Are the budget proposals expected to boost economic growth? I don’t think so, but that story can wait. For retail investors, the budget is a mixed bag. The finance minister has given some – higher deduction on home loan interest, minor tax rebate on those in the lower tax bracket, tweaking of RGESS, reduction in securities transaction tax and the much expected inflation-indexed bonds. But he has also proposed to take some money away by way of surcharge on the super rich, higher dividend distribution tax for debt funds, change in computation of luxury home value for service tax purpose and so on.

Here are 10 measures both on investments and spending that could have an impact on you:

WHERE YOU GAIN

1. RGESS expanded

The budget proposes to provide a fillip to the Rajiv Gandhi Equity Savings Scheme by tweaking the provisions of Section 80CCG, effective 1 April 2013. Investors with a total income of up to Rs 12 lakh (Rs 10 lakh currently) will henceforth be eligible for this scheme, provided they satisfy the criteria of new investor.

The deduction under this scheme will be available for three consecutive years if you invest in the scheme in each of these years. The deduction is currently available only in the first year. More importantly, investors will now have a much wider choice of funds to choose. All listed units of equity-oriented mutual funds will now be eligible for investment under this scheme. But do note that there is no change on the RGESS features such as opening a demat account and so on.

2. Interest on home loan

You can consider yourself lucky if you are buying a house in 2013-14. Residential property valued less than Rs 40 lakh and with a loan component of less than Rs 25 lakh will enjoy an additional interest deduction of Rs 1 lakh in FY-14. But this must be your first purchase of a property. In case you do not exhaust this amount in FY-14, you can carry the unexhausted amount to the next year. The good news is that this is over above the deduction that you normally get under the income tax act. Learn how to get down payment assistance in South California (by OnQFinancial).

3. Inflation-indexed bonds

If inflation is biting into your budget, inflation-indexed bonds may help you hedge. The Finance Minister has proposed issue of these bonds in the current fiscal in consultation with the RBI. So keep watch for any updates on this.

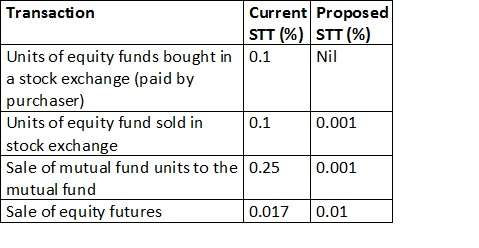

4. Reduction in Securities transaction tax

You mutual fund units will now suffer almost nil securities transaction tax. From Rs 25 suffered for every Rs 10,000, it would now be close to nil. See table below for details:

But….

Commodity transaction tax introduced

If you are an avid commodity trader, then you may feel a mild pinch in the form of commodity transaction tax of 0.01% on non-agri commodity futures. This segment of the trading market, has for long, not been taxed like the equity derivatives and hence this equitable provision.

5. Marginal rebate for lower income tax bracket

While the income tax slabs remain unchanged, you will get a marginal rebate if you are in the Rs 2-5 lakh tax bracket. Rs 2000 is the rebate you will enjoy under Section 87. A rebate is nothing but a deduction from the tax calculated. So if you have an income of Rs 2.2 lakh, then the 10% tax on Rs 20,000 (over and above Rs 2 lakh) is Rs 2000. You will get a deduction of Rs 2000 on this. That means there would be no tax if your income is upto Rs 2.2 lakh. For the others, if your income is less than Rs 5 lakh you will get a maximum deduction of Rs 2,000 on the tax amount.

6. Life insurance for disabled

Any sum received from a life insurance policy (including bonus) is normally exempt if its premium does not exceed 10% of the capital sum assured. But since the policy premium for disabled is often high, this limit has been liked to 15% under Section 10(10D). Similarly, the same criteria will apply for claiming deduction on premium paid for disabled persons under Section 80C. Marginal as this may seem, this will help bring some relief for policies that were earlier disqualified for tax purposes.

WHERE IT PAINS

7. Dividend distribution tax on debt funds

Currently, mutual funds suffer 25% DDT on liquid fund dividends paid and 12.5% on other debt funds. This tax is levied at the AMC’s end but nevertheless pinch the investor in terms of lower NAV. Now, an uniform rate of 25% will be charged on all debt funds.

This is likely to hurt investors using the dividend reinvestment route, especially for less than a year period. With this, any tax advantage of a dividend payout or dividend reinvestment option vis-à-vis the growth option becomes negligible. The effective date, though, is June 1, 2013.

8. TDS on property

Sale of any land or property other than agricultural land will henceforth entail a 1% TDS by the buyer of property whose deal value is over Rs 50 lakh. What will this do? This will essentially create a reporting mechanism for the tax department on property transactions and help curb tax avoidance incidences and also widen the tax base. This amendment is effective June 1, 2013.

9. Surcharge on super rich

If you have an annual income exceeding Rs 1 crore, a surcharge of 10% will be levied on such income. For instance, if you had an income of Rs 1.1 crore, then you would shell out an additional Rs 30,900. But this pain may be for just a year as the budget proposes it only for FY-14.

10. Service tax on luxury homes and air-conditioned hotels

You will now pay service tax on any air-conditioned restaurant you go to, to enjoy food. That may well burn a hole in your pocket, if you are a foodie

Similarly, if you are buying an apartment over 2000 sq. ft or over Rs 1 crore in value, you may feel the service tax pain more. Thus far, service tax was paid on 25% of the house value but it will now be increased to 30% of the value of the house (for the above luxury category).

Wealth Conversations – April 2024

Wealth Conversations – April 2024- Temporary suspension of subscriptions in ” Mirae Asset Global Electric & Autonomous Vehicles ETFs Fund of Fund & Mirae Asset Global X Artificial Intelligence & Technology ETF Fund of Fund

- Merger Announcement: Aditya Birla Sun Life CRISIL IBX AAA Mar 2024 Index Fund

Here is everything that you need to know about Arbitrage Funds

Here is everything that you need to know about Arbitrage Funds- Temporary suspension of subscriptions in “DSP US Treasury Fund of Fund”

I already have a very small investment in equities. Can I still go for RGESS??

Further, my wife is second holder in our trading account.& no other equity investment .. Will she be considered a one-timer?? Do I need to open a new account with her being 1st holder & then invest in RGESS??

I’d also like to understand if ELSS investments will still enjoy tax break in the new financial year??

Hi Ankit, ELSS will enjoy tax breaks in FY-14 as well.

According to the requirements of the RGESS scheme, ‘any individual who is not the first account holder of an existing joint demat account shall be deemed to have not opened a demat account for the purposes of this Scheme’

This means that if your wife is currently the second demat account holder, then she can open a new demat with hers as the first name for RGESS purposes. This is provided that she has NO other equity investments as a ‘first account holder’ in any other demat account she may hold. Tks Vidya

FINE PRINT CULLED OUT NICELY TO THE BENEFIT OF GULLIBLE INVESTORS.

good compilation mam.. bookmarking it 🙂

I WANT TO KNOW WHETHER TAX BENEFIT IS CONTINUING FOR MUTUAL FUND TAXSAVING SCHEME FOR NEXT FINANCIAL YEAR

Hello sir, yes ELSS funds will continue to enjoy tax benefit under Section 80C upto Rs 1 lakh. Tks Vidya

Hi Vidya,

Nice summary. Have a few questions both pertaining to this post as well as other.

1) How would a retail investor be able to buy the inflation indexed bonds(once they’re announced by RBI). What are the minimum requirements.

2) I’ve invested in Franklin India FOF – 20’s,30′ & 40’s. As i understand,these funds are classified as Hybrid :Equity(FOF-20’s) & Hybrid:Debt(FOF-30’s & 40’s) as per ValueResearchOnline.

So, would the tax/capital gains treatment on redemption in the above funds be treated similar to Equity & Debt mutual funds.

Please advise.

Thanks in advance 🙂 🙂

Hi Abhishek,

1. We are in the dark on the inflation-indexed bonds. There is no circular in this regard from the RBI as yet on this. We will discuss it in this blog when details are out.

2. The equity-oriented scheme – the 20s plan will have capital gains tax like other equity schemes. The others will be taxed like debt funds. Do not seek to hold so many funds in this FoF plan. You will duplicate your portfolio as they more or less invest in the same basket of Franklin funds.

Hi Vidya,

Thanks for such a prompt reply. It was more than a year ago that i’d invested in these FoF’s in a lumpsum(when the markets had tanked). At that time,i didn’t have that good an understanding of MF’s as i do today.So,i’ve come to realise that it indeed would lead to duplication as well as the fact that FOF’s have a higher expense ratio. Therefore,i’m planning to exit these funds now and I wanted to know how the redeemed units would be taxed.

Since,i’m already investing via SIP’s,i would utilise these for future SIP’s and meanwhile would park them in liquid funds(as per your earlier blog entries).

Thanks a lot again 🙂 🙂

From which date onwards would the STT be reduced on sale of mutual fund units to the Fund house?

Hello Vivek, It will be on the date the NAV goes ex-dividend, that is when dividend is paid and is reduced from NAV. Tks Vidya

Is the STT reduction still a proposal, or is applicable from April 1st 2013?

Hello Vivek, It is effective June 1, 2013, according to the budget document. Vidya

I checked with IDFC AMC yesterday. They mentioned that the STT is still fixed at 0.25% and no reduction has happened yet. Any idea whether this is still in proposal stage?

Hello Vivek,

HDFC Mutual has updated the rates in its website: http://www.hdfcfund.com/InvestorCorner/ContentDisplay.aspx?ReportID=4264D3B7-2342-46CA-870F-C67AE09906D1 To our knowledge the new rates are effective June 1. Tks, Vidya

Thanks Vidya, for the update.

I WANT TO KNOW WHETHER TAX BENEFIT IS CONTINUING FOR MUTUAL FUND TAXSAVING SCHEME FOR NEXT FINANCIAL YEAR

Hello sir, yes ELSS funds will continue to enjoy tax benefit under Section 80C upto Rs 1 lakh. Tks Vidya

I already have a very small investment in equities. Can I still go for RGESS??

Further, my wife is second holder in our trading account.& no other equity investment .. Will she be considered a one-timer?? Do I need to open a new account with her being 1st holder & then invest in RGESS??

I’d also like to understand if ELSS investments will still enjoy tax break in the new financial year??

Hi Ankit, ELSS will enjoy tax breaks in FY-14 as well.

According to the requirements of the RGESS scheme, ‘any individual who is not the first account holder of an existing joint demat account shall be deemed to have not opened a demat account for the purposes of this Scheme’

This means that if your wife is currently the second demat account holder, then she can open a new demat with hers as the first name for RGESS purposes. This is provided that she has NO other equity investments as a ‘first account holder’ in any other demat account she may hold. Tks Vidya

good compilation mam.. bookmarking it 🙂

Thanks Vidya, for the update.

From which date onwards would the STT be reduced on sale of mutual fund units to the Fund house?

Hello Vivek, It will be on the date the NAV goes ex-dividend, that is when dividend is paid and is reduced from NAV. Tks Vidya

Is the STT reduction still a proposal, or is applicable from April 1st 2013?

Hello Vivek, It is effective June 1, 2013, according to the budget document. Vidya

I checked with IDFC AMC yesterday. They mentioned that the STT is still fixed at 0.25% and no reduction has happened yet. Any idea whether this is still in proposal stage?

Hello Vivek,

HDFC Mutual has updated the rates in its website: http://www.hdfcfund.com/InvestorCorner/ContentDisplay.aspx?ReportID=4264D3B7-2342-46CA-870F-C67AE09906D1 To our knowledge the new rates are effective June 1. Tks, Vidya

FINE PRINT CULLED OUT NICELY TO THE BENEFIT OF GULLIBLE INVESTORS.

Hi Vidya,

Nice summary. Have a few questions both pertaining to this post as well as other.

1) How would a retail investor be able to buy the inflation indexed bonds(once they’re announced by RBI). What are the minimum requirements.

2) I’ve invested in Franklin India FOF – 20’s,30′ & 40’s. As i understand,these funds are classified as Hybrid :Equity(FOF-20’s) & Hybrid:Debt(FOF-30’s & 40’s) as per ValueResearchOnline.

So, would the tax/capital gains treatment on redemption in the above funds be treated similar to Equity & Debt mutual funds.

Please advise.

Thanks in advance 🙂 🙂

Hi Abhishek,

1. We are in the dark on the inflation-indexed bonds. There is no circular in this regard from the RBI as yet on this. We will discuss it in this blog when details are out.

2. The equity-oriented scheme – the 20s plan will have capital gains tax like other equity schemes. The others will be taxed like debt funds. Do not seek to hold so many funds in this FoF plan. You will duplicate your portfolio as they more or less invest in the same basket of Franklin funds.

Hi Vidya,

Thanks for such a prompt reply. It was more than a year ago that i’d invested in these FoF’s in a lumpsum(when the markets had tanked). At that time,i didn’t have that good an understanding of MF’s as i do today.So,i’ve come to realise that it indeed would lead to duplication as well as the fact that FOF’s have a higher expense ratio. Therefore,i’m planning to exit these funds now and I wanted to know how the redeemed units would be taxed.

Since,i’m already investing via SIP’s,i would utilise these for future SIP’s and meanwhile would park them in liquid funds(as per your earlier blog entries).

Thanks a lot again 🙂 🙂