a dual income family and if the dependency on your income is low, you can opt for long-term debt funds, equity mutual funds, and you can also indulge in direct equity investments. The basic rule is this: Higher the dependency on your income, lower should be your risk. Lower the dependency on your income, higher can be your risk.

-

It takes two to tango – Do not underestimate the power of expert advice. An expert investment advisor will be able to understand your income structure, expenses, and ambitions, and will help you chart out a plan accordingly. It is even better if you and your spouse approach an advisor together. Speaking to an investment expert allows you to understand your financial picture clearly. When you and your spouse speak to one advisor and discuss your finances with him / her, you get a comprehensive view of your financial status, making it easier for you to draw and stick to a plan together. At FundsIndia.com, all investors enjoy free financial advisory services from a dedicated financial advisor that is assigned to him / her.

-

Make the shift – If you’re used to investing in traditional investment options, it’s time to make the shift. And it’s time you do it now. Says Bala, “Save just 10 – 20 per cent of your savings in bank accounts and fixed deposits. You can use this at the time of any emergency. The rest of your savings must be directed towards high return yielding instruments like long-term debt funds, equity funds, and stocks. If you have time on your side, that is, if you are approximately 15-20 years away from your retirement, then you can afford to take some risk, thereby meaning greater rewards for you in the future. Try to keep your investments going until the decided time frame, and avoid stopping mid-way. Seek an advisor’s help to review your investments every year and make changes accordingly to make sure you get to your goals without any hiccups. Follow all this, and you’re on your way to making money in the markets!”

So, ladies! Embrace your investment potential! And gentlemen, allow the women in your lives to manage your savings. After all, you will also benefit when they bring home their profits from the market, isn’t it?

Wealth Conversations – April 2024

Wealth Conversations – April 2024- Temporary suspension of subscriptions in ” Mirae Asset Global Electric & Autonomous Vehicles ETFs Fund of Fund & Mirae Asset Global X Artificial Intelligence & Technology ETF Fund of Fund

- Merger Announcement: Aditya Birla Sun Life CRISIL IBX AAA Mar 2024 Index Fund

Here is everything that you need to know about Arbitrage Funds

Here is everything that you need to know about Arbitrage Funds- Temporary suspension of subscriptions in “DSP US Treasury Fund of Fund”