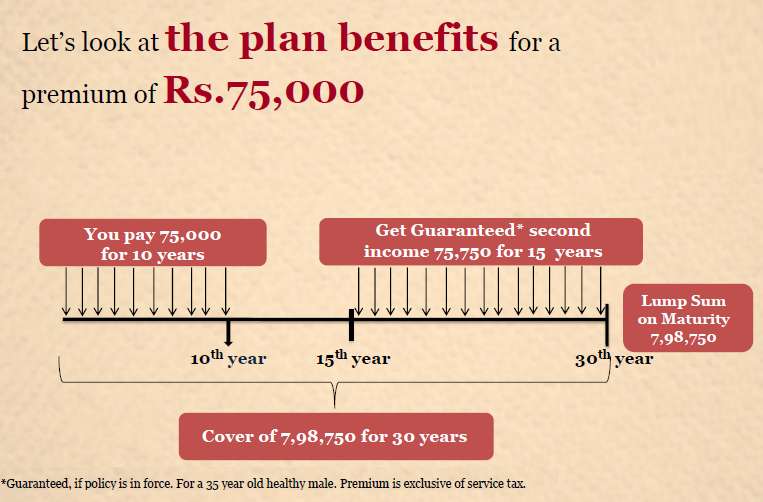

Kotak Assured Income Plan (AIP) is a flagship product from Kotak Life Insurance Company. It aims to provide guaranteed income to the policy holder, along with a life insurance cover, for a period of 30 years.

How the plan works

In this plan, the premium needs to be paid for a fixed tenure of 10 years, while the policy continues for 30 years. However, from the 15th policy year onwards, 9.1% – 10.1% of the Sum Assured is paid out to the life insured till the 29th policy year, as long as he/she is alive. Apart from this Annual Payout, there is a Maturity Benefit between 104% – 110% of the Sum Assured at the end of the policy year.

The Survival Benefit is calculated according to the Annual Premium. The Maturity Benefit will vary from 104% to 110% of the Sum Assured at the end of the policy term, which depends on the age of the policy holder at the time of entry.

However, if the life insured dies within the policy tenure, the Sum Assured is immediately paid as Death Benefit, irrespective of the amount already paid out, and the policy terminates.

Key features

- Assured income for 15 years

- Additional lump sum on maturity

- Provides protection for 30 years

- Additional protection through riders (Critical Illness, Accidental Death Benefit and Permanent Disability)

- Both the payouts and the maturity benefits are tax-free for the policy holder

Is this suitable for you

As this plan provides guaranteed payouts and long term protection to investors, it could be suitable for individuals who are looking out for regular income, coupled with a life cover. It is ideal for individuals in the age group of 40-50 years who would like some peaceful retirement income.

The return analysis

The Internal Rate of Return (IRR) for this product is close to 5.5%.

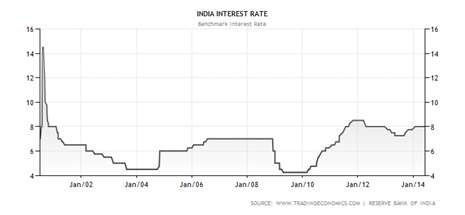

If you like guaranteed payouts coupled with a life cover, then we think this product may be good for you. The rationale behind this recommendation is that the interest rates of long-term fixed deposits in India were last recorded at 8%. This rate averaged to 7.38% from 2000 until 2013, reaching an all time high of 10% in the year 2000, and a record low of 5.25% in the year 2003 (as reported by the Reserve Bank of India).

We are of the opinion that the Indian economy grows well in the long term and hence, interest rates will obviously go down. The average interest rate stood at 7.38% which is taxable. If you come under the 30% tax slab, then the returns on fixed deposits would be close to 5.16%. In such a scenario, this product provides post tax returns of 5.5%, along with the advantage of long-term protection without taking any risk. Though the interest rates of fixed deposits and the returns from endowment plans are incomparable, it is still worthwhile to look at them from the angle of investments.

To conclude, this product is suitable for risk averse investors who are looking for a regular flow of income post retirement, and for investors who are looking out for well-disciplined investments.

Let’s assume that there is a 45-year-old investor who wishes to retire when he turns 60. So, he decides to start accumulating corpus for his retirement. The financial planner calculated his overall retirement cash flow needs to be about Rs. 5,00,000 per annum, and the present investment requirement to be Rs. 2,00,000 per annum. In such a scenario, one has to follow an asset allocation of 70:30, where 70% of the investment should be in equity and about 30% in debt to clock better average annual returns. In this case, one can choose equity mutual funds for the equity portion and the debt portion can be invested in Kotak’s AIP to lock in investments and get assured returns, as interest rates are changing rapidly from time-to-time.

Wealth Conversations – April 2024

Wealth Conversations – April 2024- Temporary suspension of subscriptions in ” Mirae Asset Global Electric & Autonomous Vehicles ETFs Fund of Fund & Mirae Asset Global X Artificial Intelligence & Technology ETF Fund of Fund

- Merger Announcement: Aditya Birla Sun Life CRISIL IBX AAA Mar 2024 Index Fund

Here is everything that you need to know about Arbitrage Funds

Here is everything that you need to know about Arbitrage Funds- Temporary suspension of subscriptions in “DSP US Treasury Fund of Fund”

Dear FundsIndia Team,

No doubt the product mentioned by you is best in the particular category though I have some different thoughts on the amount of Rs. 75000 available to invest.

As per my view person should not mix the investment and insurance. It is just like petrol & beer do not mix well similarly investment & insurance should not go together.

If a person has 75000 to invest he should open a great instrument called PPF wherein and should invest Rs. 68000 on yearly basis for 15 year and earn a interest rate of 8.5% annually. After 15 year the person will get approx Rs 20 Lacs and after 15 years an investor should invest Rs 20 Lac in some interest bearing instrument earning interest between 8 – 10%, earning interest of approx Rs. 160000 to Rs. 200000 annually.

And to take care the insurance need, an investor should buy term insurance of approx. Rs 7000 (from the initial available amount of Rs. 75000) for term of 30-35 years for sum assured of Rs. 50 lac.

Thanks

Hello Sir,

Thanks for writing to us. We have a point here that the PPF rates have come down from 11% to 8.5% in the last decade and the chances that the PPF interest rates may go down further. The second reason is that the limitation of only Rs.100,000 can be invested in PPF which may not be a very good vehicle for accumulating a larger corpus that is needed for retirement. All the more reason for recommending this plan is that the rates are fixed for the next 15 years irrespective of any economic/interest rate changing situation which is very good to lock in at this point. Again, it is not recommended to invest the entire portfolio here, only a portion of the portfolio can certainly be locked in for a guaranteed return.

Hope this clarifies.

Dear FundsIndia Team,

No doubt the product mentioned by you is best in the particular category though I have some different thoughts on the amount of Rs. 75000 available to invest.

As per my view person should not mix the investment and insurance. It is just like petrol & beer do not mix well similarly investment & insurance should not go together.

If a person has 75000 to invest he should open a great instrument called PPF wherein and should invest Rs. 68000 on yearly basis for 15 year and earn a interest rate of 8.5% annually. After 15 year the person will get approx Rs 20 Lacs and after 15 years an investor should invest Rs 20 Lac in some interest bearing instrument earning interest between 8 – 10%, earning interest of approx Rs. 160000 to Rs. 200000 annually.

And to take care the insurance need, an investor should buy term insurance of approx. Rs 7000 (from the initial available amount of Rs. 75000) for term of 30-35 years for sum assured of Rs. 50 lac.

Thanks

Hello Sir,

Thanks for writing to us. We have a point here that the PPF rates have come down from 11% to 8.5% in the last decade and the chances that the PPF interest rates may go down further. The second reason is that the limitation of only Rs.100,000 can be invested in PPF which may not be a very good vehicle for accumulating a larger corpus that is needed for retirement. All the more reason for recommending this plan is that the rates are fixed for the next 15 years irrespective of any economic/interest rate changing situation which is very good to lock in at this point. Again, it is not recommended to invest the entire portfolio here, only a portion of the portfolio can certainly be locked in for a guaranteed return.

Hope this clarifies.