Post September, those of you who held debt funds for the long-term would have seen a sudden dip in returns. While equity markets went through this rout, debt markets also slipped a bit. This may have worried you. So, what caused the slip in the performance of debt funds? With another monetary policy behind us and no announcement of rate cuts, what should you expect from here on?

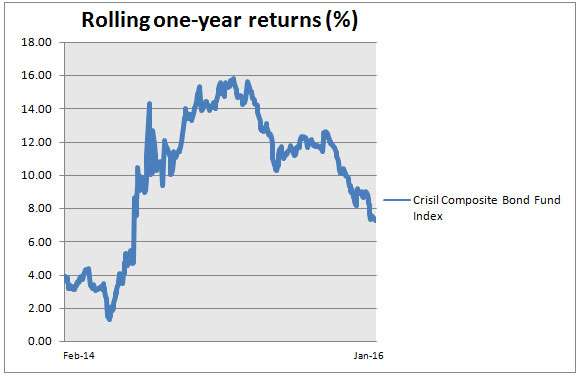

From August 2014 till almost November 2015, the one-year returns of most long-term debt funds – be it gilt or accrual funds, sported double-digit, or near double-digit returns. Clearly, the anticipation of a rate cut and such an event occurring from January 2015, led to a massive rally. In other words – duration play (rates falling and leading to a rally in bonds) was at its best. The table below gives the rolling 1-year returns of the Crisil Composite Bond Index – an index (which in reality is not easy to beat) which has a mix of medium to long-term corporate bonds and gilts, as well as short-term instruments. Rolling one-year returns mean the one-year return, from any given date to a year ago.

As can be seen, returns peaked in February-March of 2015, post the rate cut in January and March 2015. However, since then, much of the cuts were factored in, not leaving much scope for a further rally.

Fine, but what happened to the rate cuts done in June and September 2015, taking the total rate cuts to 125 basis points in the whole of 2015? Were they already factored? Not entirely.

Bond yields don’t necessarily react to rate cuts alone. Other events that happened in 2015 also impacted the movement of yields:

- One, the devaluation of the yuan by China post mid 2015, and the ensuing depreciation of the rupee also caused a yield of gilts to be impacted. Besides, the risk of a pull out of FII money in the Asian region as a result of a slowdown in China, not only impacted equity markets, but the debt market as well. In fact, it caused net outflows of debt by FII in 3 months of 2015, and tepid net flows for another three months. That means pressure on gilt yields.

-

Two, the much anticipated rate hikes in the US continued to threaten debt markets globally, and India was no exception. This caused yields to remain stubbornly at almost the same levels, despite the rate cuts.

-

Three, a high base began to kick in as high 1-year returns have remained from August 2014, and started to impact returns from November 2015.

Given this scenario should you expect your debt funds to deliver? Yes, you can, depending on which category you are invested in.

- If you are invested in pure long-term gilt funds, you may have to wait a bit and take some volatility. Remember, while credit risk is a different ball game, it is duration risk that causes more volatility to your portfolio. This category may provide high short-term returns and fade away quickly. Unless you are a discerning debt market investor, this may not be the best class funds for you to stay invested in.

-

If you are invested in income accrual funds (such as Franklin India Income Opportunities, Franklin India Income Builder and HDFC Medium Term Opportunities from our Select Funds list), you will notice that they have been less volatile and withstood this period better. It is because they do not take many interest rate calls. They bet on accrual (interest on the bonds) and any capital appreciation from corporate bonds on re-rating or declining spread on improved corporate fundamentals. Today, this is the most consistent segment to be invested in. The coupon income from bonds that this segment holds ensures there is less volatility and steady accrual income that feeds into your returns.

-

If you are invested in dynamic bonds, you may have had some short-term pain by way of a slide in your returns from double digits to low single digits. We would recommend that you hold these funds for the time frame for which you originally intended to hold. Given the flexibility that these funds have, they will likely reduce their duration, or add more corporate bonds (for accrual), depending on when they expect yields to fall. In this segment, you can expect some volatility; but holding them can deliver superior returns over the next two years.

Currently, 10-year gilt yields are at roughly the levels they were a year ago (about 7.72 per cent). That means we are back to where we were in January 2015; so, returns would be almost flat now. Another way of looking at it is that the positive impact of rate cuts done thus far has reversed, once again, providing scope for yields to ease. This, of course, will depend on other factors such as liquidity, inflation and FII flows.

That FIIs have been net buyers in debt (although selling in equities) suggests that they see opportunities in this segment.

Role of debt funds in volatile times

Investors would do well to continue to hold debt. For those of you who feel debt is not a great diversifier as it did not do well even as equities fell, the following is to be noted: those portfolios that had debt contained falls better than an all equity portfolio. And that is the primary job of debt as a diversifier. Hence, look at your portfolio returns as a whole, instead of standalone returns, to appreciate the value that debt brings to your portfolio.

FundsIndia’s Research team has, to the best of its ability, taken into account various factors – both quantitative measures and qualitative assessments, in an unbiased manner, while choosing the fund(s) mentioned above. However, they carry unknown risks and uncertainties linked to broad markets, as well as analysts’ expectations about future events. They should not, therefore, be the sole basis of investment decisions. To know how to read our weekly fund reviews, please click here.

Wealth Conversations – April 2024

Wealth Conversations – April 2024- Temporary suspension of subscriptions in ” Mirae Asset Global Electric & Autonomous Vehicles ETFs Fund of Fund & Mirae Asset Global X Artificial Intelligence & Technology ETF Fund of Fund

- Merger Announcement: Aditya Birla Sun Life CRISIL IBX AAA Mar 2024 Index Fund

Here is everything that you need to know about Arbitrage Funds

Here is everything that you need to know about Arbitrage Funds- Temporary suspension of subscriptions in “DSP US Treasury Fund of Fund”

It is generally advised to invest in liquid fund when the period of investment is short: few days to 3-4 months. With my debt investments, I would prefer to stay away from interest risk and duration risk (because I am already taking risk on equity). What opportunity would I miss if I stay invested in liquid funds till I require the capital (which could, say, span years)?

Hello Vijay,Sorry about the delayed response. if it is 5 years or over, you will certainly miss the power of equities.If it is lesser, you will not miss much in a high interest scenario but will miss on the debt rally in a falling interest scenario, if you remain in liquid funds. thanks, Vidya

Nice one, thanks for sharing. I never understood fully how RBI rate cut or hike impact market, could you please share the link or details on this as I recently started giving attention towards market ( after joining fundsindia :)…..)

It is generally advised to invest in liquid fund when the period of investment is short: few days to 3-4 months. With my debt investments, I would prefer to stay away from interest risk and duration risk (because I am already taking risk on equity). What opportunity would I miss if I stay invested in liquid funds till I require the capital (which could, say, span years)?

Hello Vijay,Sorry about the delayed response. if it is 5 years or over, you will certainly miss the power of equities.If it is lesser, you will not miss much in a high interest scenario but will miss on the debt rally in a falling interest scenario, if you remain in liquid funds. thanks, Vidya

Nice one, thanks for sharing. I never understood fully how RBI rate cut or hike impact market, could you please share the link or details on this as I recently started giving attention towards market ( after joining fundsindia :)…..)

Do U recommend UTI-Short Term Income Fund or UTI-DYNAMIC BOND FUND or MIS AGGRESIVE FUNDS.

Hello Vinod, Sorry about the delayed response. please talk to our advisors or write to us from your account, if you are a FundsIndia customer to know our recommendations. Vidya

Do U recommend UTI-Short Term Income Fund or UTI-DYNAMIC BOND FUND or MIS AGGRESIVE FUNDS.

Hello Vinod, Sorry about the delayed response. please talk to our advisors or write to us from your account, if you are a FundsIndia customer to know our recommendations. Vidya