Short on time? Listen to a brief overview of this week’s review.

What

- An income fund

- Follows an accrual strategy

Why

- Remains true to this buy-and-hold approach to top-quality debt

- Does not modify strategy like some peers to chase high yields

- Delivers low-volatile, above-average returns

Whom

- Conservative and moderate risk investors with a 3-year perspective

HDFC Medium Term Opportunities is a long-term debt fund. It earns its returns through interest accrued on the bonds it holds. The fund ticks three boxes. One, it holds papers that are of the top credit ratings and does not move into lower-quality instruments. Two, it delivers returns that are better than the average for the category and for lower risk. Three, it remains true to this buy-and-hold top-quality debt approach and does not play around with its portfolio to chase high yields.

The safety, predictability, low volatility packaged with higher returns make HDFC Medium Term Opportunities a good fit for a 3-year and above timeframe. It especially suits conservative and moderate risk investors looking for FD-beating returns without upping the risk by much.

Steady strategy

HDFC Medium Term Opportunities (HDFC MT) invests in medium and long-term bonds. In its portfolio, the fund does not take credit risk in payoff for the higher yields these instruments offer. On an average, debt rated AA+ and below formed about 5% of the portfolio since its inception. Where it did move below the AAA set, the fund remained in the AA and AA+ band and not lower. In fact, since April last year, the fund has moved entirely out of these instruments.

Its current portfolio yield-to-maturity at 7.01% is below the income fund average of 7.38%. It’s also well below category toppers DSP BlackRock Income Opportunities, L&T Resurgent India Corporate Bond, or Axis Regular Savings all of which sport YTMs in excess of 8%. However, these funds also have a third to half their portfolio in securities rated below AAA, making their risk profile very different.

HDFC MT has still managed to keep its returns above the average for the category. It uses trading opportunities on its AAA-rated bonds to enhance returns. In falling rate cycles, it invests a small portion of its portfolio in government bonds to gain from bond price rallies and thus shore up returns.

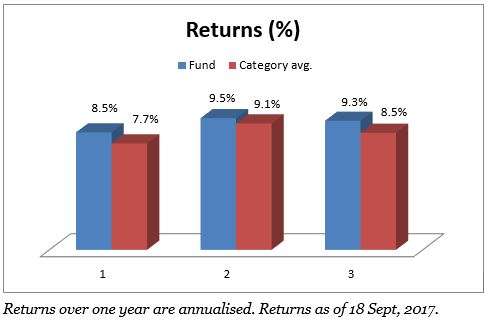

HDFC MT is among the lowest volatile income funds. Along with this, its risk-adjusted return is among the highest above even those that do take credit risk. Its average rolling 3-year return over 5 years at 9.4% is well above the category’s 8.5%. Even its worst return of 7.6% in this period was well above almost all peers. There is no one-year or even 6-month period since its inception that the fund has delivered a loss. Other funds with high credit quality portfolios, such as IDFC SSIF – Medium Term have not matched HDFC MT’s ability to deliver above-average returns or high risk-adjusted returns.

Portfolio

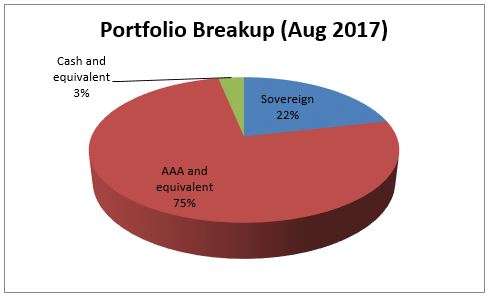

HDFC MT holds 75% of its portfolio in AAA-rated corporate bonds. Issuers represent a mix of PSUs such as PFC and Power Grid as well as private sector players such as Bajaj Finance and M&M Financial Services. It holds no paper rated below AAA.

A fifth of the portfolio is in state development loans, which at 7.9% – 8.7% are backed by government and come with good yields. The fund hasn’t gone for very long-term bonds, with maturities of less than five years and even 1-2 years in some cases. Its average maturity is therefore not very high at 2.8 years, leaving it with the room to adjust the portfolio to rate changes in the coming quarters.

HDFC MT is unlikely to provide chart-topping returns, especially now with peer funds holding higher-yielding instruments. However, for those looking for returns superior to long-term fixed deposits or a portfolio diversification from high-risk equity, a low-volatile fund is preferable. The fund is also better than dynamic bond funds for conservative investors, owing to the higher volatility inherent in dynamic bond funds.

HDFC MT’s added advantage is that it has not modified its strategy to look for higher returns. With debt funds changing colour based on market conditions as we pointed out last week, the ability to rely on this fund’s low-risk strategy is a positive. The fund has an AUM of Rs 12,150 crore. Anupam Joshi is the fund’s manager.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis for investment decisions. To know how to read our weekly fund reviews, please click here.

Wealth Conversations – April 2024

Wealth Conversations – April 2024- Temporary suspension of subscriptions in ” Mirae Asset Global Electric & Autonomous Vehicles ETFs Fund of Fund & Mirae Asset Global X Artificial Intelligence & Technology ETF Fund of Fund

- Merger Announcement: Aditya Birla Sun Life CRISIL IBX AAA Mar 2024 Index Fund

Here is everything that you need to know about Arbitrage Funds

Here is everything that you need to know about Arbitrage Funds- Temporary suspension of subscriptions in “DSP US Treasury Fund of Fund”

{kind=link}

In this current scenario, is it advisable to invest in debt funds? A rep from HDFC mutual fund suggested me to go for hdfc equity savings arbitrage fund rather than debt fund. I wanted to invest(20%) in hdfc med term opp or short ter opp to balance my sip portfolio. My next financial goal is son’s edu in 5yrs.

My sip portfolio has

Franklin ind prima plus 30%

Icici pru val disc & L&T ind val fund 30%

Mirae asset emerging blue chip 10%

Franklin i smaller cos 10%

Debt fund??? (20%)

I already hold icici long term growth fund (20%) in my lumpsum wealth creation portfolio.

Should i go for balanced fund otherwise? Please advice.

Thanks n regards

Yavika, On your first question, the equity savings fund is not a substitute for debt since it can also deliver negative returns in a market fall. If you are looking for low risk – go with debt funds. If you can take risks, since you have a 5-year time frame, then go with some exposure to regular equity funds. In that case you don’t need equity savings. You need some equity and debt. For specific fund advice, please get in touch with your FundsIndia advisor or use the advisor appointment feature in your FundsIndia account. I will be constrained from providingfund-specific advice in this forum. thanks, Vidya

THANK YOU MAM. I am not looking for specific fund advice, i understand your point. I was asking

1. In this interest rate scenario, can we still go in for Debt funds?

2. Or avoid debt and include balanced fund or MIPs instead ?

Since i have regular Equity funds, I think I should allocate little in debt funds, is it that way Mam?, please confirm. I can take risk.

thanks n regards,

Yavika

Note: It’s a suggestion. Please write an article on how to reallocate/rebalance portfolio as one nears their financial goals. thanks. Have learnt a lot from your articles, always to the point, with clarity.

i totally understand that Hybrid or balanced funds are not replacement to debt funds, they simply have some part allocated to debt. But over longer periods, they have delivered good returns.

Hello,

Debt funds are always good to hold; regardless of rate cycles, they deliver FD-plus returns. Debt funds are present in a portfolio to counter equity and provide a shield when equity falls. Trying to time your investments according to rate cycles – and doing this by moving to higher-risk funds in the interim – will be impractical and detrimental. We cannot time stock markets correctly, nor do we have the ability to time rate cycles. All that there is to do is decide an asset allocation and funds based on your requirements, run SIPs in them, review and rebalance (if required) once a year. This is the best way to avoid being influenced by equity and debt market events. If you have a near-term requirement, then you cannot do anything but invest in debt funds regardless of rate cycle. And if they give FD-plus returns, why shouldn’t you?

Thanks,

Bhavana

HDFC Med Term opportunities debt fund sounds interesting. I am , however, looking for a debt fund which is short term and monthly/qrt returns. Any suggestions

Hello,

Apologies for the delay in reply. You can refer to our Select list for quality short-term and ultra short-term funds (depending on your investment horizon) that deliver above-average returns without going overboard on credit risk. However, if by monthly/quarterly returns you mean dividends, you cannot depend on mutual funds. Dividends are not constant, guaranteed, or predictable. For debt funds, dividends are additionally subject to dividend distribution tax. Dividend from mutual funds is, at the end of the day, your own money returned – its stripped from your NAV and given to you. Depending on your needs, running an SWP from your debt fund would serve better in terms of ensuring cash flows.

Thanks,

Bhavana

sir, i m a student i save 300 rupees every month. But i want to invest money in mutual funds. But i don’t know how to invest money in mutual funds. could u give me an idea of investing my savings in mutual funds which will give me a long term benifit in future.

Hello sir,

That you are able to save each month, even while being a student, is wonderful and commendable. You cannot save monthly, however, since Rs 300 is too small. The minimum amount for SIPs is usually Rs 1,000 or Rs 500 depending on the fund. You could try accumulating Rs 1200 every four months or Rs 1000 every 3 months and investing that amount in a fund. Which fund you should invest in depends on the purpose for which you are investing. Long term is usually at least 5-7 years, so is that what you’re looking for? Or would you need it for some expense (like application fee for post-grad or some other course or some entrance exam) in the coming few years? Would you need it to buy a bike or something like that in 2-3 years? Etc…. This will tell you how many years you can invest. Then you need to understand how much risk you can take – will you panic when your investment value falls by 15%? Or will you stay calm? Add more? Time horizon and risk together will help figure out which funds are suitable for you to invest in. Don’t go by recent returns alone when selecting a fund – understand how it has performed in other time periods as well. For first-time long-term investors, something like a balanced fund would be best. Debt funds are better for shorter term timeframes.

Thanks,

Bhavana

Hi Bhavana, I received a mail from HDFC AMC regarding HDFC Medium Term fund. the has undergone a major change in it’s fundamentals and objective. It’s proposed to be a Corporate Bond Fund investing in AA+ corporate bonds. and also two other funds i.e. HDFC floating rate fund (long term) and hdfc Gilt fund( short term) are getting merged with this fund.

they are giving me the exit option. SHOULD I EXIT ? PLEASE ADVICE.

THANKS

Hi

HDFC Medium Term was always a medium maturity accrual fund that restricted itself to top-quality papers. Please get in touch with your FundsIndia advisor, if you’re a FundsIndia investor, for specific advice on the course of action.

Thanks,

Bhavana

Hi Bhavana, I received a mail from HDFC AMC regarding HDFC Medium Term fund. the has undergone a major change in it’s fundamentals and objective. It’s proposed to be a Corporate Bond Fund investing in AA+ corporate bonds. and also two other funds i.e. HDFC floating rate fund (long term) and hdfc Gilt fund( short term) are getting merged with this fund.

they are giving me the exit option. SHOULD I EXIT ? PLEASE ADVICE.

THANKS

Hi

HDFC Medium Term was always a medium maturity accrual fund that restricted itself to top-quality papers. Please get in touch with your FundsIndia advisor, if you’re a FundsIndia investor, for specific advice on the course of action.

Thanks,

Bhavana

Hi

HDFC Medium Term was always a medium maturity accrual fund that restricted itself to top-quality papers. Please get in touch with your FundsIndia advisor, if you’re a FundsIndia investor, for specific advice on the course of action.

Thanks,

Bhavana

In this current scenario, is it advisable to invest in debt funds? A rep from HDFC mutual fund suggested me to go for hdfc equity savings arbitrage fund rather than debt fund. I wanted to invest(20%) in hdfc med term opp or short ter opp to balance my sip portfolio. My next financial goal is son’s edu in 5yrs.

My sip portfolio has

Franklin ind prima plus 30%

Icici pru val disc & L&T ind val fund 30%

Mirae asset emerging blue chip 10%

Franklin i smaller cos 10%

Debt fund??? (20%)

I already hold icici long term growth fund (20%) in my lumpsum wealth creation portfolio.

Should i go for balanced fund otherwise? Please advice.

Thanks n regards

Yavika, On your first question, the equity savings fund is not a substitute for debt since it can also deliver negative returns in a market fall. If you are looking for low risk – go with debt funds. If you can take risks, since you have a 5-year time frame, then go with some exposure to regular equity funds. In that case you don’t need equity savings. You need some equity and debt. For specific fund advice, please get in touch with your FundsIndia advisor or use the advisor appointment feature in your FundsIndia account. I will be constrained from providingfund-specific advice in this forum. thanks, Vidya

Yavika, On your first question, the equity savings fund is not a substitute for debt since it can also deliver negative returns in a market fall. If you are looking for low risk – go with debt funds. If you can take risks, since you have a 5-year time frame, then go with some exposure to regular equity funds. In that case you don’t need equity savings. You need some equity and debt. For specific fund advice, please get in touch with your FundsIndia advisor or use the advisor appointment feature in your FundsIndia account. I will be constrained from providingfund-specific advice in this forum. thanks, Vidya

HDFC Med Term opportunities debt fund sounds interesting. I am , however, looking for a debt fund which is short term and monthly/qrt returns. Any suggestions

Hello,

Apologies for the delay in reply. You can refer to our Select list for quality short-term and ultra short-term funds (depending on your investment horizon) that deliver above-average returns without going overboard on credit risk. However, if by monthly/quarterly returns you mean dividends, you cannot depend on mutual funds. Dividends are not constant, guaranteed, or predictable. For debt funds, dividends are additionally subject to dividend distribution tax. Dividend from mutual funds is, at the end of the day, your own money returned – its stripped from your NAV and given to you. Depending on your needs, running an SWP from your debt fund would serve better in terms of ensuring cash flows.

Thanks,

Bhavana

sir, i m a student i save 300 rupees every month. But i want to invest money in mutual funds. But i don’t know how to invest money in mutual funds. could u give me an idea of investing my savings in mutual funds which will give me a long term benifit in future.

Hello sir,

That you are able to save each month, even while being a student, is wonderful and commendable. You cannot save monthly, however, since Rs 300 is too small. The minimum amount for SIPs is usually Rs 1,000 or Rs 500 depending on the fund. You could try accumulating Rs 1200 every four months or Rs 1000 every 3 months and investing that amount in a fund. Which fund you should invest in depends on the purpose for which you are investing. Long term is usually at least 5-7 years, so is that what you’re looking for? Or would you need it for some expense (like application fee for post-grad or some other course or some entrance exam) in the coming few years? Would you need it to buy a bike or something like that in 2-3 years? Etc…. This will tell you how many years you can invest. Then you need to understand how much risk you can take – will you panic when your investment value falls by 15%? Or will you stay calm? Add more? Time horizon and risk together will help figure out which funds are suitable for you to invest in. Don’t go by recent returns alone when selecting a fund – understand how it has performed in other time periods as well. For first-time long-term investors, something like a balanced fund would be best. Debt funds are better for shorter term timeframes.

Thanks,

Bhavana

THANK YOU MAM. I am not looking for specific fund advice, i understand your point. I was asking

1. In this interest rate scenario, can we still go in for Debt funds?

2. Or avoid debt and include balanced fund or MIPs instead ?

Since i have regular Equity funds, I think I should allocate little in debt funds, is it that way Mam?, please confirm. I can take risk.

thanks n regards,

Yavika

Note: It’s a suggestion. Please write an article on how to reallocate/rebalance portfolio as one nears their financial goals. thanks. Have learnt a lot from your articles, always to the point, with clarity.

i totally understand that Hybrid or balanced funds are not replacement to debt funds, they simply have some part allocated to debt. But over longer periods, they have delivered good returns.

i totally understand that Hybrid or balanced funds are not replacement to debt funds, they simply have some part allocated to debt. But over longer periods, they have delivered good returns.

Hello,

Debt funds are always good to hold; regardless of rate cycles, they deliver FD-plus returns. Debt funds are present in a portfolio to counter equity and provide a shield when equity falls. Trying to time your investments according to rate cycles – and doing this by moving to higher-risk funds in the interim – will be impractical and detrimental. We cannot time stock markets correctly, nor do we have the ability to time rate cycles. All that there is to do is decide an asset allocation and funds based on your requirements, run SIPs in them, review and rebalance (if required) once a year. This is the best way to avoid being influenced by equity and debt market events. If you have a near-term requirement, then you cannot do anything but invest in debt funds regardless of rate cycle. And if they give FD-plus returns, why shouldn’t you?

Thanks,

Bhavana

Hello,

Debt funds are always good to hold; regardless of rate cycles, they deliver FD-plus returns. Debt funds are present in a portfolio to counter equity and provide a shield when equity falls. Trying to time your investments according to rate cycles – and doing this by moving to higher-risk funds in the interim – will be impractical and detrimental. We cannot time stock markets correctly, nor do we have the ability to time rate cycles. All that there is to do is decide an asset allocation and funds based on your requirements, run SIPs in them, review and rebalance (if required) once a year. This is the best way to avoid being influenced by equity and debt market events. If you have a near-term requirement, then you cannot do anything but invest in debt funds regardless of rate cycle. And if they give FD-plus returns, why shouldn’t you?

Thanks,

Bhavana