A ready-made debt fund basket

The last few years have demonstrated that the Indian debt market has become more volatile and less predictable. Return opportunities of course, have risen along with the higher risks that many of these instruments now carry.

In such a scenario, you have two options if you wish to invest in a debt fund for wealth building: one, you may choose to simply hold medium-to-long-term income funds and not try to follow a cycle; two, try and ride the interest rate cycle with the right choice of funds that suit each cycle.

Now, the latter is more difficult and requires constant review and churn of your portfolio. It is for those who go with the second choice, that fund-of-funds such as ING Active Debt Multi-Manager FoF (ING Active Debt) may seem useful.

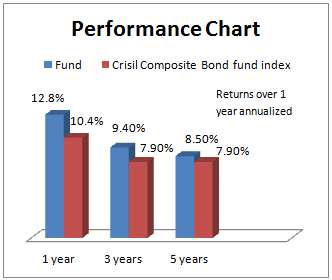

With a return of 9.4% annually in the last 3 years and 12.8% in the last 1 year, ING Active Debt has been in the top quartile of the performance chart of income funds.

The Fund

ING Active Debt is a fund-of-fund. But unlike a number of FoFs that invest in schemes from their own stable, ING Active Debt invests purely in third-party debt mutual funds (schemes from other AMCs). That means it has the option to pick the best in the industry rather than stick to what it has in house.

The fund invests in a combination of income, gilt, short-term, and liquid funds, the proportion of which is churned in line with changing interest rate scenarios. The fund will be treated like any other debt fund for capital gains tax purpose.

Suitability

ING Active Debt, as stated earlier, is suitable for investors wanting to hold a basket of funds and gain from interest rate movements with a time frame of at least 3 years. The fund is not suitable for investors looking to park short-term money as it does not have the characteristics of a liquid or ultra-short-term fund.

The advantage of holding ING Active Debt, over holding individual funds is that if you were to build your own basket of funds and actively churn your portfolio, you would incur capital gains tax. You may also face exit load if you hold for the short term.

A FoF will not incur capital gains tax when it churns, as rebalancing of underlying funds in a FoF portfolio does not suffer capital gains tax. Besides, you would also have an expert choosing the funds for you and also dynamically altering the allocation to suit interest rate cycles.

Performance

ING Active Debt delivered 8.4% annually since its inception beginning 2007; comfortably beating its benchmark – CRISIL Composite Bond Fund index return of 6.5%. Income funds on an average delivered 7% over the same period.

ING Active Debt delivered 8.4% annually since its inception beginning 2007; comfortably beating its benchmark – CRISIL Composite Bond Fund index return of 6.5%. Income funds on an average delivered 7% over the same period.

But ING Active Debt has had its roller-coaster ride as well. On a rolling one-year return basis over the last five years, the fund managed to beat its benchmark only 62% of the times.

That is not the mark of great consistency. But to its credit, it did not fall in to the negative turf, unlike some gilt/income funds that took long-dated calls in late 2008 and early 2009.

The fund fell about 1.2% from May 22, the day when debt markets started their descent. Higher exposure to long-dated income funds as well as gilt funds led to the decline post the hawkish stance by the US Federal Reserve.

While this fall is not insignificant, it is still better than the decline seen in funds such as SBI Dynamic Bond and Reliance Dynamic Bond.

Portfolio

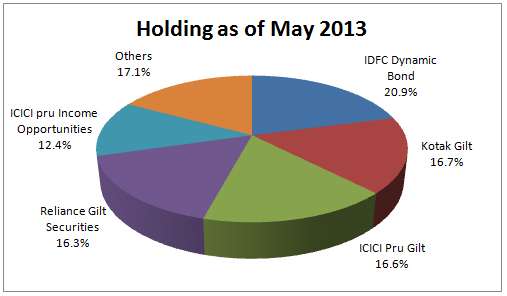

Some of the top holdings as of May included IDFC Dynamic Bond, ICICI Pru Income Opportunities, ICICI Pru Gilt and Kotak Gilt. The fund had increased its exposure to gilt funds to 58% as of May. However, post the fall in June (June portfolio was not available when this article was written), it reduced exposure to this space to 48%. It increased liquid instruments to about 7%.

One advantage that ING Active Debt holds in managing its portfolio is the ease with which it can navigate across different tenures. For instance, in the above mentioned case, the fund quickly reduced its exposure to gilt funds.

However, an individual gilt fund or an income fund may find it more difficult to quickly sell a long-dated paper and adjust the portfolio maturity, especially when the market is tanking.

The fund is managed by Shravan Kumar Srinivasula.

Note that we do not at present have a call on this fund.

Wealth Conversations – April 2024

Wealth Conversations – April 2024- Temporary suspension of subscriptions in ” Mirae Asset Global Electric & Autonomous Vehicles ETFs Fund of Fund & Mirae Asset Global X Artificial Intelligence & Technology ETF Fund of Fund

- Merger Announcement: Aditya Birla Sun Life CRISIL IBX AAA Mar 2024 Index Fund

Here is everything that you need to know about Arbitrage Funds

Here is everything that you need to know about Arbitrage Funds- Temporary suspension of subscriptions in “DSP US Treasury Fund of Fund”

Hi Vidya,

There is another fund called as All Seasons Bond Fund from IDFC which does exactly the same thing as this one except for the fact that it invests only in IDFC schemes. How do the 2 compare?

Also, the corpus of this ING fund is really miniscule. Isn’t that a factor in evaluation before investment? The other fact is that ING has not really been able to make its mark on the Indian MF scene. Would this not weigh against this fund?

Hello Dinesh,

An asset size of about Rs 300 crore cannot be called miniscule for an income fund, esp. a FoF. Their expense ratio is also competitive. That ING is not too established in MFs is true. It is for this reason that one may not wish to invest in ING’s own scheme. But this one is simply a FoF, although there is some element of active call in owning or exiting other funds. This fact may not therefore, weigh much against the fund. Thanks, Vidya

Every article i read about wealth management, there is one thing which is constant, it is always advised to distribute the investment between debt and equity. I do not know, how much it is applicable for indian markets. Anyways, personally, i feel as long as one distribute investment as per risk-return matrix, it should be fine. All equity investments do not carry same risk, investing in shares will have higher risk as compared to investing in mutual funds which is investing in only large cap stocks for example and investment in RDs let’s do not carry any risk at all. But yes, investment choices, depends upon person to person but i do not find debt funds that attractive to be honest.

Hi Vidya,

There is another fund called as All Seasons Bond Fund from IDFC which does exactly the same thing as this one except for the fact that it invests only in IDFC schemes. How do the 2 compare?

Also, the corpus of this ING fund is really miniscule. Isn’t that a factor in evaluation before investment? The other fact is that ING has not really been able to make its mark on the Indian MF scene. Would this not weigh against this fund?

Hello Dinesh,

An asset size of about Rs 300 crore cannot be called miniscule for an income fund, esp. a FoF. Their expense ratio is also competitive. That ING is not too established in MFs is true. It is for this reason that one may not wish to invest in ING’s own scheme. But this one is simply a FoF, although there is some element of active call in owning or exiting other funds. This fact may not therefore, weigh much against the fund. Thanks, Vidya

Hi Vidya,

ING is one of the fund houses I have not ventured into yet, however looking at the portfolio of this fund it looks very interesting. It has cherry picked the best GILT and Dynamic bond funds across the AMC’s as it’s top holdings.

I was planning to make some investment into BSL Dynamic Bond fund, but looking at this fund and it’s portfolio strategy, I am quite tempted. One of them is from a reputed and a stable AMC (BSL) and the other has a great portfolio mix (ING) in the current interest rate cycle.

Thanks,

Hi Vidya,

Any chance you had a look at my query?

Thanks

Hello Saurav, I thought you had made a comment:-) If your query is which one to go for BSL Dynamic Bond or ING, you have to simply answer this question: if you are a long-term investor (3-plus years) and simply wish to add a debt component to your portfolio then BSL should do. If you wish to play the debt game dynamically and ride the interest rate curve, then you either build your own portfolio of debt funds or go for options like ING.

But pl. note that as we said in the article, we do not have a view on the ING as yet. Thanks, Vidya

Thanks for your response Vidya.

Every article i read about wealth management, there is one thing which is constant, it is always advised to distribute the investment between debt and equity. I do not know, how much it is applicable for indian markets. Anyways, personally, i feel as long as one distribute investment as per risk-return matrix, it should be fine. All equity investments do not carry same risk, investing in shares will have higher risk as compared to investing in mutual funds which is investing in only large cap stocks for example and investment in RDs let’s do not carry any risk at all. But yes, investment choices, depends upon person to person but i do not find debt funds that attractive to be honest.

Hi Vidya,

ING is one of the fund houses I have not ventured into yet, however looking at the portfolio of this fund it looks very interesting. It has cherry picked the best GILT and Dynamic bond funds across the AMC’s as it’s top holdings.

I was planning to make some investment into BSL Dynamic Bond fund, but looking at this fund and it’s portfolio strategy, I am quite tempted. One of them is from a reputed and a stable AMC (BSL) and the other has a great portfolio mix (ING) in the current interest rate cycle.

Thanks,

Hi Vidya,

Any chance you had a look at my query?

Thanks

Hello Saurav, I thought you had made a comment:-) If your query is which one to go for BSL Dynamic Bond or ING, you have to simply answer this question: if you are a long-term investor (3-plus years) and simply wish to add a debt component to your portfolio then BSL should do. If you wish to play the debt game dynamically and ride the interest rate curve, then you either build your own portfolio of debt funds or go for options like ING.

But pl. note that as we said in the article, we do not have a view on the ING as yet. Thanks, Vidya

Thanks for your response Vidya.

Hi Vidya,

Similar to ING’s debt FoF, Kotak also runs a FoF running across fund houses (albeit with some representation to its own schemes) on the Equity side – Kotak Equity FoF.

What do u think of it?

Hi Dinesh,

Yes, Kotak has an equity FoF. But I see lessmerit in an equity Fof than a debt FoF, unless there is going to be an underlying asset allocation call (like FT India Dynamic PE or life stage funds) or it is for the purpose of a feeder fund. In debt, the constant churning would cause capital gains but in equity, a holding over 1 year is exempt from CG. Churning in less than a year in any case not a good idea. That being the case, one may hold their own basket of equity funds to suit their risk appetite. As for the performance of the fund you mentioned, it is mediocre. Thanks, Vidya

Hi Vidya,

Similar to ING’s debt FoF, Kotak also runs a FoF running across fund houses (albeit with some representation to its own schemes) on the Equity side – Kotak Equity FoF.

What do u think of it?

Hi Dinesh,

Yes, Kotak has an equity FoF. But I see lessmerit in an equity Fof than a debt FoF, unless there is going to be an underlying asset allocation call (like FT India Dynamic PE or life stage funds) or it is for the purpose of a feeder fund. In debt, the constant churning would cause capital gains but in equity, a holding over 1 year is exempt from CG. Churning in less than a year in any case not a good idea. That being the case, one may hold their own basket of equity funds to suit their risk appetite. As for the performance of the fund you mentioned, it is mediocre. Thanks, Vidya